Home » Economy (Page 27)

Category Archives: Economy

Blog posts during summer travel

I will start some intensive traveling starting from this Thursday: first to Italy, then to China (for a month or so), then to UK. During this period, I will not update my blog as frequent as in the past, but I will still try to send out at least one post (or commentary) each week.

Have a nice summer!

Is this normal correction, or another bear coming?

After yesterday's drop, the US market formally entered correction mode (defined by 10% decline from the recent peak). In finding out what's to come next, I pulled out my tool box.

The findings are quite surprising to me. All indicators seem to point out that there is something big coming. Because most of these indicators are coincidental indicators, so I can't be absolutely sure, but I would say that the risk is clearly on the down side.

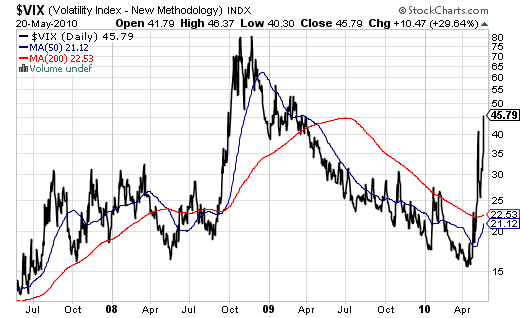

First, let's look at S&P 500 volatility index, or VIX – The sharp jump from teen-digit level in April to recent level of 45 really raised my eyebrows. I have been calling several market corrections since March 2009, but every time after a brief correction, the market turned back and resumed climbing up. The current VIX clearly broke such benign pattern – a very strong warning signal.

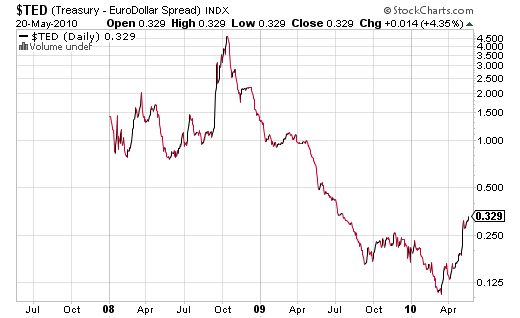

Now, let's turn to my favorite credit market indicator, the TED spread. Again the same pattern – the long declining trend since Lehman days clearly reversed direction. Because TED spread is calculated using Euro-LIBOR rate, the recent debt crisis in Europe certainly played a role. A rising TED spread signals tightening of credit markets. This won't be good for businesses (especially small businesses), the key to our nascent recovery.

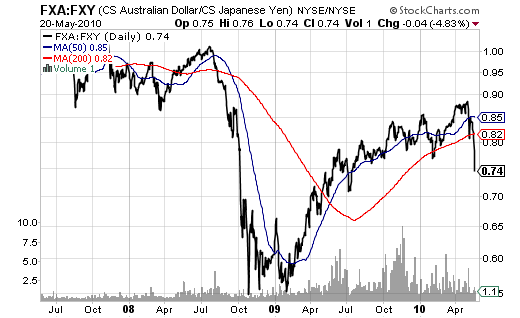

On the international front, let's look at two currency-cross indicators. First is the Aussie-Yen cross, which captures the carry trade using Japanese Yen to invest in commodities-driven economies, such as Australia and Brazil. Rising commodities currencies often signals strong economic growth or recovery ahead. The current big drop of Aussie-Yen cross indicates investors' lost of confidence for a robust of world economic recovery, especially considering China's recent clampdown of her domestic economy (housing market).

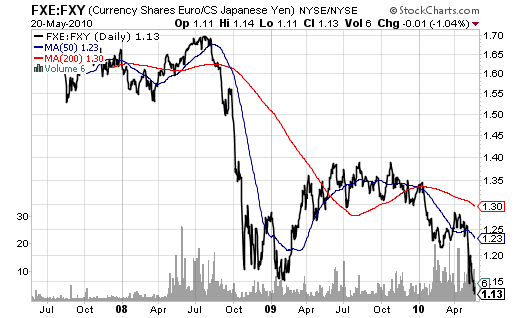

Second is the Euro-Yen cross, which is the most widely used gauge for carry trade sentiment. Again, the sharp decline of this indicator tells a story of panicking (of carry traders). In the past, the indicator is also a flight-to-quality indicator, i.e., investors scale back their risk appetite and seek for safe assets to hide.

Now, back to the question whether we are going into another bear market.

After a long climb since last March, the market (measured by SP 500 index) has risen an astonishing 82% (before recent correction) from the bottom level at 666. As as May 20, 2010, market P/E was still at 19.44, not cheap at all, compared to the long-term fair value P/E =16.4. (see graph below)

(click on the graph to enlarge)

Further, as shown in the following graph, historically, when the market falls from PE=21 level (the recent high), it at least goes down to PE=17, which means S&P 500 is likely go down to 936, at least.

