Home » Posts tagged 'Currency' (Page 2)

Tag Archives: Currency

George Soros on Chinese currency

(click to play; source: FT)

Here is the related FT article:

The prevailing exchange rate system is lopsided. China has essentially pegged its currency to the dollar while most other currencies fluctuate more or less freely. China has a two-tier system in which the capital account is strictly controlled; most other currencies don’t distinguish between current and capital accounts. This makes the Chinese currency chronically undervalued and assures China of a persistent large trade surplus.

It is no exaggeration to say that since the financial crisis, China has been in the driver’s seat. Its currency moves have had a decisive influence on exchange rates. Earlier this year when the euro got into trouble, China adopted a wait-and-see policy. Its absence as a buyer contributed to the euro’s decline. When the euro hit 120 against the dollar China stepped in to preserve the euro as an international currency. Chinese buying reversed the euro’s decline.

…

Whether it realises it or not, China has emerged as a leader of the world. If it fails to live up to the responsibilities of leadership, the global currency system is liable to break down and take the global economy with it. Either way, the Chinese trade surplus is bound to shrink but it would be much better for China if that happened as a result of rising living standards rather than a global economic decline.

Why China wanted to peg US dollar?

Let’s put aside for now the debate on whether Chinese Yuan is undervalued or not, what are the motives for China to fix its currency to the US dollar around 1995?

First comes to my mind is the need to remove currency risk in trade. As we know, almost all trade contracts are denominated in dollar, not in Yuan. Currencies tend to move a lot, and nobody likes volatility. By pegging Yuan to the dollar, Chinese firms essentially save the cost from buying expensive currency risk hedging contracts.

Second, by fixing Yuan to the dollar, more or less, China submitted its monetary policy to the Fed, i.e., the Fed’s monetary policy tends to have a great impact on China’s own monetary policy. In other words, China’s central bank largely lost its autonomy. Good thing or bad?

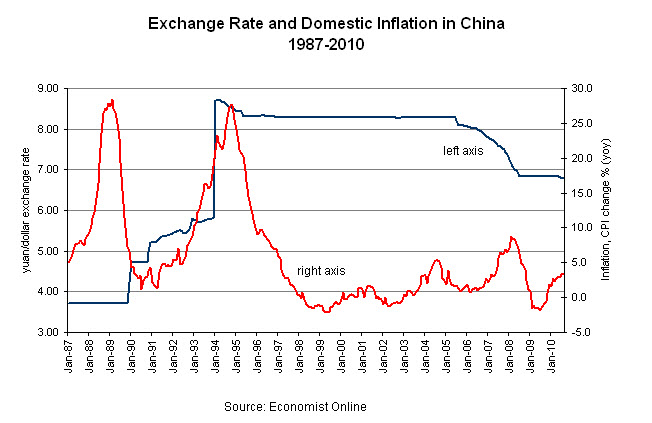

Below is a chart I just made looking at China’s domestic inflation, an important gauge for macro-stability, before and after the pegging to the US dollar.

(click on the graph to enlarge)

The chart is very dramatic. Before 1995, China’s inflation (in red) was very high and volatile. The Great Inflation in 1988 partly contributed to the 1989 students’ demonstration, which eventually led to the unfortunate Tian’anmen incident. After 1995, China’s inflation plummeted, and since then has remained quite stable – inflation never went up to over 10% again.

Was this because Chinese government suddenly improved their macro economy management skills? I don’t think so.

Here is what really happened – In essence, China achieved its macro-stability by outsourcing its monetary policy to the Fed, which has much more experiences in fighting inflation and also enjoys better credibility.

(update on Oct. 7, 2011)

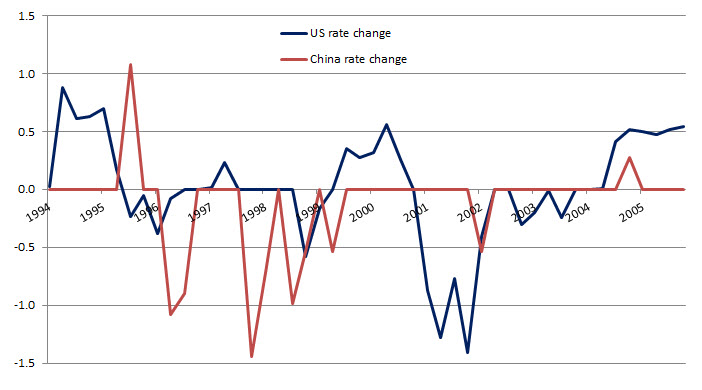

A re-look at the interest rate changes during 1995-2005 between China and the US, I changed my view that China’s inflation decline was due to its pegging to the US dollar. The more plausible explanation is China’s central bank successfully prevented inflation from rising by continuously raising interest rate, eventually pushing down inflation.

