Home » 2010 (Page 7)

Yearly Archives: 2010

Unfilled job openings

This year's Nobel prize of economics was awarded yesterday to a trio of economists who have contributed to research in labor market frictions. Given the persistently high unemployment in the US, now at 9.6% and expected to go higher, the prize seemed to have a good timing. But despite their contributions, policy makers today still could not solve the problem. So is it just a mockery?

WSJ today has a good story (also good timing), on why there are so many unfilled job openings despite the high unemployment rate:

Among the explanations for the stubbornly high U.S. unemployment rate, factors such as housing troubles and extended unemployment benefits have played a leading role. Increasingly, though, economists and job seekers are identifying another problem: Employers are being pickier, or not trying as hard as they usually do to fill the openings they have.

![[OUTLOOK]](https://sg.wsj.net/public/resources/images/NA-BI402_OUTLOO_NS_20101010201703.gif)

The reasons for the foot-dragging are closely related to the reasons employers aren't creating many openings in the first place. Companies lack confidence about the outlook for consumer demand, they're not sure what the government will do with taxes and regulation, and they want to keep squeezing as much output from their current workers as they can. They also feel they have plenty of time to pick the best candidates.

the Fed compounds its mistakes

Allan Meltzer on the Fed's potential buying of more treasury bonds and inflation talk:

The Federal Reserve seems determined to make mistakes. First it started rumors that it would resume Treasury bond purchases, with the amount as high as $1 trillion. It seems all but certain this will happen once the midterm election passes.

Then the press reported rumors about plans to raise the inflation target to 4% or higher, from 2%. This is a major change from the Fed's quick rejection of a higher target when the International Monetary Fund suggested it a few months ago.

Anyone can make a mistake, but wise people don't repeat the same one. Increasing inflation to reduce unemployment initiated the Great Inflation of the 1960s and 1970s. Milton Friedman pointed out in 1968 why any gain in employment would be temporary: It would last only so long as people underestimated the rate of inflation. Friedman's analysis is now a standard teaching of economics. Surely Fed economists understand this.

Adding another trillion dollars to the bank reserves by buying bonds will not relax a constraint that is holding back spending. There is no shortage of liquidity in the economy—banks already hold more than $1 trillion of reserves in excess of their legal requirements, and business balance sheets show an unprecedented amount of cash and near-cash assets. True, increasing bank reserves means mortgage rates will decline, at least temporarily; they already have in anticipation of the bond purchases. But neither the Fed nor the public should expect much stimulus as a result.

The most important restriction on investment today is not tight monetary policy, but uncertainty about administration policy. Businesses cannot know what their taxes, health-care, energy and regulatory costs will be, so they cannot know what return to expect on any new investment. They wait, hoping for a better day and an end to antibusiness pronouncements from the White House. President Obama could do more for the economy by declaring a three-year moratorium on new taxes and new regulation.

Homebuilding is a major employment industry. Lowering mortgage rates helps a bit, but it is small beer when the supply of unsold houses remains large. The only lasting solution for housing is to let prices fall to a new equilibrium. Painful, yes, but necessary. Temporary palliatives such as lower interest rates delay that adjustment.

The market's response to the talk about renewed bond purchases includes a 12% or 13% decline in the value of the dollar against the euro. This depreciation occurred despite a weak euro, beset by potential crises in Ireland, Greece and Spain. The dollar's decline is a strong market vote of no confidence in the proposed policy.

Once the economy does begin to heat up, the Fed will urgently need to reduce excess bank reserves lest they stoke inflation. The Fed has talked about policies it can use to do so, such as raising the interest rates it pays to banks to hold their reserves. It has not offered a coherent, credible program to do so since it does not say, and probably does not know, how high the market interest rate would have to be.

But that is always the critical issue because the administration, Congress, business, unions and much of the public will demand a looser monetary policy if interest rates rise above 5%. Adverse public reaction to higher interest rates has stopped anti-inflation policy many times in the past.

Today bond markets act as if they believe the Fed can reduce current excess bank reserves fast enough to avoid inflation above 2% or 3%. They do not share my skepticism. Will they remain sanguine when excess reserves increase to $2 trillion? Or will interest rates rise, pushed up by a flight from government bonds? That's a risk that does not seem to bother many. Not yet, but it should, and it will.

One of the main reasons offered by some Fed governors and market portfolio managers for more stimulus is the fear of deflation. Yet the annual rate of increase in the consumer price index has remained between 1.2% and 2.5% every month this year. No evidence of deflation there. In fact, the Fed's inflation target is said to be between 1% and 2%, just about where it is.

The fear of mild deflation is another mistake, one commonly made. In the almost 100 years of Federal Reserve history, periods when prices declined over several months have occurred seven times. Sometimes the deflation reached 30%, yet the recoveries that followed six of the deflations cannot be distinguished from any other post-recession recovery.