(click on the graph to enlarge)

But a more careful look at the chart above, you would agree with me that recent crisis mirrors the period during the Great Depression most closely – first a big crash followed by a sharp rebound, then another big drop. The PE ratio in the second big drop during the Great Depression went from around 21 all the way to 12. If this were to happen again (I am not saying this will happen this time around), this would give S&P 500 level at 660, below the previous low (666).

You may argue this scenario is highly unlikely given the Fed's pumping money into the economy like crazy and today we have much better institutional setups compared to 1930s. But don't forget: we have one additional problem – that's the potential debt contagion from Greece and other PIIGS countries in Europe. So it doesn't hurt to take precautions.

In short, the risk is clearly on the down side. It's wise to scale back risky investments and hoard cash again, waiting for opportunities to come.

Comments are welcome.

Euro’s fall drags down commodities

Dollar's rise (Euro's fall) fueled the decline of commodities that are denominated in dollars, reports WSJ.

It is a simple relationship: As Europe's woes fuel the dollar's rise against the euro, dollar-denominated commodity prices fall.

But the malaise runs deeper. The euro zone consumed 10.5 million barrels of oil last year, according to the International Energy Agency. That was down 6% from 2008, but still more than China consumed, and 12% of global demand. Similarly, the euro zone consumes about 15% of the world's copper, much more than the U.S., according to the International Copper Study Group.

A weaker euro will do nothing to revive demand in the region. In dollar terms, oil and copper have fallen this year by 14% and 11%, respectively. In euros, oil is off by only 2%, while copper has risen slightly.

Compounding this is policy. While some might worry that quantitative easing will stoke inflation, the bigger proximate force is deflation, said Charles Dumas at Lombard Street Research, with austerity programs in countries like Greece and perennially tight German consumers. While the euro makes the zone's exports cheaper, its biggest market, the U.K., is weak.

The euro zone's drag extends to that great hope of commodities bulls everywhere: China. China exports as much to Europe as it does to the U.S. The euro's slide against the dollar-pegged yuan makes those imports more expensive at a time when Europeans are tightening their belts anyway. True, commodities are more affordable for China now, but its export markets are weak and Beijing is tightening monetary policy.

Euro-skeptics have long derided the idea of Europe as a major force. Commodities bulls, enduring big falls not just in spot prices but far out along the futures curve, must almost wish they were right.

China took off in science R&D

Given China's size and its high sustained economic growth for the past three decades, China's research (R&D) power has also grown to a level that is beyond its current income level and into the world's top league.

Following my previous post, "Is China rising as a science superpower?" , here is another post on the same issue.

First graph shows China's share of research publications in the fields of natural science (source: R&D Magazine).

While China is long perceived as the "haven for piracy" of intellectual property rights (IPR), China has been increasing its legal protection of IPR and firms (both foreign and domestic) are filing for patents at an astonishing rate.

Both the growth and the absolute number of patent filings in China have been much greater than other emerging economies.

China's total R&D as a percentage of GDP passed 1% level around year 2002, a level widely perceived as a threshold for a country's science and technology to take off.

Here is another graph from Gary Jefferson on the longer historical perspective for science & technology takeoff:

(click graphs to enlarge)

In this financial crisis, China's export sectors got hit very badly. On the optimistic side, this crisis-led creative destruction process will however expedite China's shifting away from the low-end, low-profit-margin business, into more skill-based, value-added sectors. It's reasonable to predict this fast growth in China's R&D will continue in coming years. And within one decade or so, China will rise as a true science superpower.

Mussa on the art of economic forecasting

In my previous post in September 2009, Michael Mussa deviated sharply from blue-chip forecasters and predicted a sharp rebound of US economy. Now in hindsight, although the recovery is short of V-shaped recovery, it has been quite robust.

In this interview, Michael Mussa explains why he predicted so sharply different from others (audio, about 10 mins). His prediction for GDP growth for 2010 is 4% annually, unemployment rate (currently at 9.9%) will come down to 8% by 2011, but will take another 4 years to get to 5% level.

The impact of European debt crisis on the US economy

An European sovereign debt crisis could at least affect the US economy in the following two respects.

First, the devaluation of the Euro triggered by the debt crisis will make American exports more expensive. So far this year, Euro has depreciated against US dollar by nearly 15% (from 1.44 to 1.23). This will hurt the US’ exports. During the last couple of years, government spending and exports have been the only two growth engines of the American economy. With tepid consumer demand and very weak labor market, consume- spending recovery is less likely to be quick and robust. The recovery now requires a very strong corporate spending to fill the holes left by the American consumers. One way to spur corporate spending is to sell overseas. Since Europe is the largest export market for the US, a sharp rising dollar is going to kill one of the two recovery engines of the US economy.

But the bigger worry remains in the banking sector. The financial markets across the Atlantic are highly integrated with each other. If the Greek debt crisis spills over into other bigger economies such as Spain and Italy, it will shake the European core: Germany and France, to which the US banking sector has very exposure. The following article from WSJ offers an in-depth analysis of what a potential debt contagion in Europe could impact on the US big banks.

