Home » Posts tagged 'bubble'

Tag Archives: bubble

Bob Shiller on bubbles and psychology

This was an interview in last December from PBS.

Bob Shiller: The whole idea that the stock market reflects fundamentals is, I think, wrong. It really reflects psychology. The aggregate stock market reflects psychology more than fundamentals.

Shiller also pointed out why economists at the Fed will not call it a bubble even when they see it – This has something to do with group think and self-censorship.

China is leveraging up

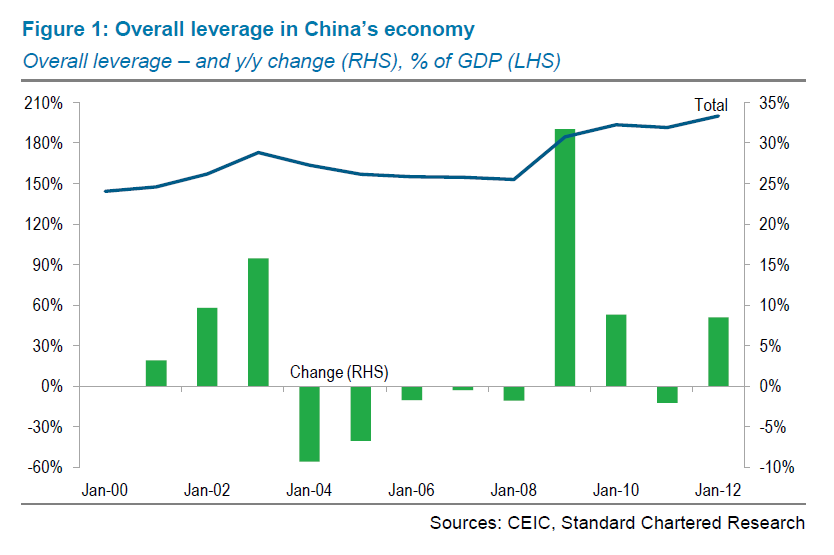

While the rest of the world is going through a deleveraging process, China has been leveraging up. Its economy is getting bubbly.

According to research by Standard Chartered Bank, China’s overall leverage ratio (the sum of the leverage of government, corporate and household) now reached 210% of GDP, rising from a rather high level 150% of GDP in early 2000s.

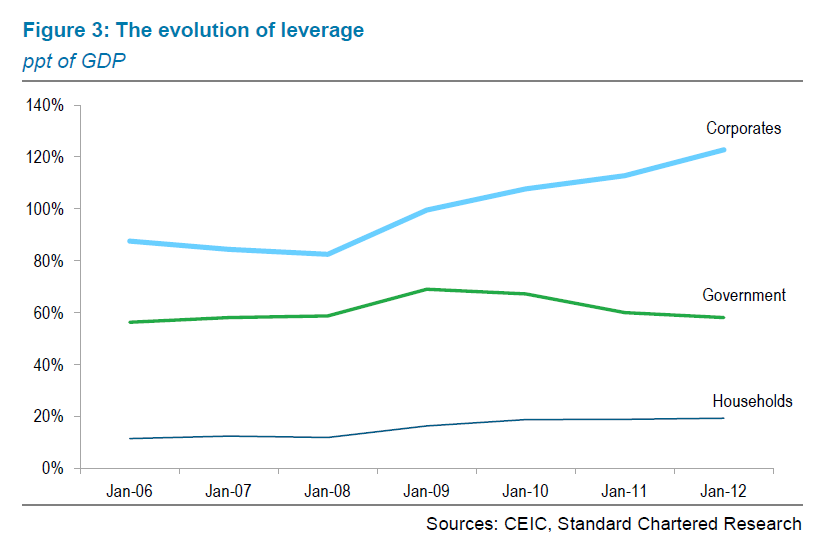

Dividing the overall leverage ratio in into three sub-components, we see the biggest increase came from the corporate sector: the ratio in that sector has increased from 80% of GDP at the beginning of the Great Recession to around 130% of GDP today.

Most of the leveraged-up corporations are SOEs. They are the natural candidates to respond quickly to government’s call for stimulus spending in the aftermath of the financial crisis during 2007-2009.

