Home » China (Page 5)

Category Archives: China

The Fed is set to surpass China…

The Fed is set to replace China as the largest holder of the US treasuries.

(source: Bloomberg)

Chinese government does not have much choice here. It can’t ditch dollar – that’s the only international reserve currency today, probably the safest one in time of crisis; It can’t buy gold, not much. Otherwise, it will push up gold price dramatically. It can’t buy high-growth currencies, like Aussie dollar or Brazilian real, either: the appreciation of these currencies will make China’s imports of natural resources more expensive.

Chinese central bank is left with roughly three choices:

1) buy assets denominated in Euro and Yen – Germans and Japanese then won’t be happy because now every country seems to have adopted a “beggar-thy -neighbor” policy, trying to increase exports through currency devaluation.

2) buy hard assets, such as oil, gas and mines – that’s what China had been doing. But this is likely to stir a lot of nationalism – Nobody likes such government-led big purchase of its own natural resources, especially this government is led by a Communist Party.

3) equity investment in or partnership with good-solid companies. Companies like Warren Buffet’s Berkshire Hathaway, Goldman Sachs, JP Morgan, Coca-cola, HP, etc…these solid blue chip companies with diversified international portfolio.

In the long term, China should work on designing an alternative international monetary system – a system not based on any paper currency of a single country.

Why China wanted to peg US dollar?

Let’s put aside for now the debate on whether Chinese Yuan is undervalued or not, what are the motives for China to fix its currency to the US dollar around 1995?

First comes to my mind is the need to remove currency risk in trade. As we know, almost all trade contracts are denominated in dollar, not in Yuan. Currencies tend to move a lot, and nobody likes volatility. By pegging Yuan to the dollar, Chinese firms essentially save the cost from buying expensive currency risk hedging contracts.

Second, by fixing Yuan to the dollar, more or less, China submitted its monetary policy to the Fed, i.e., the Fed’s monetary policy tends to have a great impact on China’s own monetary policy. In other words, China’s central bank largely lost its autonomy. Good thing or bad?

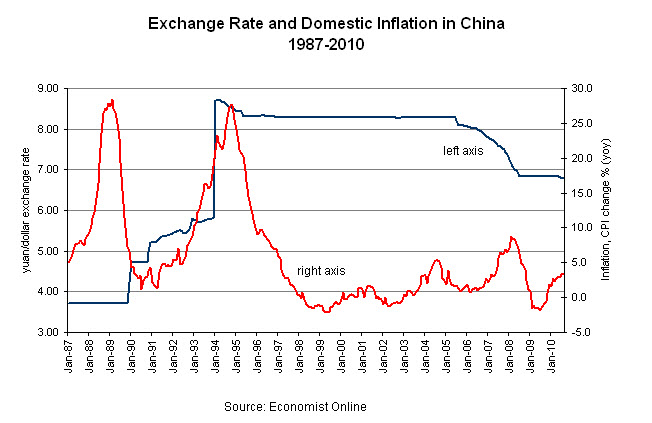

Below is a chart I just made looking at China’s domestic inflation, an important gauge for macro-stability, before and after the pegging to the US dollar.

(click on the graph to enlarge)

The chart is very dramatic. Before 1995, China’s inflation (in red) was very high and volatile. The Great Inflation in 1988 partly contributed to the 1989 students’ demonstration, which eventually led to the unfortunate Tian’anmen incident. After 1995, China’s inflation plummeted, and since then has remained quite stable – inflation never went up to over 10% again.

Was this because Chinese government suddenly improved their macro economy management skills? I don’t think so.

Here is what really happened – In essence, China achieved its macro-stability by outsourcing its monetary policy to the Fed, which has much more experiences in fighting inflation and also enjoys better credibility.

(update on Oct. 7, 2011)

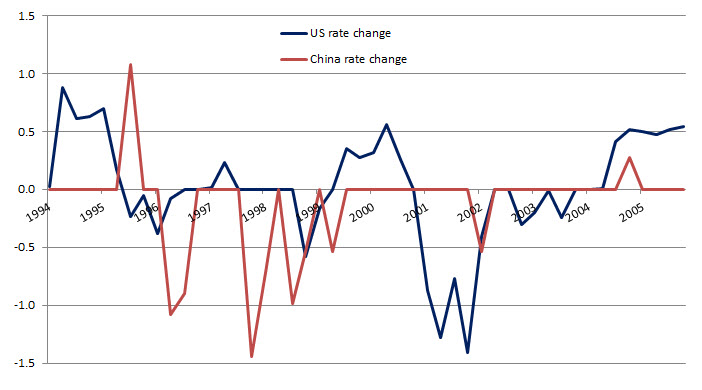

A re-look at the interest rate changes during 1995-2005 between China and the US, I changed my view that China’s inflation decline was due to its pegging to the US dollar. The more plausible explanation is China’s central bank successfully prevented inflation from rising by continuously raising interest rate, eventually pushing down inflation.

