Home » Posts tagged 'Monetary policy' (Page 3)

Tag Archives: Monetary policy

QE2: a cost benefit analysis

Martin Feldstein, former President of NBER, argues on FT that QE2 will have limited chance of success. Given the huge bank excess reserves in the system already, the marginal benefit of pumping another $1 trillion excess reserves is low. Fed’s main objective is to raise people’s inflation expectations so that real interest rate can go negative, a way of simulating the economy when facing the zero lower bound of nominal interest rate.

The Fed uses standard inflation measure, core PCE. But the excessively easy monetary policy will pop up asset prices across broad – oil, corn, cotton, gold, to name a few. The super easy monetary policy is also likely to create asset bubbles in emerging markets, laying the seeds for global instability in the future.

Like all bubbles, these exaggerated increases can rapidly reverse when interest rates return to normal levels. The greatest danger will then be to leveraged investors, including individuals who bought these assets with borrowed money and banks that hold long-term securities. These risks should be clear after the recent crisis driven by the bursting of asset price bubbles. Although the specific asset prices that are now rising are different from last time, the possibility of damaging declines when bubbles burst is worryingly similar.

The problem now extends to emerging markets, a group not directly affected in the last crisis. The lower US interest rates are causing a substantial capital flow to those economies, creating currency volatility. The economies hurt by the increasing value of their currencies are responding with measures to protect their exports and limit their imports, measures that could lead to trade conflict.

…

Although its real focus is on reducing unemployment, much of the rhetoric of Ben Bernanke, the Fed chairman, is about preventing deflation because some members of the Fed’s open market committee think the Fed should focus exclusively on price stability. But there is no deflation. Core consumer prices are rising and inflation is expected to average 2 per cent over the next 10 years.

Since short-term interest rates are already near zero, some economists advocate QE to reduce the real interest rate by raising inflation temporarily while holding the nominal interest rate unchanged. A 4 per cent expected rate of inflation for the next few years would turn a 1 per cent nominal interest rate into a real rate of minus 3 per cent, thereby stimulating interest-sensitive spending. But doing that would jeopardise the credibility of the Fed’s long-term inflation strategy.

Mr Bernanke’s argument for QE is based on the “portfolio balance” theory which stresses that, when the Fed buys bonds, investors increase their demand for other assets, particularly equities, raising their price and increasing household wealth and spending. Equity prices have already risen by 10 per cent since Mr Bernanke discussed this approach. But how much further will equity prices rise and what will that do to GDP?

Neither theory nor past experience can answer the first question. Much of the share price increase induced by QE may already have occurred based on expectations. An optimistic guess would be another 10 per cent. Since households have about $7,000bn in equities, that would imply a wealth gain of $700bn, raising consumer spending by about one-quarter of one per cent of GDP, a welcome but trivially small effect on incomes and employment.

The other ways in which QE would raise GDP are also small. A 20-basis-point reduction in mortgage rates would have little effect on homebuying at a time when house prices are again falling. The increase in banks’ liquidity would do nothing since banks already have massive excess reserves. Big corporations are sitting on vast amounts of cash. Small businesses that are not spending because they cannot get credit will not be helped, because the banks on which they depend have a shortage of capital.

The main reason behind the Fed’s action is to prevent Japan-like decade-long deflation. Given the uncertainties in forecasting, the Fed is willing to act proactively – the downside risk of deflation outweighs the risk of mild inflation, according to Jim Stock, professor at Harvard (see the video interview below). It’s assumed that the Fed can always act by raising interest rate when inflation reaches an uncomfortable level.

But something ignored here is the divergence of core inflation measure, preferred by the Fed, and the inflation in dollar-sensitive assets, such as oil, gold and commodities in general.

As pointed out by Marty, the cost-free borrowing at the short end is likely to rekindle the speculations and re-leveraging. Then 2003-2007 bubble just demonstrated how dangerous it can be when there is a sudden reversal of asset prices.

The mistake the Fed is committing now is their continuous ignorance of how monetary policy could fuel huge credit expansion and risk-taking, and help generate asset bubbles, one after another.

QE= money printing = debased dollar = asset bubbles

Interview of Jim Grant:

Stiglitz: Fed’s QE2 won’t work

Joe Stiglitz explains why the Fed’s easier monetary policy won’t work (source: WSJ):

The Federal Reserve, having done so much to create the problems in which the economy is now mired, having mistakenly thought that even after the housing bubble burst the problems were contained, and having underestimated the severity of the problem, now wants to make a contribution to preventing the economy from sinking into a Japanese-style malaise. How? As Chairman Ben Bernanke announced last week, through large-scale purchases of U.S. Treasurys—called quantitative easing, or QE.

