Home » Posts tagged 'bond'

Tag Archives: bond

American bond in bubble?

Jeremy Siegle thinks YES,

Ten years ago we experienced the biggest bubble in U.S. stock market history—the Internet and technology mania that saw high-flying tech stocks selling at an excess of 100 times earnings. The aftermath was predictable: Most of these highfliers declined 80% or more, and the Nasdaq today sells at less than half the peak it reached a decade ago.

A similar bubble is expanding today that may have far more serious consequences for investors. It is in bonds, particularly U.S. Treasury bonds. Investors, disenchanted with the stock market, have been pouring money into bond funds, and Treasury bonds have been among their favorites. The Investment Company Institute reports that from January 2008 through June 2010, outflows from equity funds totaled $232 billion while bond funds have seen a massive $559 billion of inflows.

We believe what is happening today is the flip side of what happened in 2000. Just as investors were too enthusiastic then about the growth prospects in the economy, many investors today are far too pessimistic.

The rush into bonds has been so strong that last week the yield on 10-year Treasury Inflation-Protected Securities (TIPS) fell below 1%, where it remains today. This means that this bond, like its tech counterparts a decade ago, is currently selling at more than 100 times its projected payout.

Shorter-term Treasury bonds are yielding even less. The interest rate on standard noninflation-adjusted Treasury bonds due in four years has fallen to 1%, or 100 times its payout. Inflation-adjusted bonds for the next four years have a negative real yield. This means that the purchasing power of this investment will fall, even if all coupons paid on the bond are reinvested. To boot, investors must pay taxes at the highest marginal tax rate every year on the inflationary increase in the principal on inflation-protected bonds—even though that increase is not received as cash and will not be paid until the bond reaches maturity.

…

Those who are now crowding into bonds and bond funds are courting disaster. The last time interest rates on Treasury bonds were as low as they are today was in 1955. The subsequent 10-year annual return to bonds was 1.9%, or just slightly above inflation, and the 30-year annual return was 4.6% per year, less than the rate of inflation.

Furthermore, the possibility of substantial capital losses on bonds looms large. If over the next year, 10-year interest rates, which are now 2.8%, rise to 3.15%, bondholders will suffer a capital loss equal to the current yield. If rates rise to 4% as they did last spring, the capital loss will be more than three times the current yield. Is there any doubt that interest rates will rise over the next two decades as the baby boomers retire and the enormous government entitlement programs kick into gear?

With future government finances so precarious, private asset accumulation and dividend income must become the major sources of retirement funding. At current interest rates, government bonds will not be the answer. One hundred times earnings was the tipping point for the tech market a decade ago. We believe that the same is now true for government bonds.

Paul Krugman thinks NO.

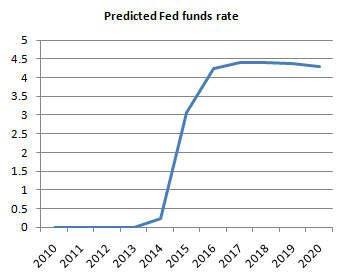

Here’s a thought for all those insisting that there’s a bond bubble: how unreasonable are current long-term interest rates given current macroeconomic forecasts? I mean, at this point almost everyone expects unemployment to stay high for years to come, and there’s every reason to expect low or even negative inflation for a long time too. Shouldn’t that imply that the Fed will keep short-term rates near zero for a long time? And shouldn’t that, in turn, mean that a low long-term rate is justified too?

Now, take the CBO projection, which calls for unemployment to fall very slowly, and core inflation to stay low for quite a while too. Here’s what it implies for the Fed funds rate, taking the zero lower bound into account:

That’s right: four years of near-zero short-term interest rates. Does a 10-year rate of 2.6 percent still sound so unreasonable? And bear in mind that I’m not using some doomsayer’s forecast; I’m using the staid folks at the CBO.

…

Here’s what I think is going on: aside from the obviously intense desire of some of the bond bubble folks to see a fiscal crisis — they’ve been planning for it, and they’re not going to take no for an answer — my sense is that a lot of people just can’t bring themselves to face the reality that we’re likely to be in a zero-interest world for a long time. They just keep assuming that the Fed is going to raise rates soon, even though there is absolutely nothing about the macro situation that would justify such a rate increase.

David Rosenberg uses “bubble-rule-of thumb” and he quotes John Rogue:

“We don’t believe there is any “bond bubble”. However, there is a bubble in people believing there is a “bond bubble”. Here’s how you will know if there is a bond bubble — ask your colleagues how many of them own bonds in their personal accounts. When nobody/almost nobody raises their hand you should be comforted in knowing that the prospects of the existence of a “bond bubble” have been reduced. By the way, this tactic has worked wonderfully for gold over the last decade.”

Treasury current is shifting, part 2

From WSJ (April 5, 2010):

The 10-year Treasury yield, the benchmark for U.S. consumer and corporate borrowing, rose to 4% for the first time since June.

The move extends a steady increase by Treasury yields, which move inversely to prices, lifted by a combination of stronger economic data and the barrage of debt issued by the government to meet its financing needs. Recent Treasury auctions have met with much weaker demand and Monday’s move comes ahead of more auctions this week, with the Treasury Department set to sell $82 billion of Treasury notes and bonds.The 10-year yield is a key benchmark for mortgage rates and other consumer and corporate lending.

My best take on the surge of 10-year rate is: this is due to more of investors’ early worry about US fiscal situation and rising long-term inflation expectation; rather than expectation of strong economic recovery.

Remember, the Fed can’t directly control long-term interest rate. IF the 10-y rate continues to rise as the result of rising inflation expectation, the Fed will be forced to raise short-term interest rate. This will put a brake on the tepid economic recovery, potentially causing a double-dip scenario, like the recession in 1981.

Now watch this great debate on the issue, between Jim Grant and Dave Rosenberg, on the topic whether “Treasury is for losers”…

Jim Grant holds the view that high inflation is ahead of us, and Rosenberg thinks deflation is a bigger risk, so treasury/bond securities are not bad bet.

(click to play, about 50 mins)