Home » Employment

Category Archives: Employment

US Labor market update

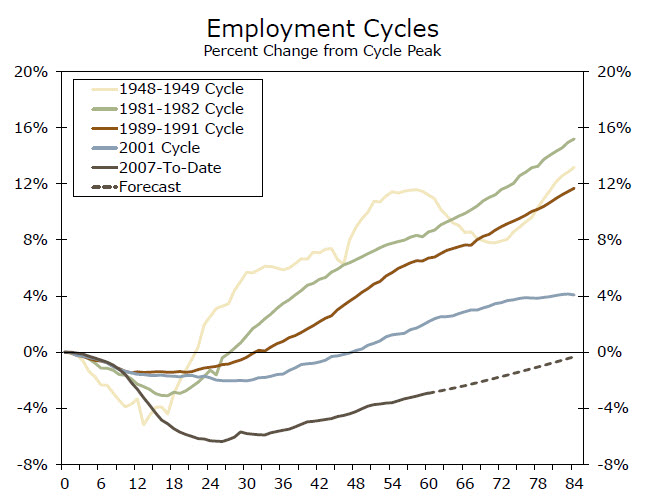

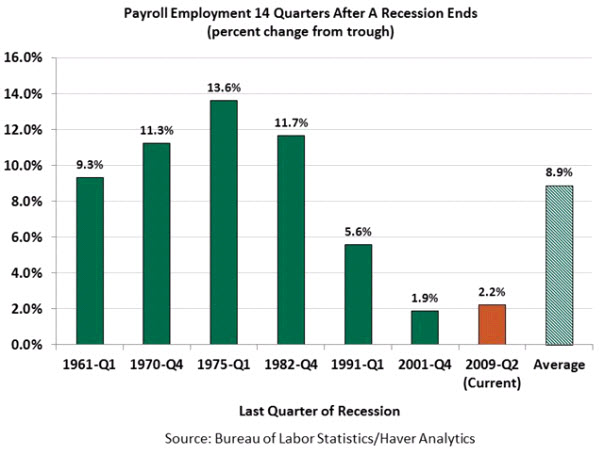

At tepid pace in monthly employment gains, this labor market recovery has been similar to the recovery after 2001 recession, if not much worse. Two charts to put the current labor market condition in comparative perspective – another “jobless recovery”.

(graph courtesy of Wells Fargo Economics)

(graph courtesy of Northern Trust)

Why still no robust employment recovery?

Gary Becker summarizes the reasons for the slow job recovery into three categories:

1. The aftermath of a big financial crisis, as explained by the research done by Reinhart and Rogoff;

2. Policy and regulation uncertainties hinder investment, although Corporate America are flooded with cash;

3. Relatively more generous unemployment benefits offer no immediate incentives for job seeking, keeping a non-negligible proportion of population out of labor force.

(graph courtesy of Calculated Risk)

America’s Lost Decade, part 4

This is a post following my previous posts on the same topic, see p1, p2, p3.

When discussing the issue, most people focus on GDP growth. Yes, in terms of GDP growth, in the past decade, the US still managed to grow 18%, cumulatively – that’s roughly 1.8 percent per year on average. However, in terms of employment growth, it has been a lost decade for the US (see the chart below).

(click to enlarge)

Given the economic dynamism in the US, and compare it to Japan, I have long thought the Lost Decade would never happen in America, a land full of opportunities.

I guess I need to re-visit my presumptions — Whether a big housing bubble (in the US’ case, two big bubbles in one decade) always foretells anemic economic growth afterward, as opposed to the common belief that Japan’s lost decade was largely due to policy mistakes. Maybe, in the aftermath of a big bubble, America and Japan are really not that much different – an open question.

Job Perspective of America’s Lost Decade

I posted a little while ago on America’s lost decade in terms of investment returns (also this post), here below is a nice graph summarizing job creation by decade: The past decade was clearly a lost decade in job creation. Also read my previous post on this here.

Firms with job openings

Percentage of firms with job openings:

(click to enlarge)

Higher productivity at the expense of labor

Labor productivity grew 9.5% last quarter. This growth came at the expense of laying off workers massively, and squeezing the current workers who still have their jobs. You can complain but you dare not jump ships as the labor market is still very soft.

High productivity growth is typical at the end of recession and at the beginning of recovery. But because firms cut employees more quickly and aggressively during this recession, current workers feel especially squeezed.

The productivity of U.S. workers surged in the third quarter, as the economy resumed growing even as employers pushed forward with layoffs and cuts in working hours across a wide range of industries.

The Labor Department said the output per hour of nonfarm workers rose at an annual rate of 9.5% in the quarter, more than four times the average productivity growth rate of the past quarter-century. When taken together with the second quarter’s 6.9% rise, it was the strongest productivity growth rate over a six-month period since 1961.

(click to enlarge)

The source of the productivity boom is straightforward. Firms are continuing to cut costs even as the economy heals, meaning they are getting more from existing work forces. Nonfarm output rose at a 4% annual rate in the third quarter while hours worked decreased at a 5% annual rate, the department said.

While unemployment remains high, corporate profits have bounced back from the shock of 2008. If output keeps climbing, employment should follow — and reduce productivity growth from the third quarter’s rate.

Big productivity gains are common at the end of recessions and the beginning of recoveries. The usual pattern is productivity grows first, then employment rises, and finally wages increase.

The productivity gains should prevent an outbreak of inflation even though the Federal Reserve has held short-term interest rates near zero and pumped $1 trillion into the financial system through loans and securities purchases. In normal times, so much monetary stimulus would push consumer prices much higher.

The Labor Department reported that unit labor costs — a measure of what it costs firms to pay workers for a single unit of output they produce — fell at a 5.2% annual rate in the quarter. They are down 3.6% from a year ago, the steepest drop since the Labor Department began keeping records in 1945.

“The combination of rapidly increasing productivity and falling unit labor costs puts downward pressure on inflation, and should make the Fed more comfortable about pursuing accommodative monetary policy amidst economic growth,” J.P. Morgan economists said in a note to clients.

(click to enlarge)

The productivity of workers is a linchpin to an economy’s health and growth potential. The U.S. economy went through a productivity drought in the 1970s and ’80s and a resurgence in the late ’90s. It slowed sharply between 2004 and 2008.

Though the latest jump could be the start of a new upturn, there are reasons to doubt that the latest rebound can be sustained. The financial shock of 2008 could debilitate a key part of the economy — the financial sector. The regulatory reshuffling that the crisis has produced could also sap the productivity of some industries. Moreover, business investment has fallen sharply, which has held back a key driver of productivity growth in the past — business use of new technologies.

Some analysts said businesses might start investing more now. “Faster productivity growth will support profits, and could lead to a more vigorous rebound in capital spending than envisaged,” Jared Franz, an analyst at T.Rowe Price, said in a commentary on the report.

A separate report by the Labor Department suggested that the intensity of layoffs could be waning. The department said new claims for unemployment benefits decreased by 20,000 to 512,000 in the week ended Oct. 31. That is the lowest level since Jan. 3. The previous week’s level was revised to 532,000. These are still high levels but appear to be on a downtrend.

The four-week moving average of new claims, which aims to smooth volatility in the data, fell by 3,000 to 523,750 from the previous week’s revised figure of 526,750. That is the lowest level since Jan. 10.

The U.S. employment report for October, out on Friday, is expected to show that the jobless rate stayed close to a 26-year high of 9.8% in September.

![Reblog this post [with Zemanta]](https://img.zemanta.com/reblog_e.png?x-id=1ef014db-7b2c-4e8f-be45-04157376c1f1)