The Fed is right to be worried.

If high unemployment continues, America faces the risk of losing human capital as the skills of the unemployed erode. It will then become increasingly difficult to bring the unemployment rate down to anywhere near the levels that prevailed in the mid- and late 1990s, and the higher unemployment rate and lower output will make the current pessimistic budget projections of the Congressional Budget Office and the Office of Management and Budget look rosy.

The problem is that, with interest rates already near zero, there is little the Fed can do to restart the economy—and doing the wrong thing can do considerable damage. In 2001, (then) record-low interest rates didn’t reignite investment in plant and equipment. They did, however, replace the tech bubble with an even more dangerous housing bubble. We are now dealing with the legacy of that bubble, with excess capacity in real estate and excess leverage in households.

Today, the Fed is paying too little attention to the transmission between the interest rates paid by government and the terms and availability of credit to small and medium-sized enterprises (SMEs). Large businesses are flush with cash, and small changes in interest rates—short-term or long—will affect them little. A banker rightly asks if such a business comes asking for money, “What’s wrong with it?”

But it is SMEs that are the source of job creation in most economies, including the U.S. Many of these enterprises are starved for cash. They can’t borrow money at the interest rate that big banks, big firms or government can. They borrow from banks, and many of the smaller local and community banks on which they depend are in dire straits—more than 800 are on the FDIC’s watch list.

Yet even if the banks were willing and able to lend, lending to SMEs is typically collateral-based, and the value of the most common form of collateral, real estate, has fallen 30% to 40%. No wonder then that credit availability is so constrained. But QE in the form of buying U.S. Treasurys is not likely to affect this much. It will have some effect in lowering mortgage rates, and lower mortgage rates will put a little more money into people’s pockets. Higher real-estate prices may also allow some SMEs to borrow more. But these effects, though positive, are likely to be small—so small as to make a barely perceptible difference in America’s persistent unemployment.

There is another channel through which easing will have some positive effects: Equity prices are likely to rise. But for all the reasons just given, this is unlikely to have much effect on investment. Nor will most Americans, burdened with debt and diminished retirement accounts, likely embark on much of a spending spree. Nor should they. Doing so would only delay the deleveraging that is necessary if we are to have sustainable growth going forward.

There is another downside risk: QE may not even succeed in lowering interest rates, or lowering them very much. Given the magnitude of excess capacity, there is little risk of inflation today. But if the inflation hawks come to believe that the risk of future inflation is real, then they’ll believe that short-term interest rates will rise. This will mean that long-term interest rates, even now, may actually rise, in spite of the massive Fed intervention, because long-term interest rates are based on expectations of future short-term interest rates.

QE poses a third risk: The bursting of the bond market bubble that the Fed is seeking to develop—the sequel to the tech and housing bubbles—will clearly have adverse effects on the economy, as we should have learned by now.

The advocates of QE point to another channel through which it will strengthen the economy: Lower interest rates may also lead to a weaker dollar, and the weaker dollar to more exports. Competitive devaluation engineered through low interest rates has become the preferred form of beggar-thy-neighbor policies in the 21st century. But this policy only works if other countries don’t respond. They will and have, through every instrument at their disposal. They too can lower interest rates. They can impose capital controls, taxes and bank regulations, and they can intervene directly in their exchange rate.

Under the gold standard, there was supposed to be an automatic adjustment mechanism, as a country with a trade surplus would see an inflow of gold and an increase in prices, leading to an automatic real appreciation of its currency. It never worked as smoothly as it was supposed to, but in the modern economy with fiat money, the adjustment processes can be short-circuited even more easily. China, for instance, has sufficient control of its banking system and economy that it can simultaneously maintain a stable exchange rate that generates a surplus and prevents inflation.

Such policies may come with a price, but the price may be less than the alternative: the bankruptcies and unemployment that would follow from disruptive currency appreciation as the U.S. lets forth a flood of liquidity. That money is supposed to reignite the American economy but instead goes around the world looking for economies that actually seem to be functioning well and wreaking havoc there.

The upside of QE is limited. The money simply won’t go to where it’s needed, and the wealth effects are too small. The downside is a risk of global volatility, a currency war, and a global financial market that is increasingly fragmented and distorted. If the U.S. wins the battle of competitive devaluation, it may prove to be a pyrrhic victory, as our gains come at the expense of others—including those to whom we hope to export.

Fed Boston Summit

First interview with Boston Fed President Eric Rosengren.

His main message I took away is, “with nominal interest rate fixed (near zero level), disinflation would be monetary tightening. Deflation would be even worse”. This offers enough reason for further monetary easing.

