How to watch China bubble

Ed. Chancellor of GMO (in Boston) has put out an excellent piece on the Chinese market and the “red flags” for investors.

The paper addresses how to identify the proper “speculative manias” and associated financial crises in the country. Chancellor sums it into key points, breaking down the bare essentials:

1. Great investment debacles generally start out with a compelling growth story.

2. A blind faith in the competence of the authorities is another typical feature of a classic mania. In other words, you can’t always trust the numbers that a government is putting out.

3. A general increase in investment is another leading indicator of financial distress. Capital is generally misspent during periods of euphoria.

4. Great booms are invariably accompanied by a surge in corruption. Countrywide, anyone?

5. Strong growth in the money supply is another robust leading indicator of financial fragility. Easy money lies behind all great episodes of speculation from the Tulip Mania of the 1630s – which was funded with IOUs – onward.

6. Fixed currency regimes often produce inappropriately low interest rates, which are liable to feed booms and end in busts.

7. Crises generally follow a period of rampant credit growth. In the boom, liabilities are contracted that cannot subsequently be repaid. The U.S. will ultimately be a perfect example of this.

8. Moral hazard is another common feature of great speculative manias. Greed isn’t necessarily good and we tend to act irresponsible during intense periods of speculation.

9. A rising stock of debt is not the only cause for concern. Investments financed with borrowed money don’t generate enough income to either service or repay the loan (what Minsky called “Ponzi finance”).

10. Dodgy loans are generally secured against collateral, most commonly real estate. Thus, a combination of strong credit growth and rapidly rising property prices are a reliable leading indicator of very painful busts.

Bergsten’s China action plan

Here is the action plan from C. Fred. Bergsten, Director of Peterson Institute of International Economics:

(Congressional Testimony) Hence I would recommend that the Administration adopt a new three-part strategy to promote early and substantial appreciation of the exchange rate of the renminbi

- Label China as a “currency manipulator” in its next foreign exchange report to the Congress on April 15 and, as required by law, then enter into negotiations with China to resolve the currency problem.

- Hopefully with the support of the European countries, and as many emerging market and developing economies as possible, seek a decision by the IMF (by a 51 percent majority of the weighted votes of member countries) to launch a “special” or “ad hoc” consultation to pursue Chinese agreement to remedy the situation promptly. If the consultation fails to produce results, the United States should ask the Executive Board to decide (by a 70 percent majority of the weighted votes) to publish a report criticizing China’s exchange rate policy.

- Hopefully with a similarly broad coalition, the United States should exercise its right to ask the WTO to constitute a dispute settlement panel to determine whether China has violated its obligations under Article XV (“frustration of the intent of the agreement by exchange action”) of the WTO charter and to recommend remedial action that other member countries could take in response. The WTO under its rules would ask the IMF whether the renminbi is undervalued, another reason why it is essential to engage the IMF centrally in the new initiative from the outse