The exception, the seventh, was the Great Depression. Prices had fallen but were expected to fall faster because, under the gold standard then in operation, people responded to failing banks and collapsing output by hoarding gold, further contracting the money supply.

Yes, a sustained deflation would be a big problem, but it is unlikely in today's circumstances. Countries with a depreciating exchange rate, an unsustainable budget deficit, and more than $1 trillion of excess monetary reserves are more likely to inflate. That's our problem today, and it's another reason the Fed should give up this nonsense about more stimulus and offer a credible long-term program to prevent the next inflation.

Mr. Meltzer is professor of political economy at Carnegie Mellon University, a visiting scholar at the American Enterprise Institute, and the author of "A History of the Federal Reserve" (University of Chicago Press, 2003 and 2010).

Why China wanted to peg US dollar?

Let’s put aside for now the debate on whether Chinese Yuan is undervalued or not, what are the motives for China to fix its currency to the US dollar around 1995?

First comes to my mind is the need to remove currency risk in trade. As we know, almost all trade contracts are denominated in dollar, not in Yuan. Currencies tend to move a lot, and nobody likes volatility. By pegging Yuan to the dollar, Chinese firms essentially save the cost from buying expensive currency risk hedging contracts.

Second, by fixing Yuan to the dollar, more or less, China submitted its monetary policy to the Fed, i.e., the Fed’s monetary policy tends to have a great impact on China’s own monetary policy. In other words, China’s central bank largely lost its autonomy. Good thing or bad?

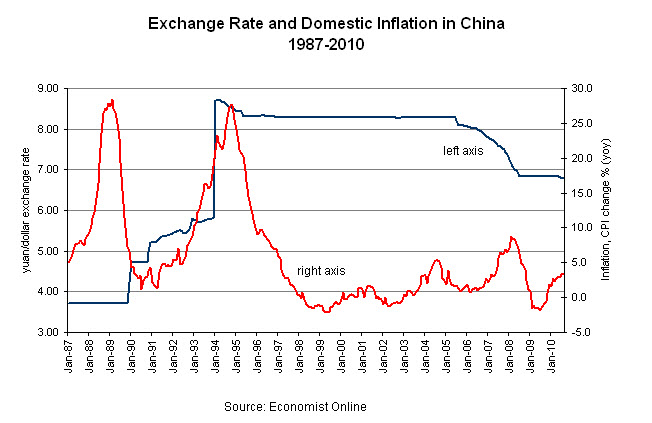

Below is a chart I just made looking at China’s domestic inflation, an important gauge for macro-stability, before and after the pegging to the US dollar.

(click on the graph to enlarge)

The chart is very dramatic. Before 1995, China’s inflation (in red) was very high and volatile. The Great Inflation in 1988 partly contributed to the 1989 students’ demonstration, which eventually led to the unfortunate Tian’anmen incident. After 1995, China’s inflation plummeted, and since then has remained quite stable – inflation never went up to over 10% again.

Was this because Chinese government suddenly improved their macro economy management skills? I don’t think so.

Here is what really happened – In essence, China achieved its macro-stability by outsourcing its monetary policy to the Fed, which has much more experiences in fighting inflation and also enjoys better credibility.

(update on Oct. 7, 2011)

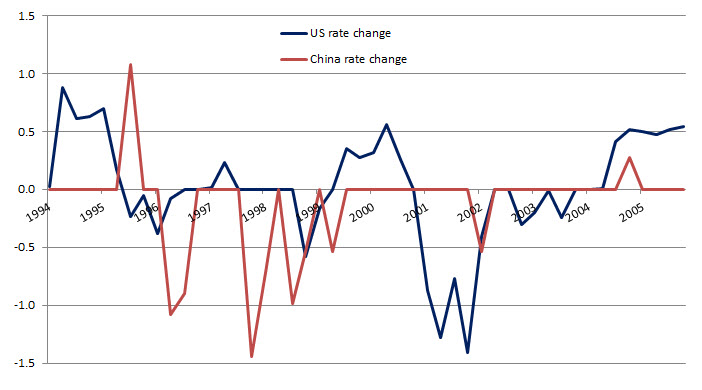

A re-look at the interest rate changes during 1995-2005 between China and the US, I changed my view that China’s inflation decline was due to its pegging to the US dollar. The more plausible explanation is China’s central bank successfully prevented inflation from rising by continuously raising interest rate, eventually pushing down inflation.

What’s holding back small businesses?

Here’s a chart from NYT breaking down what percent of small businesses cited each of these problems as their biggest challenge, going back to 1986:

Besides weak demand as shown up in poor sales, uncertainties in tax issues and government regulations are small business’ biggest concerns.

Time perspective of human behavior

Revealing the secrets of time – How people’s perspective of past, present and future shapes people’s behavior…and to some extent, a country’s development.