China says “Trade your technology for our market”

China’s government is considering plans that could force foreign auto makers to hand over cutting-edge electric-vehicle technology to Chinese companies in exchange for access to the nation’s huge market…

China’s Ministry of Industry and Information Technology is preparing a 10-year plan aimed at turning China into “the world’s leader” in developing and producing battery-powered cars and hybrids, according to executives at four foreign car companies who are familiar with the ministry’s proposal.

The draft suggests that the government could compel foreign auto makers that want to produce electric vehicles in China to share critical technologies by requiring the companies to enter joint ventures in which they are limited to a minority stake.

The government figured out China’s market is too great for foreign auto makers to say “No”. It’s a trade off both parties understood: either losing some technology secrets to Chinese or completely being shut out of the market.

This is a strategic game. And Chinese look smart. The hope is that both parties still see there are mutual gains to be made.

But Chinese policy makers risk going too far. Asking foreign auto makers to give away too much of their tech secrets will generate perverse incentives: foreign auto makers may respond to this policy by only using the less advanced technology in China’s car manufacturing. “Yes, we are going to share with you technology, but only the old dated ones”.

China’s domestic consumers may also suffer – cars equipped with the best technology may become unavailable to domestic car buyers, or only available through imports, but at a much higher price.

Demographics and Wealth of Nations

Following my previous post, “India needs manufacturing“, in which future population growth trend was analyzed, today I post another analysis from WSJ’s David Wessel on the relationship between demographics and nation’s wealth. Before that, I would like to give some background.

China’s huge population was long thought to be a development burden for the country. High population density puts all kinds of resources under pressure – water, energy, environment, traffic, etc. And if you take a static view, more population simply leads to lower living standards (if you measure living standards simply by GDP per capita). Simple math shows despite the fact that China is the second largest economy in the world (with total GDP 1/3 of the US), China’s GDP per capita is only 1/10 of the United States, as its population is 3 1/2 times larger.

China’s population surge during the second half of the 20th century was largely man-made. After 1949, when China’s Communist Party established People’s Republic, there was a big fear that the US may invade mainland China, along with the defeated Nationalist Party. During the era of conventional warfare, the size of army mattered. Chairman Mao, China’s paramount first-generation leader, encouraged every Chinese family to have more children – three, four, or even more. Such policy rendered probably the sharpest population growth in China’s modern history.

China’s policymakers soon realized they made a huge mistake. The immediate concern was how to feed the rising population when China was still in total blockage under Western Sanction (like today’s North Korea). The deliberation at the highest level then manufactured China’s unique “One Child Policy” (OCP), now worldly famous – which went into effect since mid 1970s, and got really tough since early 1980s. In urban China, OCP is strictly enforced; in rural China, it is more relaxed, especially when the first baby happens to be a girl.

Now after more than 30 years, Chinese policymakers had another problem – The rapidly shrinking young labor force. Over the past 30 years, China’s huge labor reserve (or cheap labor) has contributed a great deal to her fast economic growth. Ironically, once the growth engine started, population turned out to be a growth dividend, not a burden. China’s huge population also attracted tremendous foreign investments – who would not want a bite in the largest domestic market in the world?

But the ‘young’ developing China is forecast to face ageing problem much sooner than most countries at its development stage. To replenish population, the fertility rate should stay at least 2. Any rate below 2 means declining population (this assumes birth rate and death rate are roughly the same, but if people live longer, this will generate a larger share of older population). For thirty years, China’s fertility rate has only been slightly above 1. OCP effectively controlled China’s population growth, but also put China onto a “fast lane” toward ageing society.

Let’s get to details: One-Child Policy started roughly around 1980, so the first cohort of young population (about 20 years old) entered labor force around year 2000, that’s when China suffered its first dent on labor force. It’s no coincidence that during the same time various reports surfaced that manufacturing firms in China’s east coast started to feel labor shortage, defying the popular image that China seemed to have unlimited labor supply. The shrinking labor supply will become more severe when the last large cohort of population born right before OCP exits the manufacturing. I assume this is going to happen from now to the next five years (2010-2015), when most of these workers reach their middle-age (35 to 40). With more working experiences and skills, especially, the migrant workers in this group will seek more stable income and better location with equal social benefits. This often means exits from coastal manufacturing.

