Minsky on financial instability

Stability is destabilizing.

BBC runs a 30-minute program on Minsky and why his insights matter.

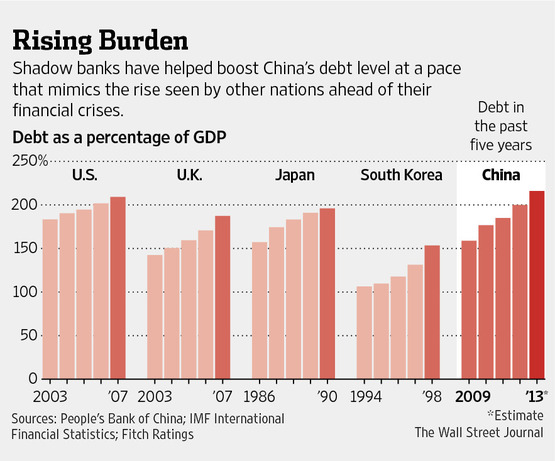

China’s debt boom will have consequence

China’s policy makers are facing a real challenge to deal with the fast and furious debt buidup. The comparison below is alarming.

(graph courtesy of WSJ)

Now, it looks as if China’s stimulus plan enacted during 2008-09 period may have just postponed the crisis, not killed it. As we say, there is no free lunch.

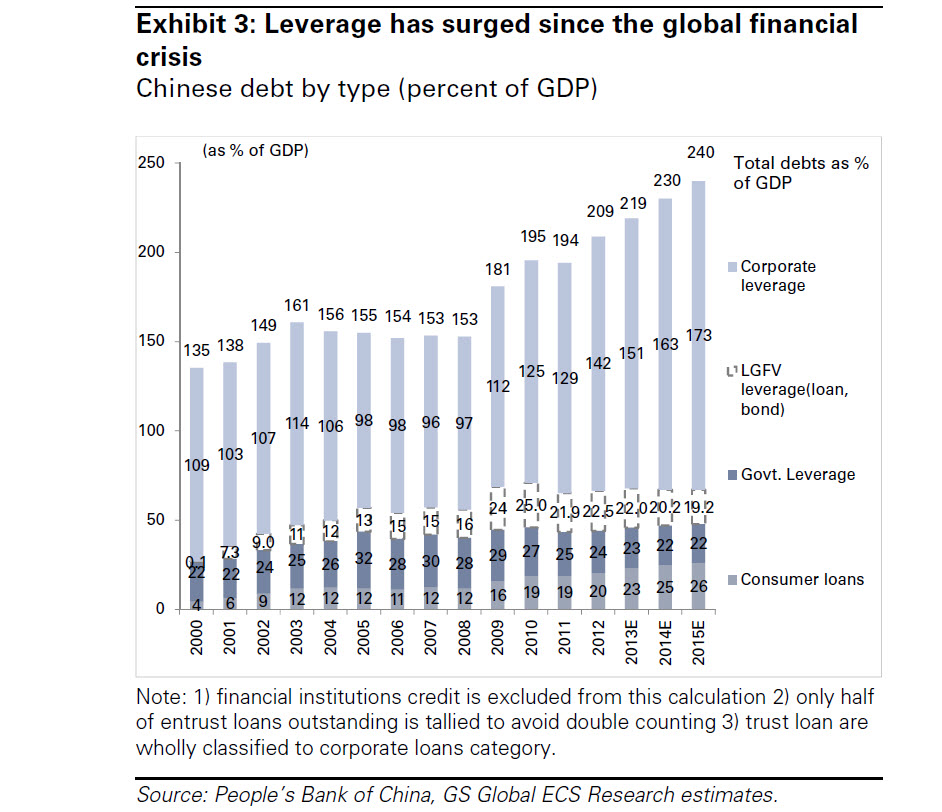

A recent report from Goldman Sachs shows that most debt, more than 70%, is concentrated in the corporate sector. My hunch is that most of the leverage in the corporates came from large state-owned enterprises (SOEs), or investment vehicles created by local governments, the so-called LGFVs. See the chart below (courteys of GS).