Besides SOEs, local governments also created all sorts of firms outside of government’s (and bank’s) balance sheet, the so-called local-government-investment-vehicles, or LGIVs. This is Chinese version of shadow banking system. My sense is that they have contributed a great deal to China’s housing bubble.

Can China keep on going?

Do you feel everything is progressing in China? Or rather China is like a fast car without a reverse gear, destined to crash?

Watch this interesting video analysis, featuring Michael Pettis.

(video courtesy of Journeymanpictures)

Microlending: India’s subprime chaos

I posted a piece about two years ago warning about the danger of a microfinance bubble in the developing world. Now the Indian version of US subprime crisis came into fruition.

WSJ reports that the microlending fueled by high-yield hungry investment banks and private equity firms has caused an upheaval in India.

The microlending movement that was supposed to help lift millions of people in India out of poverty has in recent weeks fallen into chaos.

Urged on by local government officials and politicians, thousands of borrowers have simply stopped paying lenders, even though they have the money. The government has begun ratcheting up restrictions, fearing that borrowers are being buried by usurious interest rates. In some cases, officials have even arrested lending agents for allegedly harassing borrowers.

…the unfettered expansion was leading to poor lending practices, multiple loans to the same borrowers, and fears of widespread repayment problems.

![[IMICRO]](https://sg.wsj.net/public/resources/images/MI-BG735A_IMICR_NS_20101028184935.gif)

American bond in bubble?

Jeremy Siegle thinks YES,

Ten years ago we experienced the biggest bubble in U.S. stock market history—the Internet and technology mania that saw high-flying tech stocks selling at an excess of 100 times earnings. The aftermath was predictable: Most of these highfliers declined 80% or more, and the Nasdaq today sells at less than half the peak it reached a decade ago.

A similar bubble is expanding today that may have far more serious consequences for investors. It is in bonds, particularly U.S. Treasury bonds. Investors, disenchanted with the stock market, have been pouring money into bond funds, and Treasury bonds have been among their favorites. The Investment Company Institute reports that from January 2008 through June 2010, outflows from equity funds totaled $232 billion while bond funds have seen a massive $559 billion of inflows.

We believe what is happening today is the flip side of what happened in 2000. Just as investors were too enthusiastic then about the growth prospects in the economy, many investors today are far too pessimistic.

The rush into bonds has been so strong that last week the yield on 10-year Treasury Inflation-Protected Securities (TIPS) fell below 1%, where it remains today. This means that this bond, like its tech counterparts a decade ago, is currently selling at more than 100 times its projected payout.

Shorter-term Treasury bonds are yielding even less. The interest rate on standard noninflation-adjusted Treasury bonds due in four years has fallen to 1%, or 100 times its payout. Inflation-adjusted bonds for the next four years have a negative real yield. This means that the purchasing power of this investment will fall, even if all coupons paid on the bond are reinvested. To boot, investors must pay taxes at the highest marginal tax rate every year on the inflationary increase in the principal on inflation-protected bonds—even though that increase is not received as cash and will not be paid until the bond reaches maturity.

…

Those who are now crowding into bonds and bond funds are courting disaster. The last time interest rates on Treasury bonds were as low as they are today was in 1955. The subsequent 10-year annual return to bonds was 1.9%, or just slightly above inflation, and the 30-year annual return was 4.6% per year, less than the rate of inflation.

Furthermore, the possibility of substantial capital losses on bonds looms large. If over the next year, 10-year interest rates, which are now 2.8%, rise to 3.15%, bondholders will suffer a capital loss equal to the current yield. If rates rise to 4% as they did last spring, the capital loss will be more than three times the current yield. Is there any doubt that interest rates will rise over the next two decades as the baby boomers retire and the enormous government entitlement programs kick into gear?

With future government finances so precarious, private asset accumulation and dividend income must become the major sources of retirement funding. At current interest rates, government bonds will not be the answer. One hundred times earnings was the tipping point for the tech market a decade ago. We believe that the same is now true for government bonds.

Paul Krugman thinks NO.

Here’s a thought for all those insisting that there’s a bond bubble: how unreasonable are current long-term interest rates given current macroeconomic forecasts? I mean, at this point almost everyone expects unemployment to stay high for years to come, and there’s every reason to expect low or even negative inflation for a long time too. Shouldn’t that imply that the Fed will keep short-term rates near zero for a long time? And shouldn’t that, in turn, mean that a low long-term rate is justified too?