(hat tip to Carlos Yepez for providing the link)

China to offer support to Greece

Chinese Premier Wen Jiabao offered Greece a major vote of confidence on a visit to the debt-ridden European nation, saying China will continue to buy Greek bonds and announcing the creation of a $5 billion fund to help Greek shipping companies buy Chinese ships. The remarks represent some of China's most substantive support for the euro zone amid the region's debt troubles, and reflect the Asian giant's growing willingness to wield its economic clout to obtain wider international influence.

This is another attempt that China is trying to diversify away its investment in dollar-denominated assets. It's still too early to tell the impact of these government initiated investments. But history shows repeatedly when government gets into the business of firms, banks and individuals, it usually produces very poor results. What China should do is to reform its currency policy and speed up its financial reform; What it should not do is to continue building up foreign exchange reserves, and firms and businesses should be allowed to have their own foreign currency account and manage the currency risk by themselves.

Currency appreciation will not cure trade deficit

US House passed a currency bill by a wide margin, 348-79, yesterday to penalize China’s foreign-exchange practices. The measure would allow, but not require, the U.S. to levy tariffs on countries that undervalue their currencies, which makes their goods cheaper relative to American products.

This is a highly politically-charged bill, right before the US’ mid-term election. With high unemployment rate of nearly 10% at home, blaming foreigners for one’s own backyard problem has always been the easiest solution for politicians in the past.

As I have done many analysis before, currency is not the the solution to America’s trade deficit problem, Japan’s experience back in 1980s is the best example. Neither it’s the solution for the unemployment problem. The high unemployment rate was created by the most severe recession since WWII, and by the huge bubble in housing market.

Simple economics will tell when China’s exports become more expensive, US importers will, sooner or later, choose to import from other developing countries, whose exports will become cheaper and more competitive than China. This is the so-called substitution effect. In the end, China’s trade surplus will shrink with the US, but US’ overall trade deficit will not budge. To solve the trade deficit problem, US consumers really need to save more, or consume less. The savings rate has already been rapidly increasing in the past couple of years. Sounds painful, but this is a process the US economy has to go through. Yesterday’s spendthrift means today’s frugality.

And by the way, who will get hurt most by the import tariff? The US consumers.

What about China? China should stop subsidizing exports through lower currency or tax rebate. Subsidizing exports is essentially shifting Chinese tax payer’s money and put it into American consumers’ pockets. Good deal for America; bad deal for China. The export subsidy will also distort resources allocation according to price signals, resulting in too much capital invested in the low-end export industry, with poor capital return.

Here is the latest video analysis from WSJ (quite heated):

update1: 10 am 09/30

I said above Yuan’s appreciation will shrink US trade deficit with China, but US total trade balance with the world won’t change much because of substitution effect. Now looking at the the following two charts I’ve just made, I even doubt that Yuan’s appreciation will shrink US-China trade deficit.

The first chart shows the cumulative trade deficit of US with China (in red), and Yuan-Dollar exchange rate (in black) from 2000 to 2009. Yuan had depreciated by almost 17% from 2004 to 2007, but the US trade deficits with China just kept soaring. Yuan’s appreciation did not solve the problem.

The second graph shows a similar story. The difference with the first chart is now I show the monthly trade deficits (not cumulative, in red). The blue line shows the 12-month moving average of the monthly number. The trend was clearly upward despite Yuan’s 17% appreciation during 2004-2007. Again, currency appreciation did not solve the US trade deficit problem, and it just kept growing, only until the recent recession hit, it started to trend downward.

My educated guess is that, because Chinese price is so low, even with currency appreciation and higher goods prices than before, the demand for such goods did not decrease much. In other words, American consumers may have a quite inelastic demand curve for Chinese goods. After all, majority of Chinese exports are necessity goods, not the durables, nor the luxuries.

Gary Becker on China’s Long Term Prospect

Gary Becker just came back from China. And he shares his thoughts on the country's long-term growth prospect. Like many others, Becker sounds a little worried about the enlarging state-sector in Chinese economy.

China's Next Leap Forward

by Gary Becker

Mr. Becker, the 1992 Nobel economics laureate, is professor of economics at the University of Chicago and senior fellow at the Hoover Institution.

I just spent two weeks lecturing in China and Hong Kong, and discussing China's economic development with many economists, businessmen and government officials. China's progress since my first trip there in 1981 has been truly remarkable, and I expect considerable growth during the next decade. Nevertheless, China still faces many challenges if it is to move beyond middle-level income status into the exclusive club of high per capita income countries.

No country in the modern world has managed persistent economic growth without considerable reliance on private enterprise and decentralized private markets. All centrally planned economies failed to achieve sustained development, including the Soviet Union before its collapse, China before market reforms began in the late 1970s, and Cuba since Castro's revolution in the late 1950s.