Currency appreciation will not cure trade deficit

US House passed a currency bill by a wide margin, 348-79, yesterday to penalize China’s foreign-exchange practices. The measure would allow, but not require, the U.S. to levy tariffs on countries that undervalue their currencies, which makes their goods cheaper relative to American products.

This is a highly politically-charged bill, right before the US’ mid-term election. With high unemployment rate of nearly 10% at home, blaming foreigners for one’s own backyard problem has always been the easiest solution for politicians in the past.

As I have done many analysis before, currency is not the the solution to America’s trade deficit problem, Japan’s experience back in 1980s is the best example. Neither it’s the solution for the unemployment problem. The high unemployment rate was created by the most severe recession since WWII, and by the huge bubble in housing market.

Simple economics will tell when China’s exports become more expensive, US importers will, sooner or later, choose to import from other developing countries, whose exports will become cheaper and more competitive than China. This is the so-called substitution effect. In the end, China’s trade surplus will shrink with the US, but US’ overall trade deficit will not budge. To solve the trade deficit problem, US consumers really need to save more, or consume less. The savings rate has already been rapidly increasing in the past couple of years. Sounds painful, but this is a process the US economy has to go through. Yesterday’s spendthrift means today’s frugality.

And by the way, who will get hurt most by the import tariff? The US consumers.

What about China? China should stop subsidizing exports through lower currency or tax rebate. Subsidizing exports is essentially shifting Chinese tax payer’s money and put it into American consumers’ pockets. Good deal for America; bad deal for China. The export subsidy will also distort resources allocation according to price signals, resulting in too much capital invested in the low-end export industry, with poor capital return.

Here is the latest video analysis from WSJ (quite heated):

update1: 10 am 09/30

I said above Yuan’s appreciation will shrink US trade deficit with China, but US total trade balance with the world won’t change much because of substitution effect. Now looking at the the following two charts I’ve just made, I even doubt that Yuan’s appreciation will shrink US-China trade deficit.

The first chart shows the cumulative trade deficit of US with China (in red), and Yuan-Dollar exchange rate (in black) from 2000 to 2009. Yuan had depreciated by almost 17% from 2004 to 2007, but the US trade deficits with China just kept soaring. Yuan’s appreciation did not solve the problem.

The second graph shows a similar story. The difference with the first chart is now I show the monthly trade deficits (not cumulative, in red). The blue line shows the 12-month moving average of the monthly number. The trend was clearly upward despite Yuan’s 17% appreciation during 2004-2007. Again, currency appreciation did not solve the US trade deficit problem, and it just kept growing, only until the recent recession hit, it started to trend downward.

My educated guess is that, because Chinese price is so low, even with currency appreciation and higher goods prices than before, the demand for such goods did not decrease much. In other words, American consumers may have a quite inelastic demand curve for Chinese goods. After all, majority of Chinese exports are necessity goods, not the durables, nor the luxuries.

Hong Kong – China’s currency lab

When to liberalize Chinese currency, Yuan or RMB? How to make Yuan more internationally influential? Hong Kong is being used by Chinese government as their forefront currency experiment lab. Reports WSJ:

![[HKVIEW]](https://sg.wsj.net/public/resources/images/MI-BE974_HKVIEW_NS_20100801171253.gif)

A burst of activity is under way here in the city that might be called China’s in-house research-and-development center for currency liberalization.

It’s on a tiny scale by normal standards of the $3 trillion-a-day market for foreign exchange. But in Hong Kong, banks are for the first time starting to lend yuan to one another outside mainland China and offering hedging services that weren’t available before. The result, say bankers, is reminiscent of the eurodollar market in the early 1960s, when extensive dealings in the greenback outside U.S. borders first took off.

The catalyst for this activity was an agreement signed June 19 between monetary authorities in mainland China and Hong Kong removing certain limits on usage of China’s yuan within Hong Kong. In the past, businesses were mostly confined to opening yuan accounts for trade-settlement purposes; now, accounts can be opened for any purpose. Businesses and individuals alike now can transfer yuan freely between accounts. Banks also can help businesses convert yuan without restriction.

