Home » bubble

Category Archives: bubble

fools, and greater fools

’60 minutes’ investigates the recent development of Chinese housing bubble in the following video.

Following my previous posts (here, here, here, here and here) on China’s housing bubble, I am now re-organizing my thoughts, and starting to work out a formal economic analysis on China’s housing bubble.

Specifically, I will address the question if the current housing price in China can be justified by the story of China’s fast economic growth coupled with her fast industrialization and urbanization. My initial analysis clearly says no. I call this a ‘fools-and-greater-fools’ theory. In history, great bubbles always came with even greater stories. China is no exception.

Will keep you guys posted.

Can China keep on going?

Do you feel everything is progressing in China? Or rather China is like a fast car without a reverse gear, destined to crash?

Watch this interesting video analysis, featuring Michael Pettis.

(video courtesy of Journeymanpictures)

China’s housing bubble at its extreme

Ordos, the little known prairie city in China’s inner-Mongolia autonomous region, now has become the extreme example of China’s housing bubble. Due to extreme housing speculations and land sale (mostly grassland), loads of local farmers became instant millionaires: its GDP per capita recently surpassed Hong Kong; people with assets of 1 million Yuan (or $150,000) are actually considered “poor”; in 2010, 90% sale of Land Rovers (the symbol for power and masculinity in Chinese taste) in mainland China found its buyers in Ordos…and imagine a cleaning lady driving a Toyota Land Cruiser to work?

I am shocked by this video news from SOHU (in Chinese):

You may also watch a similar Youtube video in English, but with less drama:

All this can’t be due to China’s fast economic growth. This is simply not sustainable. I see a classic asset bubble forming, reminiscent of many bubbles in history. It will burst eventually no matter what.

America in releveraging?

America’s financial sector is still undergoing the deleveraging process – Big banks are busy in repairing their balance sheets, gradually writing off their losses in housing bubble era.

But with Fed’s super easy monetary policy and easy access to the dirt cheap credit, there seems to be a divergence in terms of attitude toward credit. The main street corporate America now is the one who carries the credit torch forward. With interest rate expected only to rise (not fall), America’s corporations are borrowing like there is no tomorrow. This is being reflected in the junk bond market, where yields again fell close to the 2007-level low.

Is another credit bubble in the making? Are we going to see a flurry of corporate defaults in coming years? Is the Fed just delaying the inevitable?

This FT video may offer you some insights to the issue.

(click to play the video)

Locate China’s housing bubble

Housing market tends to be local. It’s rare to see a nationwide price decline. The recent US housing bubble is an exception and often considered a black swan.

People have been talking about China’s housing bubble for a few years now (see my previous post on China’s housing bubble debate), but where exactly is the bubble located?

The recent NBER research sheds some light on the issue. The graph below shows the price-to-income ratio of China’s eight major cities, from 1999 to Q1 of 2010.

(click to enlarge, source: NBER w16189)

Beijing and Shenzhen are clearly in bubble-shape — the typical and familiar parabolic surge in price, and they are followed by Shanghai and Hangzhou.

Now, let’s have some comparative perspective. How the same ratio compares to the major cities in the United States.

The graph below (courtesy of Infectious Greed) shows the price-to-income ratio of US cities. San Francisco, Los Angeles, Seattle were among the highest.

(click to enlarge)

At the peak of the housing bubble between 2006-07, the same ratio for San Francisco, the highest among all US cities, was around 11. In contrast, Beijing has a ratio of 18, and Shenzhen at astonishing 22.

QE= money printing = debased dollar = asset bubbles

Interview of Jim Grant:

Microlending: India’s subprime chaos

I posted a piece about two years ago warning about the danger of a microfinance bubble in the developing world. Now the Indian version of US subprime crisis came into fruition.

WSJ reports that the microlending fueled by high-yield hungry investment banks and private equity firms has caused an upheaval in India.

The microlending movement that was supposed to help lift millions of people in India out of poverty has in recent weeks fallen into chaos.

Urged on by local government officials and politicians, thousands of borrowers have simply stopped paying lenders, even though they have the money. The government has begun ratcheting up restrictions, fearing that borrowers are being buried by usurious interest rates. In some cases, officials have even arrested lending agents for allegedly harassing borrowers.

…the unfettered expansion was leading to poor lending practices, multiple loans to the same borrowers, and fears of widespread repayment problems.

![[IMICRO]](https://sg.wsj.net/public/resources/images/MI-BG735A_IMICR_NS_20101028184935.gif)

American bond in bubble?

