Home » Posts tagged 'China' (Page 5)

Tag Archives: China

How much has Chinese Yuan really appreciated?

According to Economist Magazine, adding rising labor cost, Chinese Yuan has appreciated by nearly 50% against US dollar since 2005.

A real exchange rate takes account of price movements in each country. If prices rise faster in China than in America, China’s real exchange rate goes up, even if its nominal exchange rate stays the same. That’s because higher prices at home make China’s firms less competitive abroad, just as if their currency had gone up.To calculate the real exchange rate, you need a gauge of prices in each country. Many economists use the consumer-price index (CPI). But the CPI contains lots of goods and services (such as housing rents) that cannot be traded across borders.

Our measure of the real exchange rate, which we will regularly update, offers a more direct measure of competitiveness by looking instead at unit labour costs: the price of labour per widget. These costs go up when wages rise or productivity (widgets per worker) falls. In American manufacturing, unit labour costs have risen by less than 4% since the first quarter of 2005, according to the Bureau of Labour Statistics. In Chinese industry they have risen by 25% over that period, according to our sums.

Something is happening in China

There appears to be some heated debate going on within the Chinese Communist Party (CCP) regarding the future direction of China’s political reform.

CCP censorship recently ordered Internet sites and news organizations to delete all references to a recent rare interview of Premier Wen Jiabao by CNN. In that Sept. 23 interview (shown below), Mr. Wen said that “the people’s wishes for and needs for democracy and freedom are irresistible.”

According to yesterday’s New York Times, China’s main Communist Party newspaper, People’s Daily, bluntly rejected calls for speedier political reform, publishing a front-page commentary that said any changes in China’s political system should not emulate Western democracies, but “consolidate the party’s leadership so that the party commands the overall situation.”

A cheer for Premier Wen – near the end of the interview, Wen mentioned one of his most-read book is “The Theory of Moral Sentiments” by Adam Smith. WOW!

George Soros on Chinese currency

(click to play; source: FT)

Here is the related FT article:

The prevailing exchange rate system is lopsided. China has essentially pegged its currency to the dollar while most other currencies fluctuate more or less freely. China has a two-tier system in which the capital account is strictly controlled; most other currencies don’t distinguish between current and capital accounts. This makes the Chinese currency chronically undervalued and assures China of a persistent large trade surplus.

It is no exaggeration to say that since the financial crisis, China has been in the driver’s seat. Its currency moves have had a decisive influence on exchange rates. Earlier this year when the euro got into trouble, China adopted a wait-and-see policy. Its absence as a buyer contributed to the euro’s decline. When the euro hit 120 against the dollar China stepped in to preserve the euro as an international currency. Chinese buying reversed the euro’s decline.

…

Whether it realises it or not, China has emerged as a leader of the world. If it fails to live up to the responsibilities of leadership, the global currency system is liable to break down and take the global economy with it. Either way, the Chinese trade surplus is bound to shrink but it would be much better for China if that happened as a result of rising living standards rather than a global economic decline.

Why China wanted to peg US dollar?

Let’s put aside for now the debate on whether Chinese Yuan is undervalued or not, what are the motives for China to fix its currency to the US dollar around 1995?

First comes to my mind is the need to remove currency risk in trade. As we know, almost all trade contracts are denominated in dollar, not in Yuan. Currencies tend to move a lot, and nobody likes volatility. By pegging Yuan to the dollar, Chinese firms essentially save the cost from buying expensive currency risk hedging contracts.

Second, by fixing Yuan to the dollar, more or less, China submitted its monetary policy to the Fed, i.e., the Fed’s monetary policy tends to have a great impact on China’s own monetary policy. In other words, China’s central bank largely lost its autonomy. Good thing or bad?

