Home » Posts tagged 'China' (Page 9)

Tag Archives: China

Illusion of Chinese Bubble?

I have always been wondering whether governments, through regulation, can prevent bubbles. I tend to think this is not the case. "Smart" people (frenzy investors, investment banks, etc.) can always find loopholes and circumvent the regulation. Also remember, in democratic societies, regulations are also the bargaining outcome of various interest groups. If government can single-handedly kill the bubble, we wouldn't find any bubbles in tightly regulated economies. In fact, what we actually observe proves otherwise.

Fan Gang, a well-known economist in China, argues Chinese government has learned the lesson from Japanese bubble 20 years ago, and Chinese bubble is an illusion. (source: Project Syndicate):

BEIJING – On the eve of Chinese New Year, the People’s Bank of China (PBC) surprised the market by announcing – for the second consecutive time in a month – an increase in banks’ mandatory-reserve ratio by 50 basis points, bringing it to 16.5%. Shortly before that, China’s government acted to stop over-borrowing by local governments (through local state investment corporations), and to cool feverish regional housing markets by raising the down-payment ratio for second house buyers and the capital-adequacy ratio for developers.

This latest round of monetary tightening in China reflects the authorities’ growing concern over liquidity. In 2009, M2 money supply (a key indicator used to forecast inflation) increased by 27% year on year, and credit expanded by 34%. In January 2010, despite strict “administrative control” of financial credit lines (the PBC actually imposed credit ceilings on commercial banks), bank lending grew at an annual rate of 29%, on top of already strong expansion in the same period a year earlier. While inflation remains low, at 1.5%, it has been rising in recent months. Housing prices have also soared in most major cities.

These factors have inspired some China watchers to regard the country’s economy as a bubble, if not to predict a hard landing in 2010. But that judgment seems premature, at best.

To be sure, China may have a strong tendency to create bubbles, partly because people in a fast-growing economy become less risk-averse. Thirty years of stable growth without serious crises have made people less aware of the negative consequences of overheating and bubbles. Instead, they are so confident that they often blame the government for not allowing the economy to grow even faster.

There are also several special factors that may make China vulnerable to bubbles. China’s large state sector (which accounts for more than 30% of GDP) is usually careless about losses, owing to the soft budget constraints under which they operate. Local governments are equally careless, often failing to service their debts. In addition, various structural problems – including large and growing income disparities – are causing serious disequilibrium in the economy.

But a tendency toward a bubble need not become a reality. The good news is that Chinese policymakers are vigilant and prepared to bear down on incipient bubbles – sometimes with unpopular interventions such as the recent monetary moves.

Whatever one thinks of those measures, taking counter-cyclical policy action is almost always better than doing nothing when an economy is overheating. Whereas some policies may be criticized for being too “administrative” and failing to allow market forces to play a sufficient role, they may be the only effective way to deal with China’s “administrative entities.”

In any case, the new policies should reassure those who feared that China’s central government either would simply watch the bubble inflate or that it lacked a sufficiently independent macroeconomic policy to intervene. The consequences of burst bubbles in Japan in the 1980’s and in the United States last year are powerful reasons why China’s government has acted with such determination, while the legacy of a functioning centralized system may explain why it has proven capable of doing so decisively. After all, although modern market economics provides a sound framework for policymaking – as Chinese bureaucrats are eagerly learning – the idea of a planned economy emerged in the nineteenth century as a counter-orthodoxy to address market failures.

Some people would prefer China to move to a totally free market without regulation and management, but the recent crises have reminded everyone that free-market fundamentalism has its drawbacks, too. No one has proven able to eliminate bubbles in economies where markets are allowed to function. But if the fluctuations can be “ironed out,” as John Maynard Keynes put it, total economic efficiency can be improved.

Government investment, which represents the major part of China’s anti-crisis stimulus package, should help in this regard. Roughly 80% of the total is going to public infrastructure such as subways, railways, and urban projects, which to a great extent should be counted as long-term public goods. As such, they will not fuel a bubble by leading to immediate over-capacity in industry.

Moreover, roughly 40% of the increase in bank credit in 2009 accommodated the fiscal expansion, as projects were started prior to the budget allocations needed to finance them. Over-borrowing by local government did pose risks to the banking system and the economy as a whole, but, given China’s currently low public-debt/GDP ratio (just 24% even after the anti-crisis stimulus), non-performing loans are not a dangerous problem. Indeed, they may be easily absorbed as long as annual GDP growth remains at 8-9% and, most importantly, as long as local government borrowings are now contained.

Finally, the leverage of financial investments remains very low compared to other countries. Using bank credits to speculate in equity and housing markets is still mostly forbidden. There may be leaks and loopholes in these rules, but firewalls are in place – and are more stringently guarded than ever before.

So is a Chinese bubble still possible? Perhaps. But it has not appeared yet, and it may be adequately contained if it does.