Bob Shiller on bubbles and psychology

This was an interview in last December from PBS.

Bob Shiller: The whole idea that the stock market reflects fundamentals is, I think, wrong. It really reflects psychology. The aggregate stock market reflects psychology more than fundamentals.

Shiller also pointed out why economists at the Fed will not call it a bubble even when they see it – This has something to do with group think and self-censorship.

Grantham: whipping the donkey

The latest Jeremy Gratham interview, with Charlie Rose. In this 50-min video interview, Jeremy talks about China and world’s energy price; his interesting experience with asset bubbles in the past (a frequent topic, but still refreshing), and his forecast of the US economic growth and stock market.

My favorite part is he analogized Fed’s monetary policy as whipping a donkey, trying to make the economy run faster like a race horse. 🙂 Quite accurate.

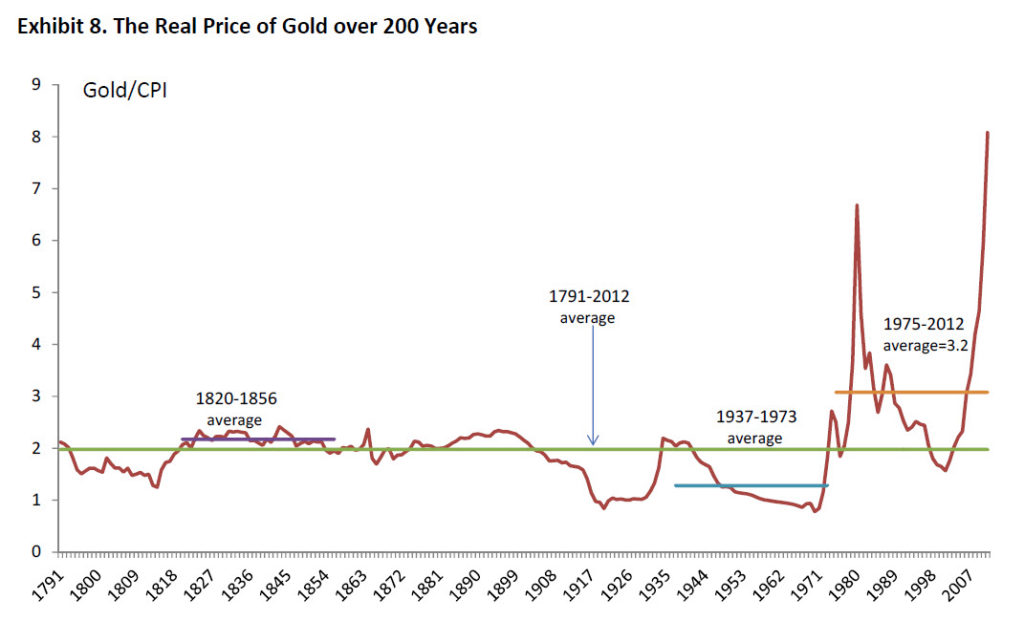

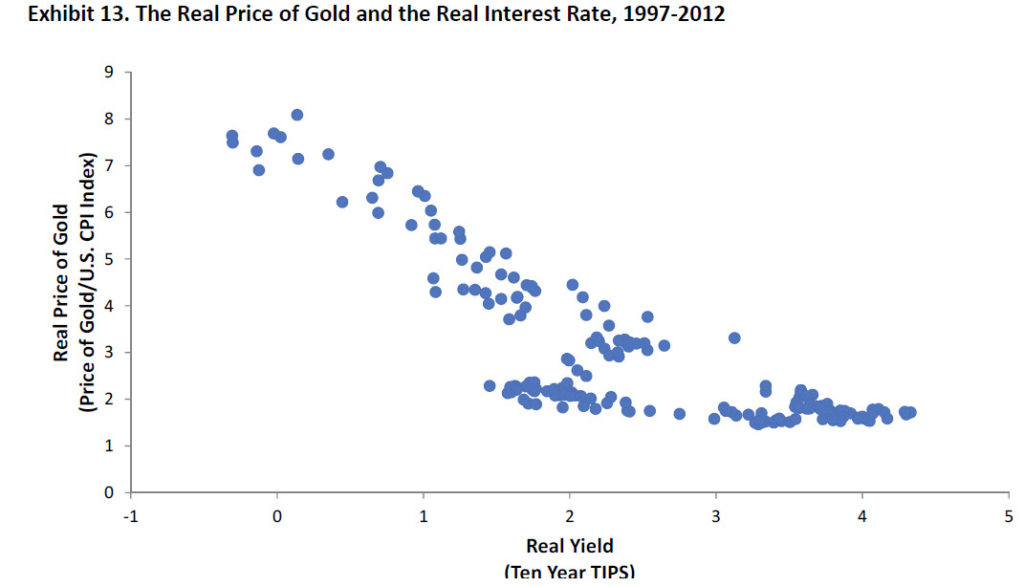

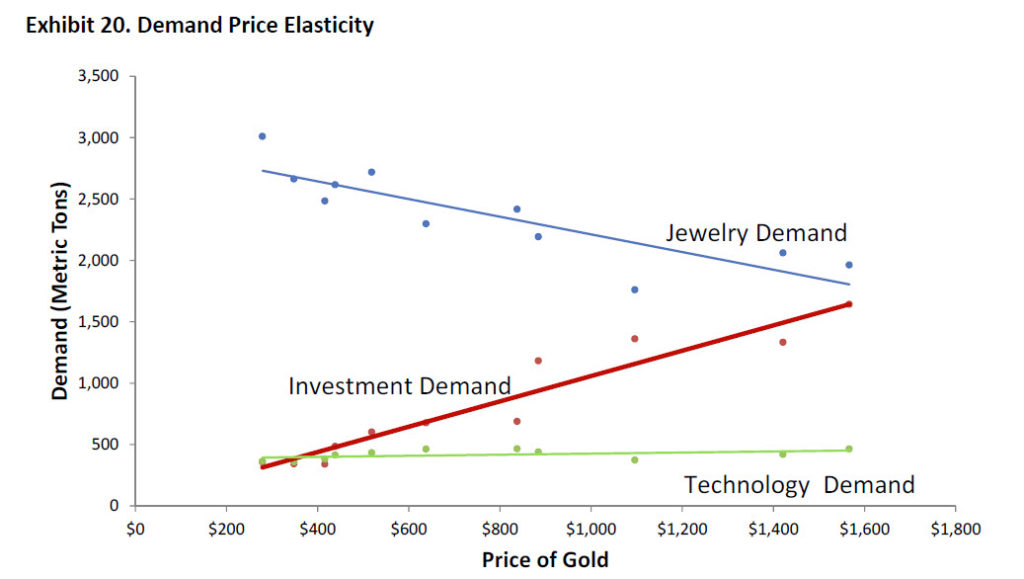

some facts about gold

In reading Campbell Harvey’s research on gold, I thought the following 3 charts were most interesting.

1. the real price of gold in the last 200 years

– the current period of price surge of gold has been extraordinary, even dwarfing the gold bubble in late 1970s. The #1 fact to bear in mind is gold price will eventually tumble in a very big way – it’s fool’s game that you think you can time the market.

2. how the gold price is related to real interest rate

– in my mind, I always think real interest rate plays a bigger role in determining the price of gold than any other factors, incl. inflation.

3. three elasticities of gold price: a. jewelry demand; b. investment demand; c. technology demand

– jewelry demand responds negatively to gold price: as price increases, fewer people can afford it in countries like India and China, where gold jewelry is popular.

– the waning jewelry demand is more than offset by increasing investment demand, especially in the age of ETFs.

– technology demand (or rather supply) responds to gold price very slowly due to the fact innovation in mining gold takes time, but eventually it will catch up.

Coase: China needs to have a free market for “ideas”

Ronald Coase, Nobel-winning economist, whose economic theory on property rights has had a profound impact on China’s economic reform in the past 30 years, prescribes medicine for China’s long-term sustained economic growth: to have a free market for ideas.

What Coase essentially argued was that China needed to have a free and open society. This would immediately mean the transformation of the current political regime.

