Home » Economy (Page 29)

Category Archives: Economy

Housing: rent or buy?

Housing, on a national level, has become much more affordable (see chart below). But housing market is always local. If you are not sure whether it’s a good time to buy vs. rent a house, you are not alone.

(graph courtesy of Northern Trust)

A yardstick to look at is the house-price/rent ratio – generally it’s good time to buy if the rent ratio is well below 20. Here is a list of rent ratios of major U.S. cities as of Q4 of 2009.

(click on the graph to enlarge; source: NYT)

Also , read this article from NYT, “In Sour Home Market, Buying Often Beats Renting“

Does SEC have a real case against Goldman?

Hear legal and investment experts on the issue:

China – bubble or no bubble?

China’s real estate bubble is of great concern to many people. Today, I want to entertain you with two contrast views on China’s real estate and housing market.

First group holds the view that China is experiencing no asset bubble in housing market, or, similar to Japan in 1970s, the sharp rising of housing price is a reflection of strong housing demands coming from high population density and rapid urbanization.

An example of this is a recent report from US Global Investors:

No Housing Bubble in China

By John Derrick, Director of Research

China’s housing market is hot, but it’s not a bubble on the verge of bursting, as many contend.

Before we can discuss why it’s not a bubble, a little background on the Chinese housing market is needed.

Prior to the early 1990s, urban dwellers in China were provided an apartment by their employers or the government, with rent set at less than 5 percent of their salary (utilities included). Starting in the early 1990s, the government began to privatize housing by selling apartments to their residents at a low price. Almost overnight it created a private home ownership rate of about 70 percent.

This policy change was also a vast redistribution of wealth from the government to the people – those apartments typically occupied prime downtown locations, and thus are worth at least the price of a new luxury apartment.

The price of housing in China has risen as the economy has expanded, but the chart from BCA Research shows that housing price growth has been significantly slower than GDP growth since the late 1980s.

The price of housing has roughly doubled since the late 1990s, but it’s important to remember that China’s prices have risen from a much lower base than in the developed countries (among them, Britain, Ireland and Spain) in which bubbles were created. It’s also relevant to point out that household disposable income in China more than doubled during the period. The rise of the Chinese middle class is a major global economic phenomenon – tens of millions of people are added each year.

Leverage is also an important indicator in judging how susceptible a housing market is to growing into a bubble. The chart below, also from BCA Research, shows debt as a percentage of disposable income in China and in a number of developed-market countries. More than half of the developed countries had debt in excess of income, with Denmark and Ireland pushing 200 percent.

China is at the far other end, with debt totaling just 44 percent of disposable income.

Furthermore, homebuyers in China put down at least 20 percent as a down payment (30 percent for a first-time buyer and 40 percent for a second-home buyer to damp down speculation). These buyers rarely fall behind on their mortgage payments.It’s obviously true that there has been rapid price appreciation in major cities like Shanghai and Beijing. Prices have risen above the affordability level for most families in these cities, and that is why the government is acting to let some air out of those markets before dangerous bubbles form.

For example, the government’s “second mortgage rule” requiring much higher down payments is having some effect – in January, price appreciation rose less than 1 percent month-over-month, down from a 2.1 percent jump in December. The government has also ordered that developers build more economical homes.

Where does the China housing market go from here? Home inventories are low in major cities – at the current sales pace, there are only a few months worth of inventory in Shanghai, and the situation isn’t much better in Beijing or Shenzhen (see chart below).

But demand is still strong. A recent survey by the Hong Kong-based brokerage CLSA found that 56 percent of China’s middle-class families are considering buying a new home – despite the higher prices many families can pay a 30 percent down payment because of their higher savings.

Our own research shows that property developers, coming off a good 2009, are expanding into second- and third-tier cities, where housing markets are also growing and prices are more affordable.

This widening of opportunity, combined with the government’s early recognition that decisive measures were needed, together will raise the probability that it will achieve its goal of slowing down home price increases without causing the market to collapse.

Another report comparing Japan and China from BoJ (Bank of Japan) also holds the similar view.

Here is the Chinese version and English version of the BoJ report. (h/t Yuki Masujima).

The other group, including myself, holds the view that China has a big real estate bubble waiting to burst. The only uncertainty is how big the impact will be.

I argued many times before that because China is at a much different development level than Japan was, thus with much higher growth potential, meanwhile China is still closed to free international capital flows, the damage of the bubble burst won’t affect China’s long-term growth projection, i.e., in China, there won’t be a lost decade similar to what happened in Japan and the U.S.

To demonstrate the key insights of the views for the second group, here I recommend two pieces:

1. NYT report on short seller Jim Chanos on his big bet against China.

2. In this Charlie Rose interview (one of my favorite shows), Jim Chanos elaborate why he’s shorting China, and what he’s been watching on China bubble.

This is a highly recommended piece,

(click to play in new window, about 30 mins)

Lowenstein: The future of Wall Street

Interview of Roger Lowenstein, author of “When Genius Failed: The Rise and Fall of Long-Term Capital Management” and “Buffett: The Making of an American Capitalist.”

Link to the interview, about 45 mins. A good history review of what went wrong.

Jereme Grantham on bubbles

It’s always good to listen to Jereme Gratham, co-founder of Boston-based GMO. Here’s his recent piece on asset bubbles.