China’s export-driven growth exaggerated

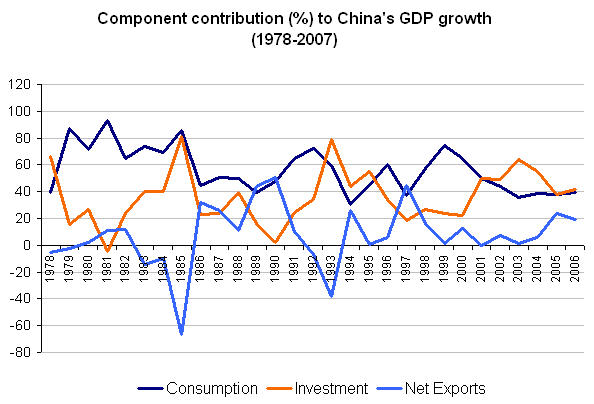

China has long been thought as export driven and heavily trade dependent. In my previous post, I told the story that China’s trade sector, if measured by value added, only accounts for less than 10% of GDP and the importance of trade is overly exaggerated. Also, according to Albert Kiedel at Carnegie Endowment, China’s GDP growth is almost independent of US GDP fluctuations (see the chart below).

Now I made another interesting graph using the data from National Bureau of Statistics (NBS): the growth component of China’s GDP growth— how investment, consumption and export have contributed China’s GDP growth historically.

(click to enlarge; source: my own calculation and NBS)

As you can see from the above graph, domestic consumption and investment have played a much larger role than net exports. In recent years, net exports’ contribution to GDP growth was only around 20% of the total. (note: the investment includes both private investment and government investment. I have to point out part of investment is surely export-related and the graph above does not capture the potential linkage between export and domestic investment. I will dig more in the future to find out). But in any case, I tend to think of China as a large open-economy (in the case of open trade and FDI, not in the sense of capital control), similar to the US. Although trade plays a very important role in China, but because the country is so large that even trade was hard hit the economy can still manage to grow at a relatively fast speed. And don’t forget China is still a relatively poor developing country; for poorer countries, faster growth came as no surprise because the strong catch-up effect often dominates.

Gaming ‘Hot Money’

I think China’s recent policy to remove the almost certainty of its currency appreciation was really a smart move. Chinese policy makers may have simply based their policy move on the concern over the grim export outlook, but the unintended consequence or byproduct of this policy is that it will actively discourage the flow of ‘hot money’ into the country.

Here below I borrow the framework of game theory to illustrate the gaming of the ‘hot money’. Hot money here refers to the short-term international capital investment, and it’s different from long-term international investment such as FDI.

The graph illustrates how a sequential game works. Chinese government chooses their first move based on their policy objectives, i.e. to discourage hot money inflow; then foreign investors respond with their best move. In this game, we implicitly assume hot money inflow is bad.

The numbers in the parenthesis show the payoff structure of the game. Chinese government first decides whether to make the prospect of currency appreciation certain, and foreign investors then choose to invest or not.

The equilibrium of the game is at the left upper corner, where Chinese government makes the appreciation uncertain and foreign investors choose not to invest as the payoff is greater for not investing (0>-1).

In hindsight, Chinese policy makers should have made the move earlier. But it’s O.K.

Now read the related article on WSJ that touches the same issue:

China’s policy makers have done a great job of creating confusion in foreign exchange markets. That might’ve been their intention all along.

Beijing has much to gain by inserting doubt into the minds of the “yuan will always rise” crowd; namely, putting an end to so-called hot money inflows that are predicated on this assumption.

![[Yuan deposits held in Hong Kong bank accounts]](https://s.wsj.net/public/resources/images/OB-CU039_YUANST_NS_20081208045802.gif)

These potentially volatile capital flows can cause inflation on the way in. Their sudden exodus, meanwhile, leaves a significant financial hole in bank balance sheets or asset prices — something China’s neighbors learned all too well during the 1997 Asian financial crisis.

Analysts think more than $150 billion of these funds made their way into China in the first half of 2008 alone, and Beijing’s made no secret of its efforts to put an end to the trend.

This is where the recent debate over the yuan’s direction could help. It started last week with a not-too-subtle move by Chinese policy makers to set the daily dollar-yuan “fixing” 0.2% higher than the day before. That was taken by some as a hint of bigger things to come, sparking trading in derivatives that profit only if the yuan is devalued in the year ahead.

The yuan itself, which trades within a band around that that daily fixing, also fell quickly. Against the dollar, the currency is down around 0.7% in the last week.

This will be unsettling for those who’ve seen the yuan’s inexorable rise as a sure-thing. Residents of Hong Kong, for example, have been converting massive amounts of their savings into yuan deposits. Over the last three years, these yuan deposits in Hong Kong banks have tripled in value to about $10 billion.

Those Hong Kongers may think twice now. They and the rest of the hot money crowd have been warned that they shouldn’t make any assumptions about Beijing’s intentions, even if a large-scale devaluation remains unlikely.