Home » 2014

Yearly Archives: 2014

My wish for this year’s Nobel prize in economics

I know it’s a fool’s business trying to predict who is going to win the prize every year.

But here is my wish:

Oliver Hart and/or Ben Holmstrom

For his (or their) contribution to the theory of firm.

Why most Americans don’t feel the recession is over?

During the past five years, I have seen many similar charts. But this one really stands out as the best story-teller.

(source: vox.com)

Minsky on financial instability

Stability is destabilizing.

BBC runs a 30-minute program on Minsky and why his insights matter.

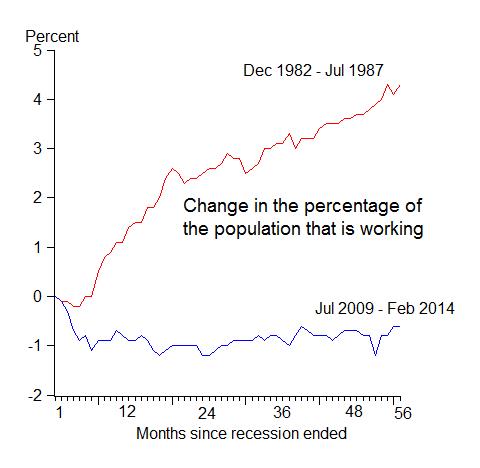

Still the same

Official unemployment rate has gone down dramatically, but the improvement of labor market has been largely fake, as the employment-population ratio hasn’t moved much since recession ended. See this sharp chart from John Taylor at Stanford.

You can also take a longer term perspective at this ratio below:

Feel puzzled? You can find out the reason why unemployment rate and the employment-population ratio tend to diverge during this reovery here.

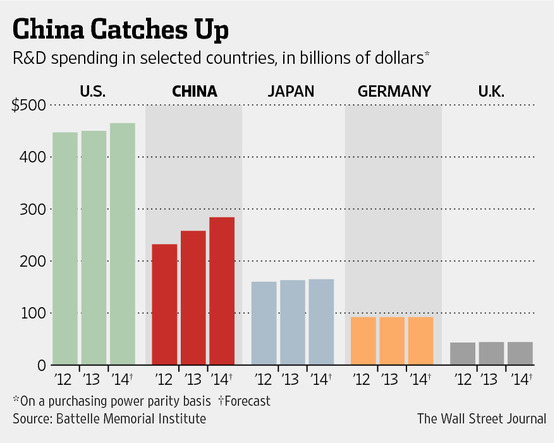

R&D and a hint of China’s future global brand

According to a study released in December by U.S.-based Battelle Memorial Institute, R&D spending in China will likely reach $284 billion this year, up 22% from 2012. That compares with just 4% growth forecast in the U.S. to $465 billion for the same period. It forecasts China will surpass Europe in terms of R&D spending by 2018 and exceed the U.S. by 2022.

According to WSJ, three Chinese companies are likely to emerge as China’s innovation leaders. They are Huawei, Lenovo and Tencent.

At Shenzhen-based Huawei Technologies Co., the world’s second-largest telecommunications-equipment supplier by revenue after Sweden’s Ericsson, annual R&D expenditures rose fourteenfold in a decade to $5.46 billion in 2013 from $389 million in 2003.

Personal-computer maker Lenovo Group Ltd., which last year overtook Hewlett-Packard Co. as the world’s largest PC maker by units sold, is setting a new precedent with its aggressive global expansion in smartphones.

Tencent Holdings Ltd., owns the WeChat smartphone application. Launched in late 2010, WeChat dominates China’s mobile messaging market and the majority of the app’s 272 million monthly active users are in China. But last year, it spent $200 million on overseas ad campaigns to push WeChat into many markets including India, South Africa, Spain and Italy. Tencent says the app has more than 100 million downloads abroad. WeChat was ahead of competitors in offering an easy-to-use feature for sending recorded voice messages and it is challenging the dominance of Silicon Valley’s WhatsApp, which has more than 300 million monthly active users globally.

Tencent’s share price nearly doubled last year and its market capitalization of $123 billion isn’t far from Facebook Inc.’s $139 billion market value.

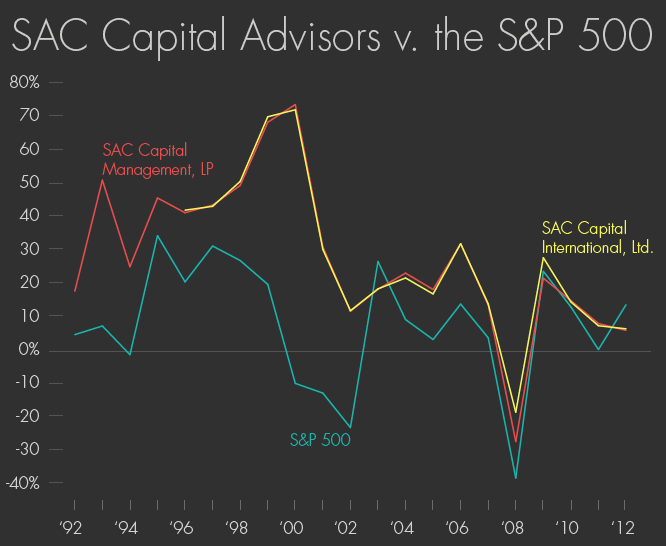

The fall of SAC

Frontline special: To Catch a Trader – The fall of king of hedge fund, SAC.