China's private sector has led its dominance in textiles, electronics, and other consumer and producer goods. It's followed the model of the "Asian Tigers"—Hong Kong, Singapore, South Korea and Taiwan—and relied heavily on exports produced with cheap labor. In the process, China has accumulated enormous reserves, as Taiwan, Japan and other rapidly growing Asian economies did in past decades.

Poorer countries like China need not get everything "right" to grow rapidly through exports to richer countries. They need only have some strong sectors that use world markets to fuel overall growth. Japan's rapid growth from the 1960s-1980s was led by a highly efficient manufacturing sector. Yet at the same time Japan also had a large and inefficient service sector, and an agricultural sector that was riddled with subsidies and inefficient incentives.

Similarly, China's economy still has a glut of state-owned enterprises (SOEs) with excessive employment and low productivity. Their importance has fallen over time, but Chinese economists estimate that they still control about half of non-agricultural GDP (*SOE's share in manufacturing sector is much lower – my own note). One crucial example is the state-controlled financial sector that makes cheap loans to other large, inefficient and unprofitable state enterprises. China's economy also suffers from extensive price controls, restrictions on migration, and many other structural barriers to efficient growth.

Some democracies, like postwar Japan, have made the economic reforms needed for sustained economic progress. India, for example, experienced rapid growth after it began in 1991 to shed a socialist orientation and encourage private investment and private initiative. But economic progress has been swift under autocratic rule as well, including in Chile under Augusto Pinochet, Singapore under Lee Kuan Yew, and Taiwan under Chang Kai-shek. Usually, however, personal freedom has grown along with rapid economic progress in autocratic governments. Chile, Taiwan and South Korea, for example, all became vibrant democracies after they'd grown rapidly for a number of years.

Something related has happened in China. The degree of personal freedom in China today is enormously greater than in 1981, when the vast majority of the population had essentially no personal freedoms. The Internet, in particular, has given hundreds of millions of Chinese access to all kinds of information, including what happens in democracies, and various criticisms of their government's policies. The government actively tries to censor the Internet, but these censors are easily bypassed. Students and others say they readily "climb the wall" by using cheap software (appropriately, made in America) that gives them direct access to the Internet in Hong Kong and hence avoids the censors.

I do not know how soon China will evolve into a political system with competing parties, or whether China will continue to have effective leadership under its single-party structure. But as the economy continues to develop it will be impossible to prevent personal freedoms from expanding, including the freedom to criticize economic and social policies.

Global markets allow poor countries to grow rapidly for a while, but it is far more difficult to grow beyond middle-income levels. Much has been made of the fact that a month ago China's aggregate GDP surpassed that of Japan. But all that means is China's per capita income is about 10% of Japan's, since China's population is about 10 times that of Japan. Despite its great economic advances, China still has a long way to go to become a rich country.

China's locally owned government enterprises have been more efficient than national enterprises. This is mainly because local government enterprises have to compete against each other, whereas national enterprises often receive monopoly positions. But competition among government enterprises is a partial substitute for competition among privately owned enterprises. If China wants to continue to grow rapidly it will have to reduce the scope of the SOEs, especially the national ones, and greatly expand the private sector in finance, telecommunications and many other fields.

Developing countries improve their technological base by importing technologies and knowledge developed in advanced countries. China has encouraged direct foreign investment in part to get access to the technologies of Japan, the U.S., Germany and other nations. Using technologies developed by others is still important after countries advance to middle-income levels, but these countries must then also develop more of their own technologies to advance much further.

To accomplish this transition, China has been promoting university enrollments and a growing R&D sector. University attendance in China has grown greatly since the late 1990s, propelled by rapid increases in the earnings of individuals with higher education. China is innovating more, but it is still a long way behind the U.S., Japan and other rich countries.

As for China's currency, it's true that the yuan is considerably undervalued due to Beijing's continued intervention in foreign-exchange markets. But the undervalued yuan is a gift to American and other consumers outside China because it makes goods produced in China much cheaper.

In effect, China sells goods cheaply to the rest of the world and receives in return U.S. and other paper assets that pay almost no interest, and will depreciate in value when inflation rates increase in the U.S. These are the main reasons why China should move toward floating the yuan.

Many Chinese officials believe that substantial yuan appreciation will make the SOEs even less competitive, thereby increasing unemployment and social unrest as these enterprises contract. Yet an undervalued currency not only leads to a further accumulation of paper assets but also weakens the incentives of Chinese companies to cater to domestic consumption—which is remarkably weak—and to upgrade their exports to higher quality products.

There is tremendous pride and enthusiasm among Chinese regarding their economic achievements, and a growing confidence that China is returning to its great-country status of centuries ago. This is reflected in the enormous energy of its professionals, entrepreneurs and workers...