Home » 2010 (Page 11)

Yearly Archives: 2010

What history tells us about the aftermath of a financial crisis

The Reinhart couple sounds the alarming bell (article from FT):

The landscape of Jackson Hole, Wyoming, where central bankers gathered at their annual conference last week, is spectacular and forbidding. Jagged peaks and vast empty spaces stretch across the horizon. For the attendees, however, it was both a vista and a metaphor. Having lived through a precipitous global economic drop, they now must forecast how steep or flat will be the incline of recovery.

Ben Bernanke, chairman of the Federal Reserve, painted a sober but reassuring picture of US prospects. The basis for sustained recovery is in place, and canny Fed officials are now alive to the dangers of both deflation and inflation. Similarly Jean Claude Trichet, head of the European Central Bank, spoke about how the dust had begun to settle on the crisis. Policymakers and financial markets seem to be looking at what comes next.

We have analysed data on numerous severe economic dislocations over the past three-quarters of a century; a record of misfortune including 15 severe post-second world war crises, the Great Depression and the 1973-74 oil shock. The result is a bracing warning that the future is likely to bring only hard choices.

Our research found real per capita gross domestic product growth tends to be much lower during the decade following crises. Unemployment rates are higher, with the most extreme increases in the most advanced economies that experienced a crisis. In 10 of the 15 episodes we studied, unemployment never fell back to its pre-crisis level, not in the following decade nor right up to the end of 2009.

It gets worse. Where house price data are available, 90 per cent of the observations over the decade after a crisis are below their level the year before the crisis. Median prices are 15 to 20 per cent lower too, with cumulative declines as large as 55 per cent. Credit is also a problem. It expands rapidly before crises, but post-crash the ratio of credit to GDP declines by an amount comparable to the pre-crisis surge. However, this deleveraging is often delayed and protracted.

Our review of the historical record, therefore, strongly supports the view that large destabilising economic events produce big changes in long-term indicators, well after the upheaval of the crisis. Up to now we have been traversing the tracks of prior crises. But if we continue as others have before, the need to deleverage will dampen employment and growth for some time to come.

Is unemployment insurance to blame?

Robert Barro thinks the expanded unemployment insurance (to 99 weeks) is the culprit for nation's high unemployment rate.

…

I want to focus here on another dimension of the Obama administration's policies: the expansion of unemployment-insurance eligibility to as much as 99 weeks from the standard 26 weeks.

The unemployment-insurance program involves a balance between compassion—providing for persons temporarily without work—and efficiency. The loss in efficiency results partly because the program subsidizes unemployment, causing insufficient job-search, job-acceptance and levels of employment. A further inefficiency concerns the distortions from the increases in taxes required to pay for the program.

In a recession, it is more likely that individual unemployment reflects weak economic conditions, rather than individual decisions to choose leisure over work. Therefore, it is reasonable during a recession to adopt a more generous unemployment-insurance program. In the past, this change entailed extensions to perhaps 39 weeks of eligibility from 26 weeks, though sometimes a bit more and typically conditioned on the employment situation in a person's state of residence. However, we have never experienced anything close to the blanket extension of eligibility to nearly two years. We have shifted toward a welfare program that resembles those in many Western European countries.

The administration has argued that the more generous unemployment-insurance program could not have had much impact on the unemployment rate because the recession is so severe that jobs are unavailable for many people. This perspective is odd on its face because, even at the worst of the downturn, the U.S. labor market featured a tremendous amount of turnover in the form of large numbers of persons hired and separated every month.

For example, the Bureau of Labor Statistics reports that, near the worst of the recession in March 2009, 3.9 million people were hired and 4.7 million were separated from jobs. This net loss of 800,000 jobs in one month indicates a very weak economy—but nevertheless one in which 3.9 million people were hired. A program that reduced incentives for people to search for and accept jobs could surely matter a lot here.

Moreover, although the peak unemployment rate (thus far) of 10.1% in October 2009 is very disturbing, the rate was even higher in the 1982 recession (10.8% in November-December 1982). Thus, there is no reason to think that the United States is in a new world in which incentives provided by more generous unemployment-insurance programs do not matter much for unemployment.

Another reason to be skeptical about the administration's stance is that generous unemployment-insurance programs have been found to raise unemployment in many Western European countries in which unemployment rates have been far higher than the current U.S. rate. In Europe, the influence has worked particularly through increases in long-term unemployment. So the key question is what happened to long-term unemployment in the United States during the current recession?