Jeremy Siegle thinks YES,

Ten years ago we experienced the biggest bubble in U.S. stock market history—the Internet and technology mania that saw high-flying tech stocks selling at an excess of 100 times earnings. The aftermath was predictable: Most of these highfliers declined 80% or more, and the Nasdaq today sells at less than half the peak it reached a decade ago.

A similar bubble is expanding today that may have far more serious consequences for investors. It is in bonds, particularly U.S. Treasury bonds. Investors, disenchanted with the stock market, have been pouring money into bond funds, and Treasury bonds have been among their favorites. The Investment Company Institute reports that from January 2008 through June 2010, outflows from equity funds totaled $232 billion while bond funds have seen a massive $559 billion of inflows.

We believe what is happening today is the flip side of what happened in 2000. Just as investors were too enthusiastic then about the growth prospects in the economy, many investors today are far too pessimistic.

The rush into bonds has been so strong that last week the yield on 10-year Treasury Inflation-Protected Securities (TIPS) fell below 1%, where it remains today. This means that this bond, like its tech counterparts a decade ago, is currently selling at more than 100 times its projected payout.

Shorter-term Treasury bonds are yielding even less. The interest rate on standard noninflation-adjusted Treasury bonds due in four years has fallen to 1%, or 100 times its payout. Inflation-adjusted bonds for the next four years have a negative real yield. This means that the purchasing power of this investment will fall, even if all coupons paid on the bond are reinvested. To boot, investors must pay taxes at the highest marginal tax rate every year on the inflationary increase in the principal on inflation-protected bonds—even though that increase is not received as cash and will not be paid until the bond reaches maturity.

…

Those who are now crowding into bonds and bond funds are courting disaster. The last time interest rates on Treasury bonds were as low as they are today was in 1955. The subsequent 10-year annual return to bonds was 1.9%, or just slightly above inflation, and the 30-year annual return was 4.6% per year, less than the rate of inflation.

Furthermore, the possibility of substantial capital losses on bonds looms large. If over the next year, 10-year interest rates, which are now 2.8%, rise to 3.15%, bondholders will suffer a capital loss equal to the current yield. If rates rise to 4% as they did last spring, the capital loss will be more than three times the current yield. Is there any doubt that interest rates will rise over the next two decades as the baby boomers retire and the enormous government entitlement programs kick into gear?

With future government finances so precarious, private asset accumulation and dividend income must become the major sources of retirement funding. At current interest rates, government bonds will not be the answer. One hundred times earnings was the tipping point for the tech market a decade ago. We believe that the same is now true for government bonds.

Paul Krugman thinks NO.

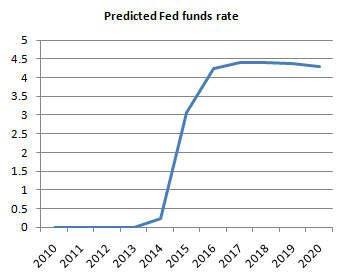

Here’s a thought for all those insisting that there’s a bond bubble: how unreasonable are current long-term interest rates given current macroeconomic forecasts? I mean, at this point almost everyone expects unemployment to stay high for years to come, and there’s every reason to expect low or even negative inflation for a long time too. Shouldn’t that imply that the Fed will keep short-term rates near zero for a long time? And shouldn’t that, in turn, mean that a low long-term rate is justified too?

Now, take the CBO projection, which calls for unemployment to fall very slowly, and core inflation to stay low for quite a while too. Here’s what it implies for the Fed funds rate, taking the zero lower bound into account:

That’s right: four years of near-zero short-term interest rates. Does a 10-year rate of 2.6 percent still sound so unreasonable? And bear in mind that I’m not using some doomsayer’s forecast; I’m using the staid folks at the CBO.

…

Here’s what I think is going on: aside from the obviously intense desire of some of the bond bubble folks to see a fiscal crisis — they’ve been planning for it, and they’re not going to take no for an answer — my sense is that a lot of people just can’t bring themselves to face the reality that we’re likely to be in a zero-interest world for a long time. They just keep assuming that the Fed is going to raise rates soon, even though there is absolutely nothing about the macro situation that would justify such a rate increase.

David Rosenberg uses “bubble-rule-of thumb” and he quotes John Rogue:

“We don’t believe there is any “bond bubble”. However, there is a bubble in people believing there is a “bond bubble”. Here’s how you will know if there is a bond bubble — ask your colleagues how many of them own bonds in their personal accounts. When nobody/almost nobody raises their hand you should be comforted in knowing that the prospects of the existence of a “bond bubble” have been reduced. By the way, this tactic has worked wonderfully for gold over the last decade.”