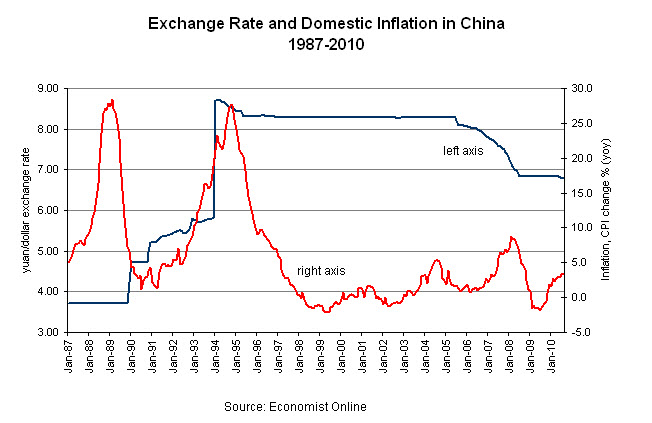

Below is a chart I just made looking at China’s domestic inflation, an important gauge for macro-stability, before and after the pegging to the US dollar.

(click on the graph to enlarge)

The chart is very dramatic. Before 1995, China’s inflation (in red) was very high and volatile. The Great Inflation in 1988 partly contributed to the 1989 students’ demonstration, which eventually led to the unfortunate Tian’anmen incident. After 1995, China’s inflation plummeted, and since then has remained quite stable – inflation never went up to over 10% again.

Was this because Chinese government suddenly improved their macro economy management skills? I don’t think so.

Here is what really happened – In essence, China achieved its macro-stability by outsourcing its monetary policy to the Fed, which has much more experiences in fighting inflation and also enjoys better credibility.

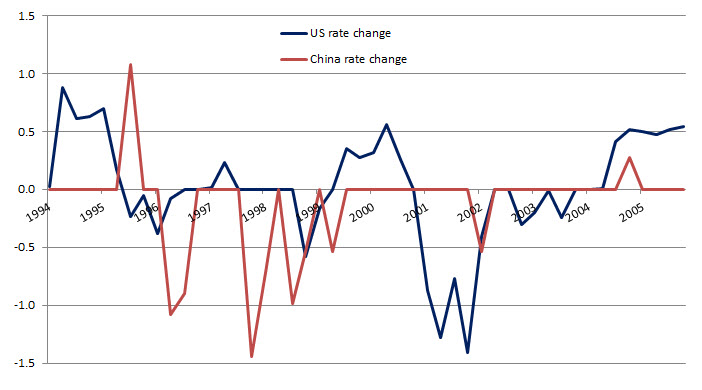

(update on Oct. 7, 2011)

A re-look at the interest rate changes during 1995-2005 between China and the US, I changed my view that China’s inflation decline was due to its pegging to the US dollar. The more plausible explanation is China’s central bank successfully prevented inflation from rising by continuously raising interest rate, eventually pushing down inflation.

Currency appreciation will not cure trade deficit

US House passed a currency bill by a wide margin, 348-79, yesterday to penalize China’s foreign-exchange practices. The measure would allow, but not require, the U.S. to levy tariffs on countries that undervalue their currencies, which makes their goods cheaper relative to American products.

This is a highly politically-charged bill, right before the US’ mid-term election. With high unemployment rate of nearly 10% at home, blaming foreigners for one’s own backyard problem has always been the easiest solution for politicians in the past.

As I have done many analysis before, currency is not the the solution to America’s trade deficit problem, Japan’s experience back in 1980s is the best example. Neither it’s the solution for the unemployment problem. The high unemployment rate was created by the most severe recession since WWII, and by the huge bubble in housing market.

Simple economics will tell when China’s exports become more expensive, US importers will, sooner or later, choose to import from other developing countries, whose exports will become cheaper and more competitive than China. This is the so-called substitution effect. In the end, China’s trade surplus will shrink with the US, but US’ overall trade deficit will not budge. To solve the trade deficit problem, US consumers really need to save more, or consume less. The savings rate has already been rapidly increasing in the past couple of years. Sounds painful, but this is a process the US economy has to go through. Yesterday’s spendthrift means today’s frugality.

And by the way, who will get hurt most by the import tariff? The US consumers.

What about China? China should stop subsidizing exports through lower currency or tax rebate. Subsidizing exports is essentially shifting Chinese tax payer’s money and put it into American consumers’ pockets. Good deal for America; bad deal for China. The export subsidy will also distort resources allocation according to price signals, resulting in too much capital invested in the low-end export industry, with poor capital return.

Here is the latest video analysis from WSJ (quite heated):

update1: 10 am 09/30

I said above Yuan’s appreciation will shrink US trade deficit with China, but US total trade balance with the world won’t change much because of substitution effect. Now looking at the the following two charts I’ve just made, I even doubt that Yuan’s appreciation will shrink US-China trade deficit.