Watch this ten-minute video:

Is manufacturing necessary for poor countries to become rich?

The traditional growth model for a poor country to become rich has always been a two-stage transition model. First, transition from agriculture to manufacturing, then from a manufacturing based economy to a modern economy largely based on services sector. Western European countries and the United States all went through the same growth process.

The intriguing question is, can a country prosper without going through the manufacturing phase? India so far seems to have defied the conventional wisdom, and its services sector led and powered India's fast growth for the last 15 years or so. But is India's growth sustainable? Can the service-led economy generate enough jobs for the poor peasants? And will India ultimately rely on manufacturing for its growth?

In one of the first efforts to untangle these questions, Economist Magazine recently has a very nice piece summarizing what we have known and not known so far:

INDIA’S services revolution has dazzled businesses in the rich world, turning Indian companies into global competitors and backwater cities such as Hyderabad into affluent, sophisticated technology centres. Yet economists have been less star-struck, clinging to the received wisdom that has prevailed since the industrial revolution: modernisation runs from agriculture through manufacturing and only later to services. Now some have broken ranks.

The logic supporting the conventional path towards an advanced economy is straightforward. Development typically involves moving workers from low-productivity activities such as subsistence farming to high-productivity sectors. That points to a shift into manufacturing because it lends itself to specialisation and economies of scale, both essential for rising output per worker. As first Japan, then Taiwan and South Korea, and now China have demonstrated, manufacturing can also accelerate development because its output can be exported to rich countries.

Services, in contrast, appear to be a graveyard for productivity. Because a haircut or a restaurant meal has to be delivered in person, there is almost no potential to exploit economies of scale and to export. People consume more services not when technological advance lowers their price but when they have reached a level of affluence that satisfies most of their other needs. Indeed William Baumol famously argued in the 1960s that as countries grew richer and their citizens became keener on buying services, their productivity growth would inevitably slow.

That conventional wisdom is now under fire, in a book edited by Ejaz Ghani of the World Bank and a related article he wrote with Homi Kharas of the Brookings Institution and Arti Grover also of the World Bank on the VoxEU website. The authors argue that technology and outsourcing are enabling services to overcome their former handicaps. Traditional services such as trade, hotels, restaurants and public administration remain largely bound by the old constraints. But modern services, such as software development, call centres and outsourced business processes (from insurance claims to transcribing medical records), use skilled workers, exploit economies of scale and can be exported. In other words, they are just like manufacturing. If that is the case, then poor countries should be able to go straight from agriculture to services, leapfrogging manufacturing.

…

Read the full text here. For the previous related post, look here and here.

Grantham on value investing and China

Jeremy Gratham of GMO talks about value investing: high growth does not mean high return to capital; it all depends on your entry point. He applies this classic investment philosophy to China. (source: Morngingstar Investment Conference, May 2009)

My wish for this year’s Nobel prize in economics

I know it’s a fool’s business trying to predict who is going to win the prize every year.

But here is my wish:

Oliver Hart and/or Ben Holmstrom

For his (or their) contribution to the theory of firm.

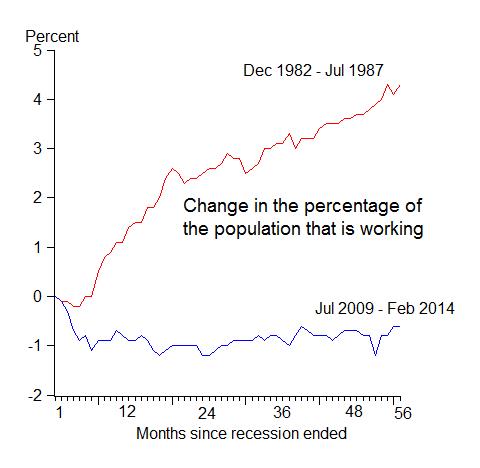

Why most Americans don’t feel the recession is over?

During the past five years, I have seen many similar charts. But this one really stands out as the best story-teller.