(click to play, source: FT)

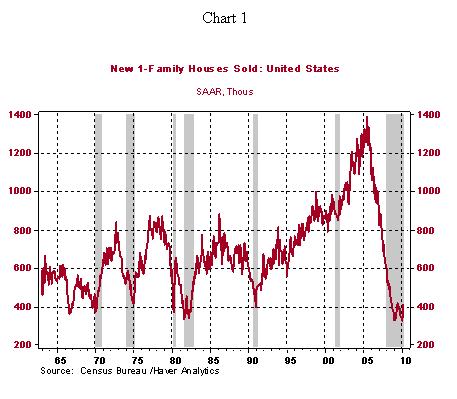

New home sales up big time, but don’t get too excited

Sales of new homes increased 27% in March, the biggest monthly increase in 47 years. The sharp jump was largely due to the fact that the first-time home buyer credit program is going to expire on April 30.

As seen in the chart below (graph courtesy of Northern Trust), the level of new home sales in March (411,000) still remains slightly below the July 2009 mark, or 70% below the peak recorded in July 2005.

Also watch this video interview of Mark Zandi, Chief Economist at Moody’s Economy.com, on the housing market outlook.

Is a Greek default inevitable?

Things are getting worse. There are also signs of contagion to other fiscally-weak countries in Europe.

Here is the latest development from WSJ that traders are betting Greece will eventually default.

Greek bond prices posted a drastic decline Thursday as traders began betting a debt default is inevitable, even if the country receives a massive bailout.

The Greek bond market is now priced for a "catastrophic event," says Sebastien Galy, senior foreign-exchange strategist at BNP Paribas.

Greece's woes helped sink the euro to an 11-month low before the common currency recovered some of its losses.

Although conditions in the Greek bond market have generally been deteriorating over the past several weeks, Thursday's session saw an especially steep decline in short-term debt prices. As a result, the yield on Greek two-year notes jumped to more than 12% from 8.3% Wednesday, according to Tradeweb.

At those levels, the prices are suggesting that "even if [Greece] finds a solution, if you buy two-year bonds, you may not be getting all your money back," says Mark Schofield, global head of interest-rate strategy at Citigroup in London.

Meanwhile, yields on 10-year Greek bonds rose to 8.92%, almost six percentage points over comparable German debt. That gap is the widest since Greek joined the euro zone. Just two weeks ago, that spread stood closer to four percentage points.

The backdrop for the selloff was still more bad news for Greece. The European Union's statistical authority said Greece's 2009 budget deficit was worse than had been previously reported, and politicians in Germany ramped up their opposition to a Greek bailout.

Meanwhile, Moody's Investors Service downgraded Greece's debt rating and warned that additional cuts could be on the way.

The woes in the Greek bond market also are spilling over to other European nations with fiscal problems, such as Portugal, Spain and, to a lesser extent, Italy. Traders say the selloffs in those markets to some degree reflect a sentiment that bond prices in those markets hadn't been reflecting the poor fundamentals of those countries.

For much of April, even as the Greek bond market began to collapse, prices on the other Mediterranean countries' debt had been relatively stable. On April 1, for example, the gap, or spread, between German and Portuguese two-year debt stood at less than 0.6 percentage point, almost the same as U.S. Treasury debt.

But in the past week, the Portuguese spread has risen sharply, hitting 1.83 percentage points Thursday from 0.83 percentage point a week ago. Spain's two-year spreads widened 0.82 percentage point Thursday from 1.38 percentage points Wednesday.

'We're seeing contagion," says Citigroup's Mr. Schofield, who noted that the impact of Greece was also being seen in a widening between the prices at which bonds could be bought and sold. "I don't think those countries are an immediate default risk to the same extent as Greece … but these are countries where the fiscal backdrop is very poor."

With financial markets focused on the prospect of a debt default by the Greek government, the International Monetary Fund fretted aloud this week about the prospects for a sovereign-debt crisis, focusing on Europe.

In a report this week, the IMF said Portugal, and to a lesser extent Spain and Italy, would be the most likely to suffer from contagion if Greece goes over the edge.

IMF's contagion analysis noted that Ireland, in the line of fire a year ago over its own fiscal woes, would escape the worst of a Greek default. Investors appear to believe Ireland has acted pre-emptively and decisively to get the deficit under control, analysts noted.

To avoid Greece's plight, says Uri Dadush, a former World Bank official now at the Carnegie Endowment in Washington, Italy too should move aggressively to cut its budget deficit by a further 4% of gross domestic product over three years, and engineer a 6% real devaluation through wage cuts and economic reforms.

"I think the broad policy recommendations have general applicability in Spain, too," he said.

On Thursday, the damage from Greece also spread to the currency markets, where the euro slid as low as $1.3257, its lowest level since May 2009. By day's end the euro had rebounded slightly and was changing hands at $1.3314, from $1.3399 Wednesday.

BNP's Mr. Galy says one potential silver lining is that many European banks may have reduced their exposure to Greece.

"Risk managers seem to have hit the panic button on anything that was left," he says. "That's good from a systemic point of view."

Many investors say there are just too many headwinds for Greece to overcome, and that even a bailout won't be an end to the crisis.

"The problem is likely going to come back in 2011 and 2012," says Michael Hasenstab, manager of the Templeton Global Bond Fund. "You get in this vicious cycle, and it's a very difficult situation."

China becoming world’s top green technology market

China and Germany are leading in the world’s clean energy market:

Here is my prediction – wherever the energy constraints and demands are the greatest (think about China’s huge population and its energy demands to fuel its fast economic growth), the most likely you will find technology breakthroughs and innovations there.

The logic of my view is explained in this classic video by economist Julian Simon,