Also, one lesson learned from Japan was that monetary policy under “liquidity trap” should be proactive. The Fed’s monetary easing can’t afford to be nearly as gradual as Japan.

Second interview with John Taylor. According to Taylor Rule, current interest rate should be at .75%. He is not in favor of QE2.

The last interview with Jim Hamilton on how the Fed might affect long term interest rate through bond purchase.

Why China wanted to peg US dollar?

Let’s put aside for now the debate on whether Chinese Yuan is undervalued or not, what are the motives for China to fix its currency to the US dollar around 1995?

First comes to my mind is the need to remove currency risk in trade. As we know, almost all trade contracts are denominated in dollar, not in Yuan. Currencies tend to move a lot, and nobody likes volatility. By pegging Yuan to the dollar, Chinese firms essentially save the cost from buying expensive currency risk hedging contracts.

Second, by fixing Yuan to the dollar, more or less, China submitted its monetary policy to the Fed, i.e., the Fed’s monetary policy tends to have a great impact on China’s own monetary policy. In other words, China’s central bank largely lost its autonomy. Good thing or bad?

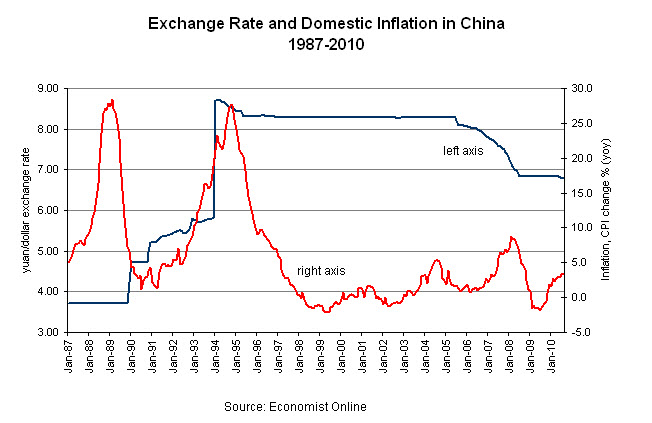

Below is a chart I just made looking at China’s domestic inflation, an important gauge for macro-stability, before and after the pegging to the US dollar.

(click on the graph to enlarge)

The chart is very dramatic. Before 1995, China’s inflation (in red) was very high and volatile. The Great Inflation in 1988 partly contributed to the 1989 students’ demonstration, which eventually led to the unfortunate Tian’anmen incident. After 1995, China’s inflation plummeted, and since then has remained quite stable – inflation never went up to over 10% again.

Was this because Chinese government suddenly improved their macro economy management skills? I don’t think so.

Here is what really happened – In essence, China achieved its macro-stability by outsourcing its monetary policy to the Fed, which has much more experiences in fighting inflation and also enjoys better credibility.

(update on Oct. 7, 2011)

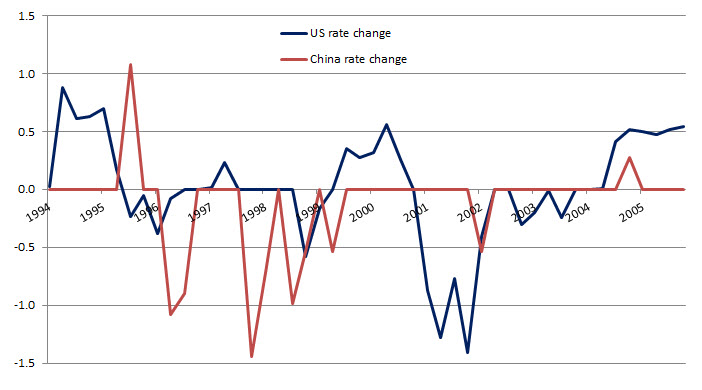

A re-look at the interest rate changes during 1995-2005 between China and the US, I changed my view that China’s inflation decline was due to its pegging to the US dollar. The more plausible explanation is China’s central bank successfully prevented inflation from rising by continuously raising interest rate, eventually pushing down inflation.

Allan Meltzer: We don’t need more excess reserves!

Allan Meltzer, author of several books on the history of US Federal Reserve, said with over 1 trillion $ excess reserves sitting on bank’s balance sheet, it would be stupid to add another 1 trillion dollars.

More monetary easing won’t be effective, the key is to remove the uncertainties in the economy so businesses can start investing again. Too much cash held by corporations, too little investment.

Big move in currency market again

Fear of Fed’s another round of quantitative easing, Euro shot up to the highest level since April,

and Gold is reaching $1300 per ounce.

And Chinese Yuan is also gradually appreciating against USD, now at 6.70 Yuan per USD. Just one week ago, it was at 6.78.