(source: vox.com)

Still the same

Official unemployment rate has gone down dramatically, but the improvement of labor market has been largely fake, as the employment-population ratio hasn’t moved much since recession ended. See this sharp chart from John Taylor at Stanford.

You can also take a longer term perspective at this ratio below:

Feel puzzled? You can find out the reason why unemployment rate and the employment-population ratio tend to diverge during this reovery here.

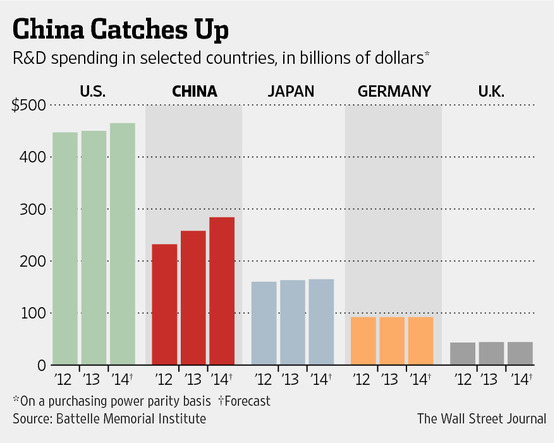

R&D and a hint of China’s future global brand

According to a study released in December by U.S.-based Battelle Memorial Institute, R&D spending in China will likely reach $284 billion this year, up 22% from 2012. That compares with just 4% growth forecast in the U.S. to $465 billion for the same period. It forecasts China will surpass Europe in terms of R&D spending by 2018 and exceed the U.S. by 2022.

According to WSJ, three Chinese companies are likely to emerge as China’s innovation leaders. They are Huawei, Lenovo and Tencent.

At Shenzhen-based Huawei Technologies Co., the world’s second-largest telecommunications-equipment supplier by revenue after Sweden’s Ericsson, annual R&D expenditures rose fourteenfold in a decade to $5.46 billion in 2013 from $389 million in 2003.

Personal-computer maker Lenovo Group Ltd., which last year overtook Hewlett-Packard Co. as the world’s largest PC maker by units sold, is setting a new precedent with its aggressive global expansion in smartphones.

Tencent Holdings Ltd., owns the WeChat smartphone application. Launched in late 2010, WeChat dominates China’s mobile messaging market and the majority of the app’s 272 million monthly active users are in China. But last year, it spent $200 million on overseas ad campaigns to push WeChat into many markets including India, South Africa, Spain and Italy. Tencent says the app has more than 100 million downloads abroad. WeChat was ahead of competitors in offering an easy-to-use feature for sending recorded voice messages and it is challenging the dominance of Silicon Valley’s WhatsApp, which has more than 300 million monthly active users globally.

Tencent’s share price nearly doubled last year and its market capitalization of $123 billion isn’t far from Facebook Inc.’s $139 billion market value.

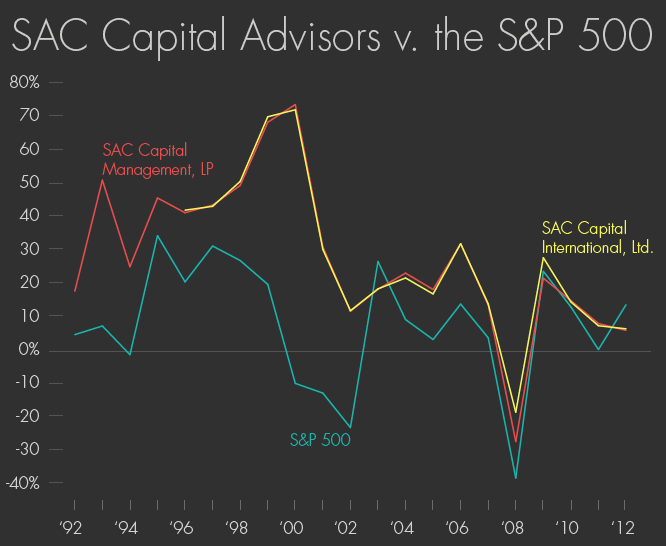

The fall of SAC

Frontline special: To Catch a Trader – The fall of king of hedge fund, SAC.

Fantastic journalism and story.