Home » Economy (Page 13)

Category Archives: Economy

John Paulson netted $5 billion in 2010

According to today's Journal,

Hedge-fund manager John Paulson personally netted more than $5 billion in profits in 2010—likely the largest one-year haul in investing history, trumping the nearly $4 billion he made with his "short" bets against subprime mortgages in 2007.

…

By comparison, Goldman Sachs Group Inc., Wall Street's most profitable investment bank, paid all of its 36,000 employees a total of $8.35 billion last year. James Gorman, chief executive of 76-year-old investment bank Morgan Stanley, is expected to receive compensation of less than $15 million for 2010.

…

Mr. Paulson amped up profits for himself and many of his investors in a novel way. He was worried about long-term weakness of the dollar and other major currencies, so he devised a way to embed a bet on gold into each of his funds—for those investors who opted for that approach. Mr. Paulson has placed the bulk of his own wealth in these gold-denominated funds and a separate gold-focused fund. Because gold rose sharply in value last year, the gold-denominated versions of his funds rose as much as 45%.

The performance last year, nevertheless, paled in comparison to his 2007 returns, when Mr. Paulson made a huge wager against subprime mortgages and his funds scored gains of as much as 590%.

read more here.

China is on buying spree

With $ 2.85 trillion foreign exchange reserves and counting, China has been on a buying spree in the past few years. From 2007 to first half 2010, China has acquired over 400 firms overseas, or $86 billion, according to Rand Corp.’s Wolf.

China has the urgent need to diversify its investment of its foreign assets since the US dollar is on steady decline. One way of spending the huge foreign reserves is through purchase of natural resources and advanced capital equipment, the latter of which will benefit China via technology spillover, boost China’s labor productivity growth.

For sure, this state-led investment will be inferior to individual-firm’s investment decisions, inevitably bringing some bad returns. China will need eventually relax its control on capital account and bring its surplus of balance of payment account to a more reasonable level.

Obama’s central planning rhetoric

In yesterday's State of Union address, President Obama said this:

We need to out-innovate, out-educate, and out-build the rest of the world…By 2035, 80% of America's electricity should come from clean energy sources. Within 25 years, 80% of Americans should have access to high-speed rail. Within five years, communications businesses should be able to deploy high-speed wireless to 98% of all Americans.

I am deeply troubled by his speech. Competition is good among countries, just like competition among firms. I am generally for competition. But it seems that Obama does not have the current US budget situation in mind – he said the nation needs to address its rising budget deficit but couldn't afford to back away from new spending on programs that he said would allow the U.S. to compete with rising powers like China and India.

Further, his lofty goals just reminded me of central planning in socialist economies. Since when the pace of innovation can be dictated by government spending? Did Google, Facebook, Apple's iPad/iPhone come out of government plan?

And there is a reason for relative backwardness of American rail travel – because the auto travel is the most convenient and most advanced in the world – compare the traffic jams in Chinese cities. China needs to have its high-speed railway, because Chinese population is four times larger than the US and heavy pollution is everywhere – this is probably China’s best option. You can't just develop high-speed railway simply because China is doing it. Have some sense of economics, please.

And finally, Mr. President – China is not another Soviet Union.

China’s banks – a drag on rebalancing

China's banks are a drag on China's economic restructuring:

1) More than ten years of joining WTO, China's banking sector is still largely closed off to foreign competition;

2) Most banks are state-owned, in favor of allocating capital to export sector and state-owned enterprises (or SOEs), whose bad loans are implicitly guaranteed by the government (reminiscent of Fannie and Freddie in the US). Small-and-medium businesses find access to bank loans very difficult;

3) Interest rates are still set by Chinese government, not determined by the market. The fixed loan-to-deposit margin provides no incentives for banks to improve their risk analysis skills.

With these problems, Joseph Sternberg argues, "Don't bank on China's rebalancing". not very soon.

To see how and why this is, look at banks, which affect so much of the rest of the economy.

To start, China lacks the infrastructure of modern consumer finance, and is years—possibly decades—away from building it to the standards of the developed world. Outstanding consumer credit stands at about 13% of GDP, according to a 2009 study from McKinsey & Company, compared to 48% in Malaysia and 70% in South Korea.

Banks face significant structural and regulatory barriers to offering more consumer-finance products. One is the lack of national consumer credit ratings that would give banks greater confidence in their ability to measure credit risks. Another is that loan officers and managers still work from a mindset focused heavily on business lending.

Meanwhile, Beijing has lost a decade or more during which it could have allowed foreign banks to start developing a consumer-finance market. Thus Chinese banks have faced few competitive pressures to serve lower-income consumer borrowers themselves, so they haven't. Only in November did regulators allow a foreign company into this brand-new field. Dutch PPF Group will offer in-store financing for durable-goods purchases—the kind of installment plan that made its appearance in America 160 years ago.

More interesting is the supply side of the consumption equation. Rebalancing is not a matter of Chinese export factories losing a foreign customer and gaining a domestic one, Patrick Chovanec of Tsinghua University observes. Export factories are part of global supply chains in which someone else does the product development, logistics, marketing and retailing. Chinese export factories aren't equipped to do those things on their own. Rebalancing would cause them to lose foreign customers and go out of business, allowing entrepreneurs who are oriented toward domestic consumption to buy the assets.