To begin with a historical perspective, in the 1982 recession the peak unemployment rate of 10.8% in November-December 1982 corresponded to a mean duration of unemployment of 17.6 weeks and a share of long-term unemployment (those unemployed more than 26 weeks) of 20.4%. Long-term unemployment peaked later, in July 1983, when the unemployment rate had fallen to 9.4%. At that point, the mean duration of unemployment reached 21.2 weeks and the share of long-term unemployment was 24.5%. These numbers are the highest observed in the post-World War II period until recently. Thus, we can think of previous recessions (including those in 2001, 1990-91 and before 1982) as featuring a mean duration of unemployment of less than 21 weeks and a share of long-term unemployment of less than 25%.

These numbers provide a stark contrast with joblessness today. The peak unemployment rate of 10.1% in October 2009 corresponded to a mean duration of unemployment of 27.2 weeks and a share of long-term unemployment of 36%. The duration of unemployment peaked (thus far) at 35.2 weeks in June 2010, when the share of long-term unemployment in the total reached a remarkable 46.2%. These numbers are way above the ceilings of 21 weeks and 25% share applicable to previous post-World War II recessions. The dramatic expansion of unemployment-insurance eligibility to 99 weeks is almost surely the culprit.

To get a rough quantitative estimate of the implications for the unemployment rate, suppose that the expansion of unemployment-insurance coverage to 99 weeks had not occurred and—I assume—the share of long-term unemployment had equaled the peak value of 24.5% observed in July 1983. Then, if the number of unemployed 26 weeks or less in June 2010 had still equaled the observed value of 7.9 million, the total number of unemployed would have been 10.4 million rather than 14.6 million. If the labor force still equaled the observed value (153.7 million), the unemployment rate would have been 6.8% rather than 9.5%.

Consider how the prospects for Democrats in the November elections would look if the unemployment rate were now only 6.8%. Obviously, this change would make all the difference, and President Obama can reasonably blame his economic advisers. They should have protected their boss by standing firm and arguing that a reckless expansion of unemployment-insurance coverage to 99 weeks was unwise economically and politically. Congressman Boehner's advice to Mr. Obama seems correct, though possibly too late to matter.

No more prop-trading at Goldman

Goldman Sachs decided to close down its prop-trading business, to conform to the new finance overhaul bill, reports WSJ.

Goldman Sachs Group Inc. has decided to close its principal-strategies unit, which does proprietary trading, in the wake of financial-overhaul regulation passed by Congress, according to a person familiar with the matter.

The widely expected decision follows J.P. Morgan Chase & Co.'s decision this week to close its proprietary-trading business. That bank started telling its proprietary traders earlier this week that it would exit that part of the business.

Proprietary trading, which involves putting a company's own capital at risk in trades, is now a relatively small part of the two companies' operations. An analyst at Citigroup has estimated that Goldman Sachs Principal Strategies has shrunk in the past three years and generates less than 1% of the company's overall trading revenue, or about $100 million to $200 million a quarter. Virtually all of Goldman Sachs' proprietary trading is done in the principal-strategies unit.

Bob Shiller on confidence and the economy

Bob Shiller, economics professor at Yale University and a pioneer in behavior finance talks about the importance of confidence in economic recovery. He thinks with lingering high unemployment, the national morale is sinking.

And we have to admit we simply do not know many things in the working of our economy.

Is US labor market no longer flexible?

One of the greatest strength of American economy is its very flexible labor market. Following my previous post on hiring mismatch in the US labor market, here is a nice piece from Economist Magazine on whether the high unemployment rate, currently at 9.5%, is more due to structural change, rather than weak demand, in American economy.

There are a few things that might have contributed to such structural rigidities in the labor market. First is the skill mismatch. Imagine how many people went into housing and construction business in this great housing bubble, how many of them can retrain themselves and find jobs in new sectors. Also imagine how many people went into financial industry. If you agree that American financial industry is also in a secular decline, this just adds more into the structural skill mismatch.

Another factor is also related to housing. Buying at peak price and with more than 35% price decline at nationwide, a lot of home owners have their home equity now under the water. The heavy mortgage debt limits people's mobility, and prevents them from taking jobs in new places.

AMERICANS are used to thinking of their job market as lithe and supple. Employment snaps back quickly after recessions. Workers routinely shuttle between industries and cities to wherever jobs are abundant. But in the past decade, the labour market has resembled an ageing athlete. Each new injury is more painful and takes longer to heal. More than a year into the current economic recovery the unemployment rate remains stuck close to 10%, raising concerns about the kind of sclerosis that continental Europe suffered in the 1980s.