Fantastic journalism and story.

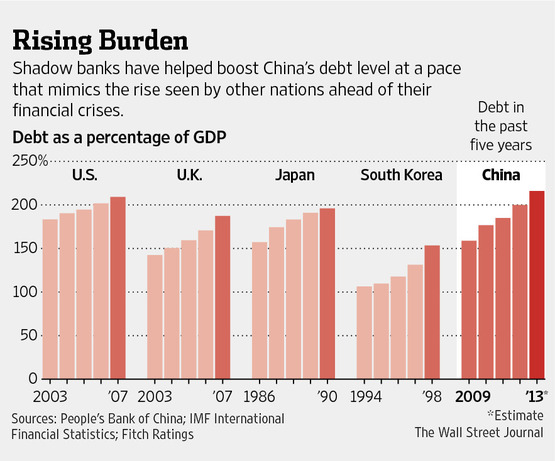

China’s debt boom will have consequence

China’s policy makers are facing a real challenge to deal with the fast and furious debt buidup. The comparison below is alarming.

(graph courtesy of WSJ)

Now, it looks as if China’s stimulus plan enacted during 2008-09 period may have just postponed the crisis, not killed it. As we say, there is no free lunch.

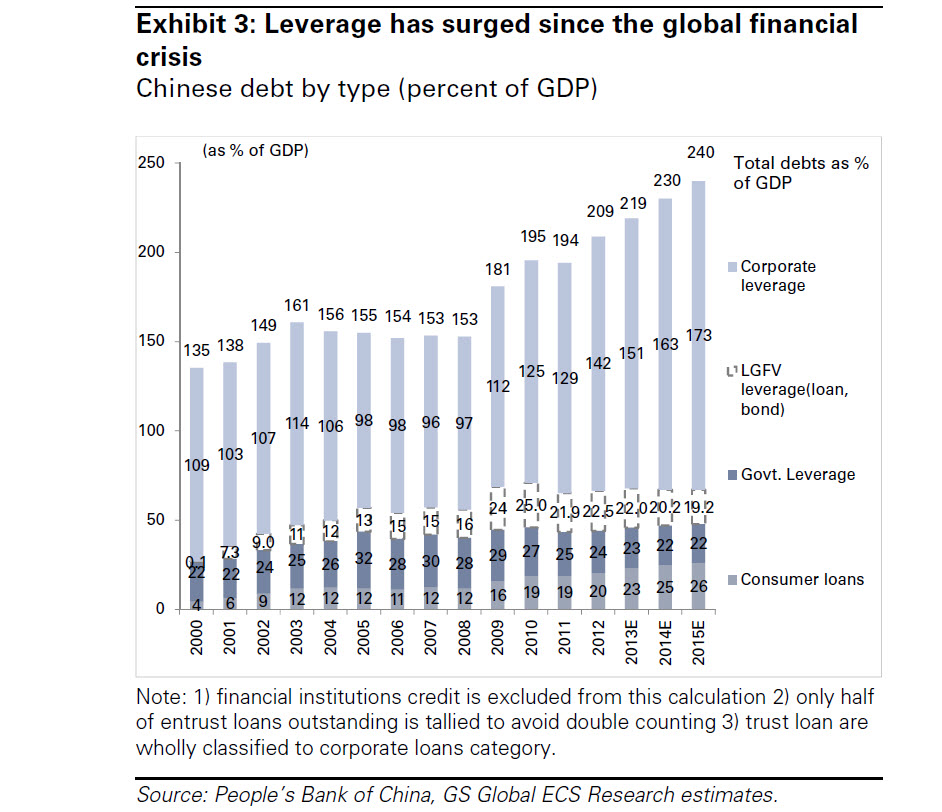

A recent report from Goldman Sachs shows that most debt, more than 70%, is concentrated in the corporate sector. My hunch is that most of the leverage in the corporates came from large state-owned enterprises (SOEs), or investment vehicles created by local governments, the so-called LGFVs. See the chart below (courteys of GS).

Bob Shiller on bubbles and psychology

This was an interview in last December from PBS.

Bob Shiller: The whole idea that the stock market reflects fundamentals is, I think, wrong. It really reflects psychology. The aggregate stock market reflects psychology more than fundamentals.

Shiller also pointed out why economists at the Fed will not call it a bubble even when they see it – This has something to do with group think and self-censorship.