China needs to reallocate capital and labor on a massive scale to orient itself toward producing goods and services that Chinese consumers want to consume. This will require major banking changes, especially improving access to credit for the small and medium-sized enterprises that make a modern consumption-driven economy tick. Both regulation and habit will get in the way.

The regulation involves interest rates: Government manages both deposit and lending rates in a way that guarantees banks a wide spread. This was intended to help banks earn themselves out of an earlier generation of nonperforming loans at the expense of households, which earn lower rates on savings deposits. And the policy could prove especially necessary if 2009's credit binge results in huge piles of bad debts.

But the policy hurts consumption by depressing household earnings on savings. It also depresses bank lending to small enterprises by discouraging bank risk-taking. Instead of taking a chance that some of their guaranteed profit margin might be eaten up by a nonperforming loan to a small start-up, banks can reap the entire spread by lending to larger state-owned enterprises whose debts the government implicitly or explicitly guarantees.

A related banking habit is insistence on physical collateral, often real estate, a stricture that favors asset-heavy state-owned companies and exporting manufacturers. Any other kind of business lending is more challenging, as it involves training each loan officer and his manager to evaluate a small firm's business plan and projections to reach a judgment on creditworthiness. And without clear laws in place for when uncollateralized loans go bad, banks will continue to prefer the comfort of having assets to seize if worse comes to worst.

Nature of China’s urbanization

Gang Fan provides another insightful piece on China's urbanization.

He analyzed why China's urbanization rate lags behind other countries with similar development level – he attributed this to China's Hukou system – most readers will find nothing new on this account. More interestingly, he shared his view on why China does not have urban slums as typically found in other developing countries with large mass migration. This has something to do with China's land tenure system.

For a graph on China's urbanization gap, you may find my previous post useful.

Warning indicators on US Treasuries

PIMCO's Kashkari and Rodosky show the market is flashing warning signals on US Treasuries (source: WSJ),

We can suggest market indicators that leaders should watch for warning signs:

• Increasing U.S. government debt-to-GDP ratio. From 1960 to 2007, that ratio averaged 36%. At the end of 2010, it was 62%. The Congressional Budget Office forecasts that it will climb to 100% by 2020 unless current tax and spending policies change. Research by economists Carmen Reinhart and Ken Rogoff indicates that sovereign debt begins to stifle economies' productive capacity when it passes 90% of GDP. Japan has had a ratio of greater than 150% for several years, and it has contributed to anemic growth.

• Increasing inflation expectations. The U.S. has enjoyed low inflation for two decades due to the Federal Reserve's commitment to stable prices. But if that resolve were perceived to weaken, confidence in Treasurys would decline, pushing both nominal and real yields higher. Since Fed Chairman Ben Bernanke's Jackson Hole speech in August 2010, the forward five-year annual inflation rate has increased 94 basis points to 2.90%, which is now above policy makers' unofficial target of 2%.

Reduced Treasury demand from abroad. Foreign ownership of Treasurys has increased to 55% in 2008, from 34% in 2000, providing the U.S. with cheap funding. As the U.S. continues to issue record levels of Treasurys, it will grow increasingly difficult for foreign buyers, both private and sovereign, to maintain their share. For example, foreign ownership of Treasurys has fallen to about 50% today. As foreign buyers increasingly look elsewhere, U.S. funding costs could increase, creating a drag on economic growth.

• Rapid dollar depreciation. A large and rapid drop in the value of the dollar would indicate concerns among investors in Treasurys and across the U.S. economy. Although currencies are volatile, the dollar index (DXY) has fallen by 5% or more in one month only 16 times since the index began 44 years ago. It has done so four times in the past two years. This suggests increased concern about the stability of the dollar.

• Dramatic steepening of the yield curve. A steepening yield curve—signifying that long-term rates are climbing more quickly than short-term ones—is usually a positive indicator that reflects increased optimism for future economic growth. However, if the yield curve were to steepen while economic growth expectations remained modest, such as during a period of prolonged private deleveraging, it could indicate that investors were demanding higher rates to compensate them for increased risk over time. Today's yield curve has 10-year rates about 315 basis points above overnight rates. A spread of greater than 400 basis points would be rare and potentially concerning.

Will munis default?

Muni market is in turmoil. In the following interview, Meredith Whitney gives her update on the muni market and why she thinks municipalities (not states) could default.

There should be some opportunities coming up. Investors should keep a close watch on the muni market in coming weeks.

To find out why cities got into the trouble in the first place, read this piece on today’s Journal.

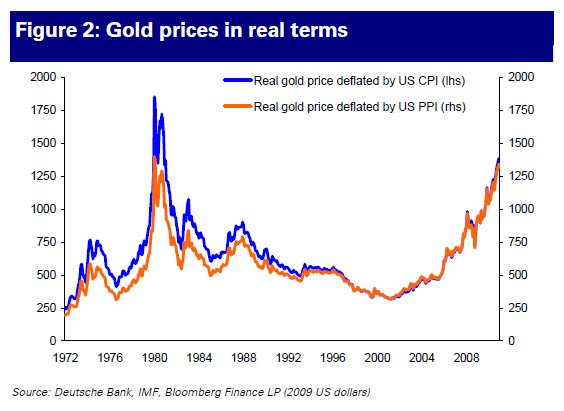

Where are we in gold?

According to DB research, gold prices on a PPI and CPI adjusted basis would need to surpass USD1,455/oz (very close now), and USD1,850/oz respectively to represent an all time high.