China’s young labor force will continue to shrink until 20 years after the major policy reversal. The policy reversal now in effect is to allow qualified couples to have up to two children, if both husband and wife are the only child in their own families. Let’s assume these couples will have their children between 25 and 35 years old (or between year 2005 to 2015 for the first cohort). Only when their children grow old enough to join labor force, i.e, when they become abut 20 years old (or between 2025 and 2035), will China’s young labor force start to grow again. This simply means within roughly a 30-year range, from 2000 to 2030, China’s young labor force will continuously trend downward. For a country still at its early development stage, this forecast should sound high alert to policy makers.

If you want to know about the role of population in country’s growth and development, feel free to download my lecture notes on the population theory. Economist Magazine also has a terrific article, “Does Population Matter?”

Now without further adieu, I introduce you to David Wessel’s analysis on the “Demographics and Nation’s Wealth“. Pay special attention to the US’ future demographic trend, and what can we learn from it.

Demography is not destiny. In 1300, China was bigger than Europe and had the world’s most sophisticated technology. But China blew it. By 1850, its population was 65% larger than Europe’s, but—thanks to the Industrial Revolution—Europeans were far richer.

Yet demography does matter. “We never pay enough attention to demography because it’s so long term,” says Dominique Strauss-Kahn, head of the International Monetary Fund. So turn for a moment from angst about the disappointing pace of the economic recovery and daunting government budget deficits, and look over the horizon.

Over the next 40 years, Japan and Europe will see working-age populations shrink by 30 million and 37 million, respectively, according to United Nations projections. Birth rates are low and so many of their people are already elderly.

![[Capital]](https://sg.wsj.net/public/resources/images/NA-BH438_Capita_NS_20100811192813.gif)

China’s working-age population will keep growing for 15 years or so, then turn down, the result of its one-child policy and the tendency of birth rates to fall as incomes rise. In 2050, the U.N. projects, China will have 100 million fewer workers than it does today. India’s population, in contrast, will grow by 300 million working-age persons over the next 40 years.

The U.S. is in between, benefiting from a higher birth rate and younger populations than Europe and Japan and more immigration. It is projected to add 35 million working-age persons by 2050.

So what?

History, as interpreted by modern economists pondering the mysteries of growth, teaches that more people lead to more ideas. And unlike land or oil, ideas can be used by more than one person simultaneously. Before countries began sharing ideas, the biggest had the most rapid technological progress. Now, trade, travel and the Internet speed new ideas around the globe ever-more rapidly. So the benefits are dispersed. Belgium is rich not because it is big or has invented a lot, but because it has the wherewithal to employ technology invented by others, notes Michael Kremer of Harvard University. Zaire is bigger, but lacks the wherewithal.

…

“China’s population is roughly equal to that of the U.S., Europe and Japan combined,” optimistic Stanford University economists Chad Jones and Paul Romer observed recently in an academic journal. “Over the next several decades, the continued economic development of China might plausibly double the number of researchers throughout the world pushing forward the technological frontier. What effect will this have on incomes in countries that share ideas with China in the long run?” Somewhere between a lot and really a lot, they say. In fact, they say that even if the U.S. had to bear all the costs of mitigating the added carbon emitted by a rapidly developing China, ideas generated by the Chinese would boost U.S. per capita income enough to more than compensate.

…

For China, the challenge is to build social structures and retirement schemes to sustain a growing cadre of old folks that, unlike previous generations, won’t be able to rely so much on its children for support. Today, 1.4% of Chinese are over age 80; in 2050, 7.2% will be, the U.N. projects.

…

And the U.S.? For all today’s gloom, it may be in the sweet spot. A growing population, an openness to ambitious immigrants and trade (if not disrupted by xenophobic politics) and strong productivity growth (if sustained) could lift living standards and bring faster growth, which would reduce big government budget deficits far easier for the U.S. than for slower growing Europe and Japan.

Hong Kong – China’s currency lab

When to liberalize Chinese currency, Yuan or RMB? How to make Yuan more internationally influential? Hong Kong is being used by Chinese government as their forefront currency experiment lab. Reports WSJ:

![[HKVIEW]](https://sg.wsj.net/public/resources/images/MI-BE974_HKVIEW_NS_20100801171253.gif)

A burst of activity is under way here in the city that might be called China’s in-house research-and-development center for currency liberalization.

It’s on a tiny scale by normal standards of the $3 trillion-a-day market for foreign exchange. But in Hong Kong, banks are for the first time starting to lend yuan to one another outside mainland China and offering hedging services that weren’t available before. The result, say bankers, is reminiscent of the eurodollar market in the early 1960s, when extensive dealings in the greenback outside U.S. borders first took off.

The catalyst for this activity was an agreement signed June 19 between monetary authorities in mainland China and Hong Kong removing certain limits on usage of China’s yuan within Hong Kong. In the past, businesses were mostly confined to opening yuan accounts for trade-settlement purposes; now, accounts can be opened for any purpose. Businesses and individuals alike now can transfer yuan freely between accounts. Banks also can help businesses convert yuan without restriction.