The first chart shows the cumulative trade deficit of US with China (in red), and Yuan-Dollar exchange rate (in black) from 2000 to 2009. Yuan had depreciated by almost 17% from 2004 to 2007, but the US trade deficits with China just kept soaring. Yuan’s appreciation did not solve the problem.

The second graph shows a similar story. The difference with the first chart is now I show the monthly trade deficits (not cumulative, in red). The blue line shows the 12-month moving average of the monthly number. The trend was clearly upward despite Yuan’s 17% appreciation during 2004-2007. Again, currency appreciation did not solve the US trade deficit problem, and it just kept growing, only until the recent recession hit, it started to trend downward.

My educated guess is that, because Chinese price is so low, even with currency appreciation and higher goods prices than before, the demand for such goods did not decrease much. In other words, American consumers may have a quite inelastic demand curve for Chinese goods. After all, majority of Chinese exports are necessity goods, not the durables, nor the luxuries.

Is America in paradigm shift?

Long recession, high unemployment. Will the long ailing economy eat away American optimism?

Almost 3 years into recession (technically, the recession may have ended in summer of 2009), the current recovery looks much dimmer than previous ones (see details in the following article). In 1970s, there was also a lot of pessimism. Back then, the problem was high inflation and high unemployment, or the so-called “stagflation”. Now, we are facing a much worse scenario, the threat of deflation combined with high unemployment. With current employment trend, we will probably still be stuck with 9% unemployment rate by the mid of the next year. People started to feel the dent psychologically, and this pessimism is so easy to spread, believe me.

For contrarian investors out there, this is your best time looking out for opportunities. But before that, let’s take a minute to read this nice piece from the Journal, “The End of American Optimism“, by Mortimer Zuckerman:

Our brief national encounter with optimism is now well and truly over. We have had the greatest fiscal and monetary stimulus in modern times. We have had a whole series of programs to pay people to buy cars, purchase homes, pay off their mortgages, weatherize their homes, and install solar paneling on their roofs. Yet the recovery remains feeble and the aftershocks of the post-bubble credit collapse are ongoing.

We are at least 2.5 million jobs short of getting back to the unemployment rate of under 8% promised by the Obama administration. Concern grows that we are looking at a double-dip recession and hovering on the brink of a destructive deflation. Things are bad enough for Federal Reserve Chairman Ben Bernanke to have characterized the economic outlook late last month as “unusually uncertain.”

Are we at the end of the post-World War II period of growth? Tons of money have been shoveled in to rescue reckless banks and fill the huge hole in the economy, but nothing is working the way it normally had in all our previous crises.

Rather, we are in what a number of economists are referring to as the “new normal.” This is a much slower-growing economy that, recent surveys have revealed, is causing many Americans to distance themselves from the long-held assumption that their children will have it better than they.

What was thought to be normal in the context of post-World War II recoveries? One is that four quarters into the recovery, real GDP would expand at an annual rate over 6%. We are coming out of the current recession at a 2.4% growth rate.

We did enjoy a GDP boost from a buildup of inventories anticipating a recovery at normal speed, but it didn’t happen. David Rosenberg, chief economist of Gluskin Sheff, regards it as “frightening” that whereas the “normal” rate of increase in final sales is 4% annually, this time sales have averaged only 1.2%, the weakest revival in recorded history.

At this point after the onset of a recession, employment payrolls have typically exceeded 700,000 jobs above the previous peak. In this recession, we are still down roughly eight million jobs from the December 2007 peak. As for consumer confidence, the Conference Board survey shows an average a full 20 points below the average lows of previous recessions.

There seems to be a structural change in the American economy. The relationship of household debt to income has proven unsustainable. The ratio is normally established somewhere below 100%, but in 2007 the debt ratio hit 131% of income. It has now fallen to 122%, but at this pace it would take another five years to bring it under 100%. The pre-bubble norm was 70%. To get to this ratio again, debt would have to be reduced by about $6 trillion.

In the meantime, we may well be looking at a vicious cycle of defaults that in turn would produce credit tightening and still more economic weakness—compounding the caution among borrowers, lenders and public financial authorities.