The slow rehabilitation is in part because the economy suffered a trauma, not a scrape. The fall in GDP during the last recession was easily the largest of the post-war period, and output remains well below its potential. Few had expected a rapid return to full employment, but even modest expectations for jobs growth have not been met. Employment has actually fallen since the end of the recession; and unemployment would be even higher than it is were it not for discouraged would-be jobseekers quitting the workforce. Some economists now fret that other barriers besides weak demand stand between workers and jobs, and that high unemployment is partly “structural” in nature.

The case begins with some kinks in recent data. Rising GDP has not led to the fall in unemployment predicted by Okun’s Law, established in the 1960s by Arthur Okun, an economist. The figures have also departed from the Beveridge curve (named for a British economist, William Beveridge) which relates job vacancies and the jobless rate. Unemployment has failed to fall in a way consistent with the increase in job openings.

Such deviations are perhaps too short-lived to be conclusive. But they jar because there are other reasons to believe that structural obstacles to jobs growth have risen. For instance, jobless benefits have been extended to 99 weeks in some states with high unemployment, compared with the usual limit of 26 weeks. Such payments provide crucial support to the long-term jobless and help to prop up aggregate demand. But they also push up the unemployment rate by discouraging workers from looking for jobs as assiduously as they might otherwise do.

A bigger worry is that jobseekers no longer have the skills demanded by employers. Half of the 8m jobs lost went in construction and manufacturing, and those departing these industries may struggle to adapt to jobs in more vibrant areas such as education and health services. The cost of this skills mismatch is compounded by America’s housing bust. Many owe more on mortgages than their homes are worth. Households often opt to stay put rather than default, leaving them trapped in places with high unemployment and unable to move to where jobs are plentiful. The rise of the two-income household has also made workers less mobile than they were: it is harder to move in search of jobs if there are two careers to consider.

How important are these factors? Very, says Narayana Kocherlakota, president of the Federal Reserve Bank of Minneapolis. He recently caused a stir by arguing that “most” of America’s unemployment is thanks to such mismatches, and hence not easily alleviated with looser monetary policy. Most American policymakers believe that structural joblessness has risen little, if at all.

One of the few concrete estimates comes from the IMF. A recent report compared the skill levels of the unemployed with indicators of the skills required by employers, to create state-level indices of mismatches. It used local mortgage-default and foreclosure figures to estimate geographical immobility. The results suggest that each of these factors acts to magnify the impact of the other. The authors conclude that, because of these rigidities, the unemployment rate consistent with stable inflation—roughly speaking, the structural rate—rose from around 5% in 2007 to between 6% and 6.75% by 2009.

Ten predictions for the next ten years

From Bob Doll, chief equity strategist at BlakRock:

1. US equities experience high single-digit percentage total returns after the worst decade since the 1930s.

2. Recessions occur more frequently during this decade than only once a decade as occurred in the last 20 years.

3. Healthcare, information technology and energy alternatives are leading growth areas for the United States.

4. The US dollar continues to become less dominant as the decade progresses.

5. Interest rates move irregularly higher in the developed world.

6. Country self-interest leads to more trade and political conflicts.

7. An aging and declining population gives Europe some of Japan’s problems.

8. World growth is led by emerging market consumers.

9. Emerging markets weighting in global indices rises significantly.

10. China’s economic and political ascent continues.

Read more about his predictions here.

American bond in bubble?

Jeremy Siegle thinks YES,

Ten years ago we experienced the biggest bubble in U.S. stock market history—the Internet and technology mania that saw high-flying tech stocks selling at an excess of 100 times earnings. The aftermath was predictable: Most of these highfliers declined 80% or more, and the Nasdaq today sells at less than half the peak it reached a decade ago.

A similar bubble is expanding today that may have far more serious consequences for investors. It is in bonds, particularly U.S. Treasury bonds. Investors, disenchanted with the stock market, have been pouring money into bond funds, and Treasury bonds have been among their favorites. The Investment Company Institute reports that from January 2008 through June 2010, outflows from equity funds totaled $232 billion while bond funds have seen a massive $559 billion of inflows.

We believe what is happening today is the flip side of what happened in 2000. Just as investors were too enthusiastic then about the growth prospects in the economy, many investors today are far too pessimistic.

The rush into bonds has been so strong that last week the yield on 10-year Treasury Inflation-Protected Securities (TIPS) fell below 1%, where it remains today. This means that this bond, like its tech counterparts a decade ago, is currently selling at more than 100 times its projected payout.