…

With the latest liberalization move, banks in Hong Kong are now freer than ever to take all that yuan and put it to work. Some speak of linking the interest rate paid on yuan deposits to the direction of the euro or gold prices. Frances Cheung, senior strategist at Crédit Agricole Corporate & Investment Bank, foresees a market for yuan interest-rate swaps as interbank lending in the currency gains momentum.

…

Meanwhile, more and more yuan pour into Hong Kong. Monthly trade between Hong Kong and mainland China settled in yuan jumped tenfold from January to June to 13.24 billion yuan, or nearly $2 billion, and it’s set to rise more quickly since a pilot program allowing yuan settlement expanded to cover more of China in June.

Qu Hongbin, chief China economist at HSBC in Hong Kong, believes we are seeing just the tip of the iceberg. The anomaly, he says, is the fact that China conducts virtually all its trade in dollars, euros or yen. Historically, he says, “we’ve never seen a case where the world’s largest exporter uses other people’s currency for their trading.”

Will China surpass the US?

An interesting question ask, and a nice debate to watch.

My 2 seconds on this: China’s TOTAL GDP, now about 1/3 of the US, will catch up with the US in around 2020-2025 – for this I have no doubt. China is not another Soviet Union – China’s political party is still called Communist Party, but if you ever travel to China, and talk to the average people there, you will immediately know China is the most capitalist country in the world – travel makes you smarter 🙂

The much more difficult task is to lift the living standards of average Chinese citizen to the US level – China’s GDP per capita is only 1/10 of the US – and build up stronger and better institutions, especially political and legal ones, to sustain the long-term growth. For this, China has a lot to learn from the US.

How to watch China bubble

Ed. Chancellor of GMO (in Boston) has put out an excellent piece on the Chinese market and the “red flags” for investors.

The paper addresses how to identify the proper “speculative manias” and associated financial crises in the country. Chancellor sums it into key points, breaking down the bare essentials:

1. Great investment debacles generally start out with a compelling growth story.

2. A blind faith in the competence of the authorities is another typical feature of a classic mania. In other words, you can’t always trust the numbers that a government is putting out.

3. A general increase in investment is another leading indicator of financial distress. Capital is generally misspent during periods of euphoria.

4. Great booms are invariably accompanied by a surge in corruption. Countrywide, anyone?

5. Strong growth in the money supply is another robust leading indicator of financial fragility. Easy money lies behind all great episodes of speculation from the Tulip Mania of the 1630s – which was funded with IOUs – onward.

6. Fixed currency regimes often produce inappropriately low interest rates, which are liable to feed booms and end in busts.

7. Crises generally follow a period of rampant credit growth. In the boom, liabilities are contracted that cannot subsequently be repaid. The U.S. will ultimately be a perfect example of this.

8. Moral hazard is another common feature of great speculative manias. Greed isn’t necessarily good and we tend to act irresponsible during intense periods of speculation.

9. A rising stock of debt is not the only cause for concern. Investments financed with borrowed money don’t generate enough income to either service or repay the loan (what Minsky called “Ponzi finance”).

10. Dodgy loans are generally secured against collateral, most commonly real estate. Thus, a combination of strong credit growth and rapidly rising property prices are a reliable leading indicator of very painful busts.

Bergsten’s China action plan

Here is the action plan from C. Fred. Bergsten, Director of Peterson Institute of International Economics:

(Congressional Testimony) Hence I would recommend that the Administration adopt a new three-part strategy to promote early and substantial appreciation of the exchange rate of the renminbi

- Label China as a “currency manipulator” in its next foreign exchange report to the Congress on April 15 and, as required by law, then enter into negotiations with China to resolve the currency problem.

- Hopefully with the support of the European countries, and as many emerging market and developing economies as possible, seek a decision by the IMF (by a 51 percent majority of the weighted votes of member countries) to launch a “special” or “ad hoc” consultation to pursue Chinese agreement to remedy the situation promptly. If the consultation fails to produce results, the United States should ask the Executive Board to decide (by a 70 percent majority of the weighted votes) to publish a report criticizing China’s exchange rate policy.

- Hopefully with a similarly broad coalition, the United States should exercise its right to ask the WTO to constitute a dispute settlement panel to determine whether China has violated its obligations under Article XV (“frustration of the intent of the agreement by exchange action”) of the WTO charter and to recommend remedial action that other member countries could take in response. The WTO under its rules would ask the IMF whether the renminbi is undervalued, another reason why it is essential to engage the IMF centrally in the new initiative from the outse