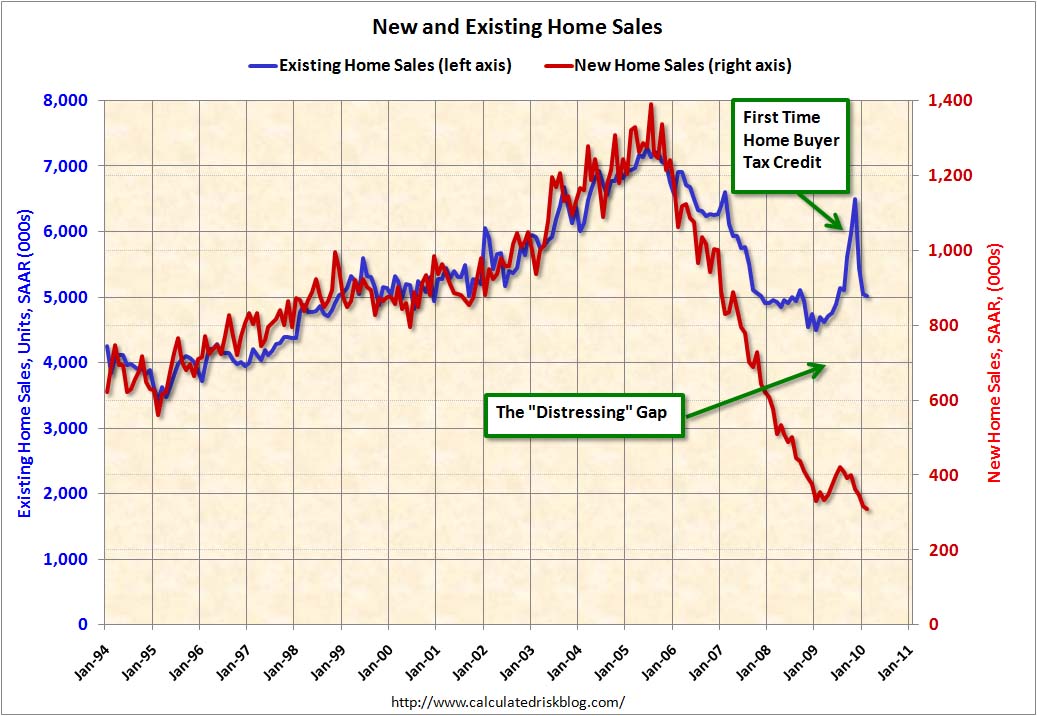

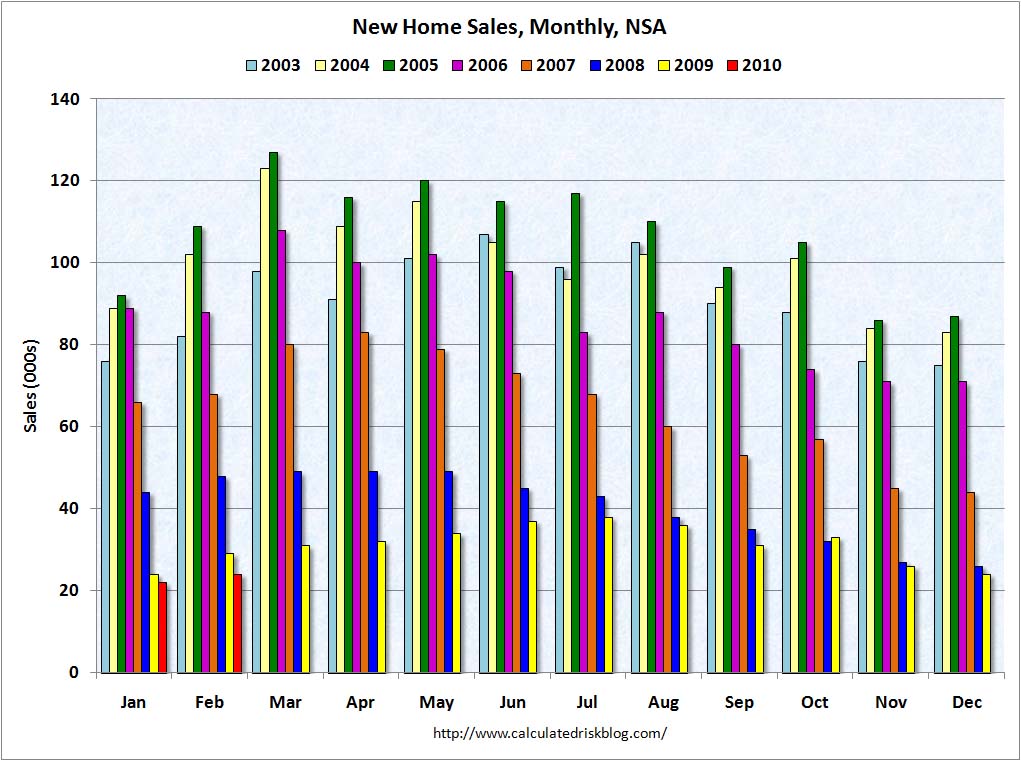

American Dream 2: Default, then Rent

The housing market is back down, in both sales of new homes and existing homes. The crawling recovery in both housing market and labor market put a deep dent on American consumers’ wealth and income. The danger still exists that the U.S. will follow Japan into a lost decade.

(click to enlarge; graph courtesy of CalculatedRisk)

American Dream of owning a house will soon turn to (arguably, has already turned) Dream v2: “default, then rent”:

People’s increasing willingness to abandon their own piece of America illustrates a paradoxical change wrought by the housing bust: Even as it tarnishes the near-sacred image of home ownership, it might be clearing the way for an economic recovery.

Thanks to a rare confluence of factors — mortgages that far exceed home values and bargain-basement rents — a growing number of families are concluding that the new American dream home is a rental.

Some are leaving behind their homes and mortgages right away, while others are simply halting payments until the bank kicks them out. That’s freeing up cash to use in other ways.

The U.S home-ownership rate has charted its biggest decline in more than two decades, falling to 67.6% as of September from a peak of 69.2% in 2004. And more renters are on the way: Credit firm Experian and consulting firm Oliver Wyman forecast that “strategic defaults” by homeowners who can afford to pay are likely to exceed one million in 2009, more than four times 2007’s level.

Stiffing the bank is bad for peoples’ credit, and bad for banks. Swelling defaults could also mean more losses for taxpayers through bank bailouts.

Analysts at Deutsche Bank Securities expect 21 million U.S. households to end up owing more on their mortgages than their homes are worth by the end of 2010. If one in five of those households defaults, the losses to banks and investors could exceed $400 billion. As a proportion of the economy, that’s roughly equivalent to the losses suffered in the savings-and-loan debacle of the late 1980s and early 1990s.