Shorter-term Treasury bonds are yielding even less. The interest rate on standard noninflation-adjusted Treasury bonds due in four years has fallen to 1%, or 100 times its payout. Inflation-adjusted bonds for the next four years have a negative real yield. This means that the purchasing power of this investment will fall, even if all coupons paid on the bond are reinvested. To boot, investors must pay taxes at the highest marginal tax rate every year on the inflationary increase in the principal on inflation-protected bonds—even though that increase is not received as cash and will not be paid until the bond reaches maturity.

…

Those who are now crowding into bonds and bond funds are courting disaster. The last time interest rates on Treasury bonds were as low as they are today was in 1955. The subsequent 10-year annual return to bonds was 1.9%, or just slightly above inflation, and the 30-year annual return was 4.6% per year, less than the rate of inflation.

Furthermore, the possibility of substantial capital losses on bonds looms large. If over the next year, 10-year interest rates, which are now 2.8%, rise to 3.15%, bondholders will suffer a capital loss equal to the current yield. If rates rise to 4% as they did last spring, the capital loss will be more than three times the current yield. Is there any doubt that interest rates will rise over the next two decades as the baby boomers retire and the enormous government entitlement programs kick into gear?

With future government finances so precarious, private asset accumulation and dividend income must become the major sources of retirement funding. At current interest rates, government bonds will not be the answer. One hundred times earnings was the tipping point for the tech market a decade ago. We believe that the same is now true for government bonds.

Paul Krugman thinks NO.

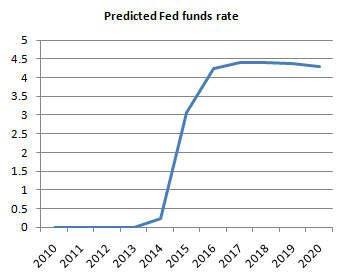

Here’s a thought for all those insisting that there’s a bond bubble: how unreasonable are current long-term interest rates given current macroeconomic forecasts? I mean, at this point almost everyone expects unemployment to stay high for years to come, and there’s every reason to expect low or even negative inflation for a long time too. Shouldn’t that imply that the Fed will keep short-term rates near zero for a long time? And shouldn’t that, in turn, mean that a low long-term rate is justified too?

Now, take the CBO projection, which calls for unemployment to fall very slowly, and core inflation to stay low for quite a while too. Here’s what it implies for the Fed funds rate, taking the zero lower bound into account:

That’s right: four years of near-zero short-term interest rates. Does a 10-year rate of 2.6 percent still sound so unreasonable? And bear in mind that I’m not using some doomsayer’s forecast; I’m using the staid folks at the CBO.

…

Here’s what I think is going on: aside from the obviously intense desire of some of the bond bubble folks to see a fiscal crisis — they’ve been planning for it, and they’re not going to take no for an answer — my sense is that a lot of people just can’t bring themselves to face the reality that we’re likely to be in a zero-interest world for a long time. They just keep assuming that the Fed is going to raise rates soon, even though there is absolutely nothing about the macro situation that would justify such a rate increase.

David Rosenberg uses “bubble-rule-of thumb” and he quotes John Rogue:

“We don’t believe there is any “bond bubble”. However, there is a bubble in people believing there is a “bond bubble”. Here’s how you will know if there is a bond bubble — ask your colleagues how many of them own bonds in their personal accounts. When nobody/almost nobody raises their hand you should be comforted in knowing that the prospects of the existence of a “bond bubble” have been reduced. By the way, this tactic has worked wonderfully for gold over the last decade.”

Blinder: Fed’s running low on ammunition

The Fed is running low on ammunition, but not completely out of it. Former vice chairman of Fed’s Board of Governors, Alan Blinder, economics professor at Princeton University, lists four weak weapons the Fed is now left with, and he analyzes how the Fed should use them, and their limitations. A very insightful piece. (source: WSJ)

You may have noticed that the complexion of the U.S. economy has turned a bit sallow of late. The Federal Reserve definitely has. At its Aug. 10 meeting, the Federal Open Market Committee (FOMC) shifted attention away from its former concern—how to tighten a bit—and toward a new concern: how to loosen a bit. By central bank standards, this turnabout came at warp speed.

Chairman Ben Bernanke has told the world that the Fed is not out of ammunition. It still has easing options, should it need to deploy them. The good news is that he’s right. The bad news is that the Fed has already spent its most powerful ammunition; only the weak stuff is left. Mr. Bernanke has mentioned three options in particular: expanding the Fed’s balance sheet again, changing the now-famous “extended period” language in its statement, and lowering the interest rate paid on bank reserves. Let’s examine each.