Federal Reserve officials took pains this past week to dispel any notion that their support of Europe’s $1 trillion bailout meant U.S. taxpayer funds would be used to prop up the profligate Greeks. But in explaining the need for it to help ease financial strain, the Fed underscored that big U.S. banks remain vulnerable to Europe’s financial contagion.

During a closed-door meeting on Capitol Hill, Fed Chairman Ben Bernanke told lawmakers a European crisis would threaten U.S. banks, Sen. Richard Shelby said after the meeting. In a speech Thursday, Fed Vice Chairman Donald Kohn noted that lending systems “remain somewhat vulnerable.”

Yet big U.S. banks reported minimal exposures to Greece or Portugal, the most at-risk countries. So where does the danger lie?

The biggest threat is that the European rescue operation proves insufficient and problems spread from smaller euro-zone countries to bigger economies like France or Germany. That may threaten the viability of the euro, potentially paralyzing credit markets globally, just as happened following the collapse of Lehman Brothers.

If so, this could spell big trouble for five of the biggest U.S. banks—J.P. Morgan Chase, Bank of America, Citigroup, Goldman Sachs and Morgan Stanley. Exposures to France and Germany, along with second-tier euro countries, is equal to about 81% of the banks’ combined Tier 1 common capital, a buffer to absorb losses, according to first-quarter and year-end securities filings.

While the risk of widespread contagion is still a worst-case scenario, fears that Europe’s debt crisis is far from over and that austerity measures may slow economic growth roiled stock markets on Friday and pushed the euro to 19-month lows.

Which countries should investors in U.S. banks worry about? Take Ireland, Spain and Italy. Exposures of the big-five to these three are equal to about 25% of the banks’ combined Tier 1 common capital. In particular, U.S. banks have to worry about banks in these countries being hit. Exposure to banks in Spain and Ireland, for example, exceeds risks to government or private entities.

An even bigger risk is if any European crisis blows back on the bulwarks of the euro: France and Germany. It isn’t impossible for that to happen. French and German banks have Greek exposure of more than €110 billion ($138 billion). Analysts have predicted that any restructuring of Greek debt could force France and Germany to recapitalize some of their own banks.

The big U.S. banks had exposures to the debt of governments, banks and other entities within those two countries equal to about 61% of their combined Tier 1 common capital. Exposure of the big-five banks to French and German counterparts totals about $100 billion. And while German government bonds likely would be a haven, the U.S. banks’ exposure to German banks is greater than their government exposure.

Clearly, holdings of European bank and government debt wouldn’t be worthless, but the financial crisis showed how quickly bank fears can feed on themselves. And the need for the Fed to help backstop Europe raises the question of whether, nearly two years after the crisis, U.S. banks really have enough capital, and liquidity, to weather big global shocks.

Investors in U.S. banks should be on alert: what happens in Europe may not stay there.

Update 1 (Nov. 7, 2011)

WSJ had an article with a nice graph depicting the ties between Europe and the US:

[singlepic id=15 w=400 h=300 float=]

Euro-zone members are stuck with each other

Richard Barley of WSJ has a good analysis on that Greece is unlikely to leave (either voluntarily or be forced out of) Euro-zone. So basically, Euro-zone members are stuck. Pay attention to the highlights.

In one sense, the euro is collapsing: dropping 10% against the dollar so far this year to around $1.282 (as of May 5, now only at 1.236) as European debt markets remain gripped by crisis. But in another sense, the euro seems almost impregnable: However much some policy makers, not least in Germany, might secretly wish to see Greece suspended or thrown out of the single currency, it is almost impossible for a country to leave. The solution to Europe's sovereign-debt crisis may ultimately require more unpalatable measures.

From a legal perspective, there is no mechanism to force a country out of the currency area, European Central Bank legal counsel Phoebus Athanassiou argued in a December 2009 working paper. And while the Lisbon Treaty introduced a means for states voluntarily to withdraw from the European Union, it was silent on leaving the euro. Ultimately, that means the only way a country could leave the euro would be to quit the EU, too, according to Mr. Athanassiou. That raises the stakes far higher, since it would affect the rights and obligations of citizens and companies.

Practically, too, leaving the euro would be extremely difficult. Beyond the huge logistical problems in introducing a new currency and untangling the national central bank from the Euro system, a euro exit followed by a devaluation would likely leave a country with a mountain of unserviceable euro-denominated debt, leading to major legal wrangles, mass personal bankruptcies and huge losses for creditors.

Nor would a weak economy like Greece gain much from currency devaluation in terms of increased trade and competitiveness, given its relatively low exports and manufacturing base. Exits from the euro could also damage one of the clear benefits the single currency has brought: a far deeper corporate-bond market that last year helped nonfinancial companies raise €277 billion ($360.2 billion) of cash, according to Société Générale.

Short of voters electing new isolationist governments ready to contemplate withdrawal from the EU, it looks as if euro-zone members are stuck with each other. That makes the likely endgame, should policy makers fail to halt the current crisis, a default within the euro zone, with the potential for support from other member states that would entail, no matter how unpalatable. All the more reason why member states need to draw up far tougher fiscal rules to ensure there can never be a repeat of this crisis.