(click to play the interactive graph of Strategic Default)

The flip side of those losses, though, is massive debt relief that can help offset the pain of rising unemployment and put cash in consumers’ pockets.

For the 4.8 million U.S. households that data provider LPS Applied Analytics estimates haven’t paid their mortgages in at least three months, the added cash flow could amount to about $5 billion a month — an injection that in the long term could be worth more than the tax breaks in the Obama administration’s economic-stimulus package.

“It’s a stealth stimulus,” says Christopher Thornberg of Beacon Economics, a consulting firm specializing in real estate and the California economy. “The quicker these people shed their debts, the faster the economy is going to heal and move forward again.”

As the stigma of abandoning a mortgage wanes, the Obama administration could face an uphill battle in its effort to keep people in their homes by pressuring banks to cut their mortgage payments. Some analysts argue that’s not always the right approach, particularly if it prevents people from shedding onerous debts and starting afresh.

“The effect of these programs is often to lead homeowners to make decisions that are not in their economic best interests,” says Brent White, a law professor at the University of Arizona who has studied mortgage defaults.

![Reblog this post [with Zemanta]](https://img.zemanta.com/reblog_e.png?x-id=8e58cb77-e39e-49a8-b96a-90e6b9c63b56)

Housing market is still at depressed level

New homes built during the bubble are still not moving much; adding to the problem is the retreat of existing home sales, due to the expiration of housing credit.

The housing market still points to an anemic economic recovery for the US economy.

Graph courtesy of CalculatedRisk.

China has the most diabetics in the world

Report from WSJ. I was wondering how auto consumption has contributed to the increase. This is a sharp reminder that China should put developing better public transportation on the same importance level as developing its auto sector.

One in 10 Chinese adults have diabetes and another 16% are on the verge of developing it, according to a study published Thursday in the New England Journal of Medicine. The finding nearly equals the U.S. rate of 11%.

With 92 million diabetics, China is now home to the most cases world-wide, overtaking India. The survey found much higher rates than previous studies largely due to more rigorous testing measures. David Whiting, an epidemiologist at the International Diabetes Federation, who wasn’t involved in the study, said, “The rate of increase is much faster than we’ve seen in Europe and in the U.S.”

In China, many people are moving out of farms and into cities, where greater wealth has led to a sedentary lifestyle and sweeping diet changes, including heavily salted foods, fatty meats and sugary snacks. “As people eat more high-calorie and processed foods combined with less exercise, we see an increase of diabetes patients,’’ said Huang Jun, cardiovascular professor at the Jiangsu People’s Hospital in Nanjing who didn’t participate in the study.

What the US needs to achieve in healthcare reform

This graph tells more than thousands words.

(click to enlarge; source: Sam Cook at Columbia U)

Denmark spent half of the US does, but achieved the same outcome. Coverage is just one aspect of the reform, more attention should be paid to how to run the system more efficiently.

Union shows the crack

More Euro volatility ahead (source: WSJ):

More volatility and weakness are in store for the euro this week as European Union leaders debate whether to offer a lifeline to debt-strapped Greece.

Currency traders aren't expecting the EU summit this Thursday and Friday to yield a specific plan to support Greece, but contradictory statements in the run-up to the event will weigh on the currency. Even an agreement may not benefit the euro for long, amid problems of deflation and weak growth.

"Extreme uncertainty" surrounds this week's meeting, said Sebastien Galy, currency strategist at BNP Paribas in New York. "Nothing's going to be resolved that fast," he said, which means the euro is likely to fall further against the dollar and the yen. Since the start of the year, the common currency has lost 5.8% against the greenback.

Ahead of the summit, the Greek government has ratcheted up the pressure, warning that it can't continue to pay the high interest rates the market is demanding and threatening to turn to the International Monetary Fund instead.

The euro zone's position on involving the IMF is in flux: France and the European Central Bank want the solution to be found within the euro zone; Germany, which fears having to pay the bulk of a bailout that would be hard to sell to voters, appears to be more inclined toward drawing in the IMF.

"EU authorities seem to have explicitly broken ranks on the issue of support to Greece," said analysts at UniCredit in Milan.

Stuart Bennett, senior currency strategist at Crédit Agricole CIB in London, sees $1.36 as key for the euro. The euro held above that level for most of last week, but fell as low as $1.3503 Friday as concerns over Greece increased. That could open the way for a fall to $1.3460, he said.

Late Friday in New York, the euro was at $1.3537 from $1.3609 late Thursday. The dollar was at 90.56 yen from 90.35 yen, while the euro was at 122.60 yen from 122.96 yen. The U.K. pound was at $1.5018 from $1.5239.