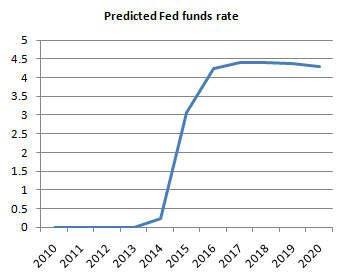

Now, take the CBO projection, which calls for unemployment to fall very slowly, and core inflation to stay low for quite a while too. Here’s what it implies for the Fed funds rate, taking the zero lower bound into account:

That’s right: four years of near-zero short-term interest rates. Does a 10-year rate of 2.6 percent still sound so unreasonable? And bear in mind that I’m not using some doomsayer’s forecast; I’m using the staid folks at the CBO.

…

Here’s what I think is going on: aside from the obviously intense desire of some of the bond bubble folks to see a fiscal crisis — they’ve been planning for it, and they’re not going to take no for an answer — my sense is that a lot of people just can’t bring themselves to face the reality that we’re likely to be in a zero-interest world for a long time. They just keep assuming that the Fed is going to raise rates soon, even though there is absolutely nothing about the macro situation that would justify such a rate increase.

David Rosenberg uses “bubble-rule-of thumb” and he quotes John Rogue:

“We don’t believe there is any “bond bubble”. However, there is a bubble in people believing there is a “bond bubble”. Here’s how you will know if there is a bond bubble — ask your colleagues how many of them own bonds in their personal accounts. When nobody/almost nobody raises their hand you should be comforted in knowing that the prospects of the existence of a “bond bubble” have been reduced. By the way, this tactic has worked wonderfully for gold over the last decade.”

China – bubble or no bubble?

China’s real estate bubble is of great concern to many people. Today, I want to entertain you with two contrast views on China’s real estate and housing market.

First group holds the view that China is experiencing no asset bubble in housing market, or, similar to Japan in 1970s, the sharp rising of housing price is a reflection of strong housing demands coming from high population density and rapid urbanization.

An example of this is a recent report from US Global Investors:

No Housing Bubble in China

By John Derrick, Director of Research

China’s housing market is hot, but it’s not a bubble on the verge of bursting, as many contend.

Before we can discuss why it’s not a bubble, a little background on the Chinese housing market is needed.

Prior to the early 1990s, urban dwellers in China were provided an apartment by their employers or the government, with rent set at less than 5 percent of their salary (utilities included). Starting in the early 1990s, the government began to privatize housing by selling apartments to their residents at a low price. Almost overnight it created a private home ownership rate of about 70 percent.

This policy change was also a vast redistribution of wealth from the government to the people – those apartments typically occupied prime downtown locations, and thus are worth at least the price of a new luxury apartment.

The price of housing in China has risen as the economy has expanded, but the chart from BCA Research shows that housing price growth has been significantly slower than GDP growth since the late 1980s.

The price of housing has roughly doubled since the late 1990s, but it’s important to remember that China’s prices have risen from a much lower base than in the developed countries (among them, Britain, Ireland and Spain) in which bubbles were created. It’s also relevant to point out that household disposable income in China more than doubled during the period. The rise of the Chinese middle class is a major global economic phenomenon – tens of millions of people are added each year.

Leverage is also an important indicator in judging how susceptible a housing market is to growing into a bubble. The chart below, also from BCA Research, shows debt as a percentage of disposable income in China and in a number of developed-market countries. More than half of the developed countries had debt in excess of income, with Denmark and Ireland pushing 200 percent.

China is at the far other end, with debt totaling just 44 percent of disposable income.

Furthermore, homebuyers in China put down at least 20 percent as a down payment (30 percent for a first-time buyer and 40 percent for a second-home buyer to damp down speculation). These buyers rarely fall behind on their mortgage payments.It’s obviously true that there has been rapid price appreciation in major cities like Shanghai and Beijing. Prices have risen above the affordability level for most families in these cities, and that is why the government is acting to let some air out of those markets before dangerous bubbles form.

For example, the government’s “second mortgage rule” requiring much higher down payments is having some effect – in January, price appreciation rose less than 1 percent month-over-month, down from a 2.1 percent jump in December. The government has also ordered that developers build more economical homes.