• From exit to re-entry. The first easing option is to create even more bank reserves by purchasing even more assets—what everyone now calls “quantitative easing.” The FOMC took a baby step in that direction at its last meeting by announcing that it would no longer let its balance sheet shrink as its holdings of mortgage-backed securities (MBS) mature and are paid off. Instead, it will reinvest the proceeds in Treasury securities.

Two distinct policy shifts are embedded in this announcement. Most obviously, the gradual shrinkage of the Fed’s balance sheet—a key component of its exit strategy—comes to a screeching halt.

Less obviously, the purpose of quantitative easing changes. When the Fed buys private-sector assets like MBS it is trying to shrink interest rate spreads over Treasurys—and thereby to lower private-sector borrowing rates such as home mortgage rates—by bidding up the prices of private assets, and so lowering their yields. Judged by this criterion, the MBS purchase program was pretty successful.

But when the Fed buys long-dated Treasury securities it is trying to flatten the yield curve instead—by bidding up the prices on long bonds. That effort also seems to have succeeded, perhaps surprisingly so given the vast size of the Treasury market. Now put the two together. By reducing its holdings of MBS and increasing its holdings of Treasurys, the Fed de-emphasizes shrinking risk spreads and emphasizes flattening the yield curve. That strikes me as a bad deal for the economy because the real problem has been high risk spreads, not high Treasury bond rates.

If the FOMC is serious about re-entry into quantitative easing, it should buy private assets, not Treasurys. Which assets? The reflexive answer is: more MBS. But with mortgage rates already so low, how much further can they fall? And would slightly lower rates revive the lifeless housing market?

To give quantitative easing more punch, the Fed may have to devise imaginative ways to purchase diversified bundles of assets like corporate bonds, syndicated loans, small business loans and credit-card receivables. Serious technical difficulties beset any efforts to do so without favoring some private interests over others. And the political difficulties may be even more severe. So the Fed will go there only with great reluctance.

• What’s in a word? The FOMC has been telling us repeatedly since March 2009 that the federal-funds rate will remain between zero and 25 basis points “for an extended period.” This phrase is intended to nudge long rates lower by convincing markets that short rates will remain near zero for quite some time.

The Fed’s second option for easing is to adopt new language that implies an even longer-lasting commitment to a near-zero funds rate.

Frankly, I’m dubious there is much mileage here. What would the new language be? Hyperextended? Mr. Bernanke is a clever man; perhaps he can turn a better phrase. But market participants already interpret the “extended period” as lasting deep into 2011 or beyond. How much longer could any new language stretch that belief?

• Interest on reserves. In October 2008, the Fed acquired the power to pay interest on the balances that banks hold on reserve at the Fed. It has been using that power ever since, with the interest rate on reserves now at 25 basis points. Puny, yes, but not compared to the yields on Treasury bills, federal funds, or checking accounts. And at that puny interest rate, banks are voluntarily holding about $1 trillion of excess reserves.

So the third easing option is to cut the interest rate on reserves in order to induce bankers to disgorge some of them. Unfortunately, going from 25 basis points to zero is not much. But why stop there? How about minus 25 basis points? That may sound crazy, but central bank balances can pay negative rates of interest. It’s happened.

Charging 25 basis points for storage should get banks sending money elsewhere. The question is where. If they just move money from their accounts at the Fed to the federal funds market, the funds rate will fall—but it can’t fall far. After all, it has averaged only 16 basis points since December 2008. If banks move the money into Treasury bills instead, the T-bill rate will fall. But even if it drops all the way to zero, that’s not a big change from its 12-month average of 11 basis points (for three-month bills). So charging 25 basis points is no panacea.

But suppose some fraction of the $1 trillion in excess reserves was to find its way into lending. Even if it’s only 10%, that would boost bank lending by 3%-4%. Better than nothing.

• A fourth way out. There is a fourth weapon, which the Fed chairman has not mentioned: easing up on healthy banks that are willing to make loans. Given bank examiners’ record of prior laxity, it is understandable that they have now turned into stern disciplinarians, scowling at any banker who makes a loan that might lose a nickel. That tough attitude keeps the banks safe, but it also starves the economy of credit.

Well, quite a few of those bank examiners happen to work for the Fed. It would probably do some good, maybe even a lot, if word came down from on high that some modest loan losses are not sinful, but rather a normal part of the lending business.

So that’s the menu. The Fed had better study it carefully, for if the economy doesn’t perk up, it will soon be time to fire the weak ammunition.