…

With the latest liberalization move, banks in Hong Kong are now freer than ever to take all that yuan and put it to work. Some speak of linking the interest rate paid on yuan deposits to the direction of the euro or gold prices. Frances Cheung, senior strategist at Crédit Agricole Corporate & Investment Bank, foresees a market for yuan interest-rate swaps as interbank lending in the currency gains momentum.

…

Meanwhile, more and more yuan pour into Hong Kong. Monthly trade between Hong Kong and mainland China settled in yuan jumped tenfold from January to June to 13.24 billion yuan, or nearly $2 billion, and it’s set to rise more quickly since a pilot program allowing yuan settlement expanded to cover more of China in June.

Qu Hongbin, chief China economist at HSBC in Hong Kong, believes we are seeing just the tip of the iceberg. The anomaly, he says, is the fact that China conducts virtually all its trade in dollars, euros or yen. Historically, he says, “we’ve never seen a case where the world’s largest exporter uses other people’s currency for their trading.”

Will the Fed roll over asset purchases?

Two former Fed. Board of Governors (one being Fred Mishkin) discuss the issue. Fed’s action in coming weeks is likely to have a big impact on both bond market and currency market.

Mishkin took the view that it would be a mistake for the Fed to continue buying asset-backed securities or buying treasuries directly.

update 1.

Another discussion on the same issue:

What’s behind Euro’s sharp rebound?

The biggest banks are unwinding their short positions against Euro. Whenever a large number of negative bets on a currency is closed, that currency climbs.

Some of the world’s most prestigious foreign-exchange banks are ripping up their gloomy forecasts for the rallying euro.Several of the top banks in the business are backtracking on their previously dire predictions for the single currency, most of which were formed when the European monetary union itself seemed in peril during April and May this year.

Some believe this is nothing new, a natural consequence of the market’s stabilization after an extraordinary run of events for major currencies this year. However, some industry veterans say that the market is now beholden to new forces that few if any market watchers yet fully understand.

…On Monday, Switzerland’s UBS AG —the world’s second-biggest bank in foreign exchange—tore up its forecast for the euro to be trading at $1.20 against the dollar in the next month. It now expects to see the currency at around $1.28—a 6% revision.

In a separate research note, the bank described the euro as “exasperating,” adding that the currency’s rally from under $1.19 in early June to over $1.30 by late July had “wrong-footed many in the currency market.”

Other banks caught off guard include Credit Suisse, another top-10 operation, which in late July upgraded its three-month forecast for the euro’s level against the dollar to $1.30 from $1.16, citing, in part, “a more rapid than anticipated recovery in euro-area policy credibility.”

BNP Paribas SA, whose analysts have held some of the gloomiest views of any in the market, took a similar step towards the end of July. “We still expect the euro to trade lower against the dollar, but the trough should be near $1.10 rather than $0.97,” the bank said.

European regulators’ stress tests on the region’s banks have played a big role. The generally upbeat results were roundly criticized when they were released July 23, but longer-term, the tests have rebuilt confidence in Europe’s financial sector and eased nerves over the euro area’s government bonds.

In addition, concerns that the U.S. may slip back into recession, and that the U.S. Federal Reserve may be drawn into further bond purchases to support the economy, took many in the market by surprise, and hit the dollar hard.

…

“We don’t often get extremes of pessimism like we had in April and May. It was dangerous,” said Marshall Gittler, a director and chief strategist at Deutsche Bank Suisse SA in Geneva, who has been watching the currencies market since 1998.

“We have gone from an Armageddon scenario, where some people thought the euro really might break up, to euphoria, or at least a return to normality, in a very short time,” he said.

…

Mr. Brown at Mitsubishi said that the sorts of hefty revisions banks are making now are a common part of the market’s rhythm. “My broad view is that it’s no harder to predict currency movements than it ever was,” he said.

Now comes Euro’s real test…

Euro is breaking down and reached its (at least) 4-year low against US dollar, now trading around only 1.236, below the important psychology mark of 1.25, which was last reached during the period of “flight to quality” when Lehman Brothers went bust. See chart below.

I am betting Euro will go down further.

And I am re-reading this great debate between Milton Friedman and Bob Mundell – Euro may eventually survive, but it will emerge much weaker.

And let’s have a real debate on the wisdom of having a common currency even though European economies are vastly different.