Where does the China housing market go from here? Home inventories are low in major cities – at the current sales pace, there are only a few months worth of inventory in Shanghai, and the situation isn’t much better in Beijing or Shenzhen (see chart below).

But demand is still strong. A recent survey by the Hong Kong-based brokerage CLSA found that 56 percent of China’s middle-class families are considering buying a new home – despite the higher prices many families can pay a 30 percent down payment because of their higher savings.

Our own research shows that property developers, coming off a good 2009, are expanding into second- and third-tier cities, where housing markets are also growing and prices are more affordable.

This widening of opportunity, combined with the government’s early recognition that decisive measures were needed, together will raise the probability that it will achieve its goal of slowing down home price increases without causing the market to collapse.

Another report comparing Japan and China from BoJ (Bank of Japan) also holds the similar view.

Here is the Chinese version and English version of the BoJ report. (h/t Yuki Masujima).

The other group, including myself, holds the view that China has a big real estate bubble waiting to burst. The only uncertainty is how big the impact will be.

I argued many times before that because China is at a much different development level than Japan was, thus with much higher growth potential, meanwhile China is still closed to free international capital flows, the damage of the bubble burst won’t affect China’s long-term growth projection, i.e., in China, there won’t be a lost decade similar to what happened in Japan and the U.S.

To demonstrate the key insights of the views for the second group, here I recommend two pieces:

1. NYT report on short seller Jim Chanos on his big bet against China.

2. In this Charlie Rose interview (one of my favorite shows), Jim Chanos elaborate why he’s shorting China, and what he’s been watching on China bubble.

This is a highly recommended piece,

(click to play in new window, about 30 mins)

China bubble getting deflated…

Recent bubble pricking measures by China’s policy makers have had a big impact on the price of China’s real estate market. I think in general this is healthy for China – the earlier the bubble got deflated, the less damage will the bubble bursting do to the Chinese economy. As I said before, China stands at the forefront of bubble containing experiment. Let’s see how far the government measures can go…but so far, I like what I have seen.

Here is the latest report from WSJ.

The global economic recovery has drawn support from a swift rebound in China. Now, investors and economists wonder whether a bursting Chinese property bubble could put China’s economy in a bind.

![[AINVEST]](https://sg.wsj.net/public/resources/images/AM-AI974_AINVES_NS_20100420132601.gif)

Over the past week, China’s cabinet has announced measures aimed at cracking down on property speculators, including tougher down-payment requirements for second and third homes. This comes after China reported an 11.7% rise in urban home prices last month from a year earlier, its fastest gain in five years.

“This is the critical policy point that finally cracks the Chinese property market,” declared Morgan Stanley China strategist Jerry Lou.

All this could be seen as bolstering the case for short-seller James Chanos. The name of Mr. Chanos’s $6 billion hedge fund, Kynikos Associates LP, means “cynic” in Greek—appropriate since the New York-based money manager earlier this year made himself the world’s best-known cynic when it comes to China’s growth story.

“What we’re talking about is a world-class, if not the, world-class property bubble,” Mr. Chanos said in an interview with Charlie Rose, comparing conditions in Chinese cities to Dubai and Miami. He predicts the bubble will begin to unravel later this year.

Mr. Chanos argues that China’s lending spree during the financial crisis has pumped too much money into real estate, and that housing prices have surpassed affordability.

Among the counter-arguments: China’s growing wealth feeds a long-term demand to upgrade the country’s housing stock, and regulators put a tight cap on loan-to-value ratios, limiting the downside of any bubble. Some note that China’s government, using measures such as those announced in the last week, has long avoided a crash in housing prices.

Those inclined to favor Mr. Chanos’s analysis—or who at least believe that some kind of correction is likely—could try to emulate his strategy. He is betting on a decline in the price of Hong Kong-listed Chinese property developers and other companies linked to China’s property market, such as those exporting cement and copper to China.

![Reblog this post [with Zemanta]](https://img.zemanta.com/reblog_e.png?x-id=9b3c4ae9-df28-423e-95a0-b28bac57edd0)

China’s bubble pricking experiment, part 2

More update after my previous post on China’s curbing on real estate bubble: