Home » history

Category Archives: history

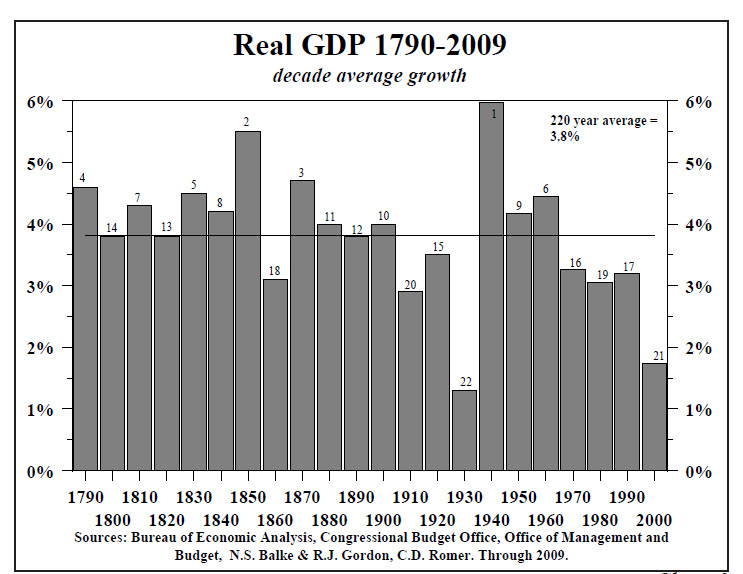

US economic growth for the last 200 years

The below graph shows the average growth rate by decade in the US since 1790. The recent decade, 2000-2009, ranks the bottom 2nd. The only worse decade was 1930s. This helps to put a lot of things into perspective.

(Note: the small number on the bar indicates the ranking; graph courtesy of Hoisington Investment Management)

Ferguson on global re-convergence

Economic historian Naill Ferguson on the six “killer apps” (or institutions) in the West that generated the Great Divergence since 1700s, up until the recent rise of China. And he argues that gap between the West and the East is coming to an end, with China fast catching up with the West, leading to a re-convergence of the world economy.

In the interview, Naill Ferguson had many claims in his sharp observation of the history. However, despite being deeply intriguing, most of his claims remain to be just hypotheses. As a China watcher, I am not so certain at this moment that China’s surpassing of the US on per capita income level is inevitable, although I am positive that China’s total GDP will pass the US in no time.

For readers who are interested in the topic of the Great Divergence and Re-convergence, I would recommend two additional readings: The first is a classic by Ken Pomeranz, “The Great Divergence: China, Europe, and the Making of the Modern World Economy“; and the second is by Ian Morris, “Why the West Rules -For Now.”

Making sense of China

Martin Jacques explains the three building blocks in understanding China, and how China is fundamentally different from the West.

This is one of the videos worth watching, and I’d highly recommend it. Although I am not a believer of those grand projections into the future, Martin got his facts about China very right.

Lessons from 1937’s double-dip

With economic recovery looking on track, what lessons can be learned from the 1937-stalled recovery — the double-dip contraction? (source: WSJ). This is a followup to my previous post “The lessons of 1937“.

WASHINGTON — A few months ago, Obama administration officials were sounding the alarm about another 1929. These days, it’s 1937 that has them in a sweat.

The Great Depression was W-shaped. The stock-market collapse led to a steep economic decline. But by 1933, the economy had rebounded. Then a series of monetary and fiscal blunders drove the country back into a deep recession at the end of 1937.

![[history lessons]](https://s.wsj.net/public/resources/images/NA-AZ916_OUTLOO_NS_20090823173250.gif)

That episode is at the heart of the debate over how quickly the government and the U.S. Federal Reserve should unwind the emergency measures they have taken to fend off a Depression-like contraction.

For the administration, the answer is clear: Err on the side of continued expansionary policies. “What you learned from that episode in 1937 is that it’s not enough to be recovering,” says Christina Romer, chairman of the president’s Council of Economic Advisers and an expert on the Great Depression. “You don’t want to do anything when you start recovering that nips it off too soon.”

For fiscal conservatives, the answer is equally clear: Start cutting the federal deficit and slowing the growth in the money supply now, before the binge generates a burst of inflation.

Ms. Romer is “sending the absolutely wrong message — that we can’t do anything to worry about inflation until the recovery is locked in because of concern for unemployment,” says Allan H. Meltzer, a political economist at Carnegie Mellon University. “The reason economists and central bankers have two eyes is so they can do two things at once.”

The economy was recovering briskly during Franklin D. Roosevelt’s first term in the White House. The jobless rate, which had peaked at 25% in 1933, fell to 14% in 1937 — not exactly cause for celebration but a relief nonetheless.

The comeback stalled in 1937. Banks, nervous about the fragile recovery, were holding huge amounts of cash in reserve at the Fed. Fearing an inflationary surge should the banks decide to lend that money out to businesses and individuals, the Fed — which had made the mistake of tightening monetary policy soon after the 1929 stock-market crash — miscalculated again. The Fed ratcheted up banks’ reserve requirements three times, starting in 1936. The banks reacted by cutting lending even further.

“There’s no doubt that [Fed Chairman Ben] Bernanke is heavily influenced by these two mistakes of the Fed during the Depression and is absolutely intent on not repeating them,” says Alex J. Pollock of the American Enterprise Institute, a free-market think tank in Washington.

Compounding the Fed’s errors, the federal government tightened fiscal policy. Congress approved a big bonus for World War I veterans in 1936, providing a spark of consumer spending. But lawmakers allowed the subsidy to lapse in 1937. At the same time, the government began collecting the first Social Security taxes, on top of income and capital-gains tax increases that Mr. Roosevelt approved in 1934-35.

Tightening the monetary and fiscal screws sent the economy into free fall again — the second trough of the W. Unemployment shot up to 19%, prolonging the nation’s suffering.

Fast-forward to 2009. Most economists surveyed by The Wall Street Journal this month believe that the recession is over. On average, they expect to see a 2.4% increase in output in the third quarter, at a seasonally adjusted annual rate. Construction of new single-family homes has started to climb. Auto sales are up.

But administration officials and their allies fear a second dip if the government pulls back the $787 billion stimulus or if the Fed clamps down too soon.

“I think it’s a fringe view to say we should get rid of the stimulus,” says Ms. Romer. Economists who say the economy is on the upswing do so because they assume a continued fiscal boost through 2010, she says.

“Even though the Fed is talking about and obviously doing internal planning for the exit strategy, nobody should think it’s imminent,” says Princeton University economist Alan Blinder, a former Fed vice chairman and economic adviser to the Clinton White House. “And it shouldn’t be imminent; the Fed has got to have its pedal to the metal for some time yet.”

Mr. Meltzer says the risk lies not in pulling back too soon but dithering too long. And he would scrap the stimulus program immediately and replace it with cuts in marginal tax rates for individuals and businesses. “It’s certainly not a bad idea to get rid of a policy that isn’t working,” he says. “It takes courage, but that’s what we pay these people to do.” And, he says, the Fed should now slow the growth of the money supply.

Conservative voices in Congress are sending the same message. Last week, Sen. Jon Kyl, an Arizona Republican, reiterated his view that the rebounding economy renders further stimulus spending superfluous.

This week the Obama administration and Congressional Budget Office are to release new federal deficit forecasts. The White House projection is expected to be a record $1.58 trillion for the year ending Sept. 30, and the congressional forecast could be even larger. Expect the news to prompt an outcry from those who believe that the inflation of the 1970s is now a bigger risk than the deflation of the 1930s.