Home » Inflation

Category Archives: Inflation

Andy Xie on China’s inflation outlook

Interview of Andy Xie, former Morgan Stanley Chief China economist.

Pay attention to his view that raising interest rate will have limited effect on containing inflation because it may prick the housing bubble. This is especially true when considering local governments’ huge stake in keeping housing and land prices high.

I expect Chinese government will resort more to raising bank reserves and administrative measures to contain inflation.

Three other things are also likely to happen:

1) Chinese government may distort official inflation numbers, i.e., more human smoothing.

2) Accelerate Yuan’s appreciation, which I think is most likely. In fact, Qing Wang of Morgan Stanley expects the RMB to appreciate from currently 6.64 to 6.2 by Dec. 2011. Marty Feldstein, in my earlier post, echoed the similar view.

3) tighter capital control to prevent inflow of hot money.

More broader picture is that the super easy monetary policy by the Fed is propping asset bubbles everywhere in the world, especially in the fast growing emerging economies (carry trade factor). Besides China, Brazil also faces grim inflation outlook, and Brazilian interest rate is already above 10% and expected to rise further.

Commodity prices are already high and fast rising. But given the debasement of paper currency across board, and the grim inflation outlook in emerging markets, it’s reasonable to believe commodities are set to rise further.

Higher volatility is ahead of us; expect to see more booms and busts; and China is facing another real challenge.

Why China wanted to peg US dollar?

Let’s put aside for now the debate on whether Chinese Yuan is undervalued or not, what are the motives for China to fix its currency to the US dollar around 1995?

First comes to my mind is the need to remove currency risk in trade. As we know, almost all trade contracts are denominated in dollar, not in Yuan. Currencies tend to move a lot, and nobody likes volatility. By pegging Yuan to the dollar, Chinese firms essentially save the cost from buying expensive currency risk hedging contracts.

Second, by fixing Yuan to the dollar, more or less, China submitted its monetary policy to the Fed, i.e., the Fed’s monetary policy tends to have a great impact on China’s own monetary policy. In other words, China’s central bank largely lost its autonomy. Good thing or bad?

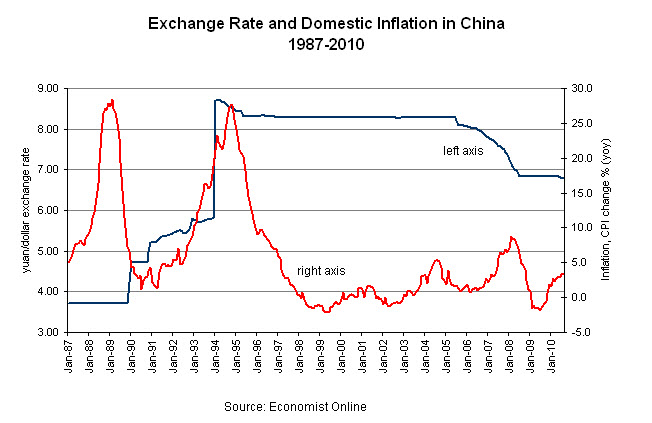

Below is a chart I just made looking at China’s domestic inflation, an important gauge for macro-stability, before and after the pegging to the US dollar.

(click on the graph to enlarge)

The chart is very dramatic. Before 1995, China’s inflation (in red) was very high and volatile. The Great Inflation in 1988 partly contributed to the 1989 students’ demonstration, which eventually led to the unfortunate Tian’anmen incident. After 1995, China’s inflation plummeted, and since then has remained quite stable – inflation never went up to over 10% again.

Was this because Chinese government suddenly improved their macro economy management skills? I don’t think so.

Here is what really happened – In essence, China achieved its macro-stability by outsourcing its monetary policy to the Fed, which has much more experiences in fighting inflation and also enjoys better credibility.

(update on Oct. 7, 2011)

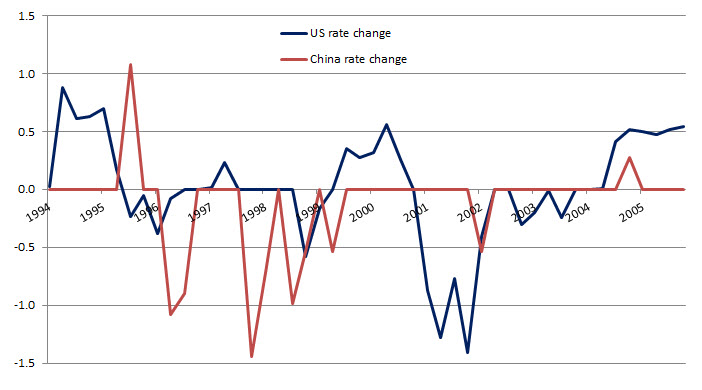

A re-look at the interest rate changes during 1995-2005 between China and the US, I changed my view that China’s inflation decline was due to its pegging to the US dollar. The more plausible explanation is China’s central bank successfully prevented inflation from rising by continuously raising interest rate, eventually pushing down inflation.

Deflation watch

An update of US core CPI in three different measurements:

(click to enlarge; graph courtesy of calculatedrisk)

The trend is not comforting…

Deflation Threat: Is America another Japan?

Does America face Japanese-style deflation?

China is leading world into inflation

China is the first to lead the world economy out of recession, and now it is the first leading the world into high inflation.

Massive government stimulus and money printing will put emerging economies on the inflation alert first, then developed economies will follow suit. I don’t believe governments and central banks can time well when to raise interest rate — the bias toward lower unemployment will almost guarantee interest rates will be raised too slowly, and too late.

Also read former Morgan Stanley Asia Chief Economist Andy Xie’s comments on the outlook of inflation in the world (in Chinese).

![Reblog this post [with Zemanta]](https://img.zemanta.com/reblog_e.png?x-id=22fc3968-0453-47a8-bda7-8b161c4a3f68)

Start to feel inflation in China

China’s central bank raised it’s inter-bank lending rate, showing worries about inflation pressure in the economy. The graph below from new order PMI clearly demonstrates the pressure has built up in most sectors.

One of the areas of concern in China’s PMI report was the rise of input prices by 3.3 points to 66.7. This is an indicator of rising inflationary pressures. This, coupled with the rise in food prices, should be monitored closely in the coming months.

![Reblog this post [with Zemanta]](https://img.zemanta.com/reblog_e.png?x-id=bb7b20c9-aa29-4579-9edc-8669f4b8c7e7)

World gold rush continues…

(click to enlarge)

Gold rush

Analysis of recent rise of gold price (source: FT)

(click to play the video)