Home » Currency (Page 2)

Category Archives: Currency

Stephen Roach: Take out Krugman’s baseball bat

Krugman portrayed the problem of global imbalances as solely coming out of China’s high saving rate and manipulation of its currency. Stephen Roach, Chairman of Morgan Stanley Asia, offers a more comprehensive perspective.

Americans have been saving nothing, consuming too much, and high on leverage. “Get your own house in order” before you carry stick toward others — that’s the sensible advice from Roach.

Market and the Dollar

This is a remarkable graph showing the negative correlation between the market and US dollar.

Warren Buffet: Squanderville vs. Thriftville

Borrow to spend like the debts won’t be repaid forever. That’s how we got here. That’s how the US, the world superpower, jeopardizes its own currency and subjects its national security to foreign trading partners.

Also read Paul Samuelson’s warning on the US dollar

and Julian Robertson on “How we put ourselves into this terrible position“.

![Reblog this post [with Zemanta]](https://img.zemanta.com/reblog_e.png?x-id=96287378-429e-47f9-8a70-db2b8d4860b6)

Gaming ‘Hot Money’

I think China’s recent policy to remove the almost certainty of its currency appreciation was really a smart move. Chinese policy makers may have simply based their policy move on the concern over the grim export outlook, but the unintended consequence or byproduct of this policy is that it will actively discourage the flow of ‘hot money’ into the country.

Here below I borrow the framework of game theory to illustrate the gaming of the ‘hot money’. Hot money here refers to the short-term international capital investment, and it’s different from long-term international investment such as FDI.

The graph illustrates how a sequential game works. Chinese government chooses their first move based on their policy objectives, i.e. to discourage hot money inflow; then foreign investors respond with their best move. In this game, we implicitly assume hot money inflow is bad.

The numbers in the parenthesis show the payoff structure of the game. Chinese government first decides whether to make the prospect of currency appreciation certain, and foreign investors then choose to invest or not.

The equilibrium of the game is at the left upper corner, where Chinese government makes the appreciation uncertain and foreign investors choose not to invest as the payoff is greater for not investing (0>-1).

In hindsight, Chinese policy makers should have made the move earlier. But it’s O.K.

Now read the related article on WSJ that touches the same issue:

China’s policy makers have done a great job of creating confusion in foreign exchange markets. That might’ve been their intention all along.

Beijing has much to gain by inserting doubt into the minds of the “yuan will always rise” crowd; namely, putting an end to so-called hot money inflows that are predicated on this assumption.

![[Yuan deposits held in Hong Kong bank accounts]](https://s.wsj.net/public/resources/images/OB-CU039_YUANST_NS_20081208045802.gif)

These potentially volatile capital flows can cause inflation on the way in. Their sudden exodus, meanwhile, leaves a significant financial hole in bank balance sheets or asset prices — something China’s neighbors learned all too well during the 1997 Asian financial crisis.

Analysts think more than $150 billion of these funds made their way into China in the first half of 2008 alone, and Beijing’s made no secret of its efforts to put an end to the trend.

This is where the recent debate over the yuan’s direction could help. It started last week with a not-too-subtle move by Chinese policy makers to set the daily dollar-yuan “fixing” 0.2% higher than the day before. That was taken by some as a hint of bigger things to come, sparking trading in derivatives that profit only if the yuan is devalued in the year ahead.

The yuan itself, which trades within a band around that that daily fixing, also fell quickly. Against the dollar, the currency is down around 0.7% in the last week.

This will be unsettling for those who’ve seen the yuan’s inexorable rise as a sure-thing. Residents of Hong Kong, for example, have been converting massive amounts of their savings into yuan deposits. Over the last three years, these yuan deposits in Hong Kong banks have tripled in value to about $10 billion.

Those Hong Kongers may think twice now. They and the rest of the hot money crowd have been warned that they shouldn’t make any assumptions about Beijing’s intentions, even if a large-scale devaluation remains unlikely.

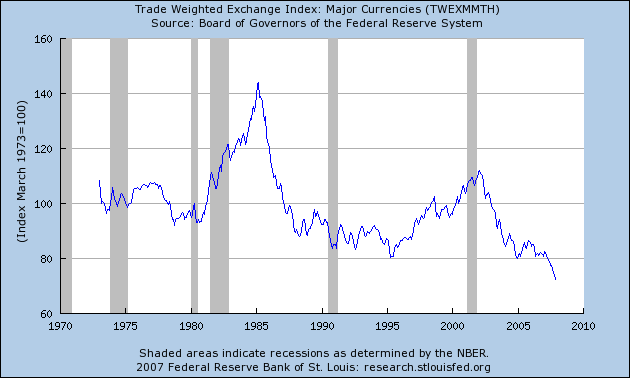

Put dollar depreciation in historical perspective

{kind=link}