The most obvious source of distress right now is lack of payroll growth, and it’s likely to get worse. Real unemployment today is well above the headline number of 9.5%. That number held steady only because 1,115,000 people gave up hope of finding work and left the labor force in the last three months. Otherwise the headline unemployment rate would have been around 10.4%.

Now there are at least 14.5 million Americans still searching for work: 1.4 million of them have been jobless for more than 99 weeks, 6.5 million have been jobless for over 27 weeks. This is a stunning reflection of the longer-term unemployment we are coping with.

…The Obama administration projects the unemployment rate will drop to 8.7% by the end of next year and 6.8% by 2013. That is totally unrealistic. It means we would have to add nearly 300,000 jobs a month over the next three years. At the rate we’re going, it will take anywhere from six to nine years to climb out of this hole. The labor market may be improving, but the pace is glacial.

If there is one great policy failure of this recession, it’s that we have not used the crisis to introduce structural reforms. For example, we have a gross mismatch of available skills and demonstrable needs. Businesses struggle to find the skills and talents that are needed to compete in this new world. Millions drawing the dole to sit around should be in training for the jobs of the future that require higher educational skills.

Given that nearly eight in 10 new jobs, according to the administration, will require work-force training or higher education, it furthermore makes no sense that we have reversed the traditional American policy of welcoming skilled immigrants and integrating them into our economy. Because of a recrudescent nativism, we send home thousands upon thousands of foreign students who have gotten masters and doctoral degrees in the hard sciences at American universities. These are people who create jobs, not displace them. The incorporation of immigrants used to be one of the core competencies of our economy. It’s time to return to that successful model.

Higher education is another critical issue. As President Obama pointed out last week in his speech at the University of Texas, we have fallen from first to 12th in college graduation rates for young adults. The unemployment rate for those who have never gone to college is almost double what it is for those who have.

Education may be the key economic issue of our time, Mr. Obama said in his speech, for “countries that out-educate us today . . . will out-compete us tomorrow.” To improve our performance will involve massive increases in scholarship support for higher education, and an increase in H-1B visas for foreign students who get M.A.s and Ph.D.s in the hard sciences.

But if the economic scene these days is daunting, the political scene is downright depressing. We have a paralyzed system. Neither the Democrats nor the Republicans seem able to find common ground to address what is clearly going to be an ongoing employment crisis. Finding that common ground is a job opportunity for real leaders.

Now let’s watch this interview of PIMCO’s El-Erian, the pioneer of the fancy phrase “New Normal”.

Update 1. David Rosenberg WSJ interview, in which Rosenberg explains his position of why the risk of US economy faltering is quite high, and what’s the best solution to revitalize the economy (this is a very informative piece, will be very useful for the macro-type).

So, if America is in a paradigm shift, what does this mean for China? In the past couple of months, I have been traveling in China, talking with fellow economists. There seemed to be a consensus that this recession is also the historical dividing line on China’s economic development path – China is also in a paradigm shift, moving away from a heavily export-oriented economy to a more consumption-domestic oriented economy.

The world is changing fast…

Demographics and Wealth of Nations

Following my previous post, “India needs manufacturing“, in which future population growth trend was analyzed, today I post another analysis from WSJ’s David Wessel on the relationship between demographics and nation’s wealth. Before that, I would like to give some background.

China’s huge population was long thought to be a development burden for the country. High population density puts all kinds of resources under pressure – water, energy, environment, traffic, etc. And if you take a static view, more population simply leads to lower living standards (if you measure living standards simply by GDP per capita). Simple math shows despite the fact that China is the second largest economy in the world (with total GDP 1/3 of the US), China’s GDP per capita is only 1/10 of the United States, as its population is 3 1/2 times larger.

China’s population surge during the second half of the 20th century was largely man-made. After 1949, when China’s Communist Party established People’s Republic, there was a big fear that the US may invade mainland China, along with the defeated Nationalist Party. During the era of conventional warfare, the size of army mattered. Chairman Mao, China’s paramount first-generation leader, encouraged every Chinese family to have more children – three, four, or even more. Such policy rendered probably the sharpest population growth in China’s modern history.

China’s policymakers soon realized they made a huge mistake. The immediate concern was how to feed the rising population when China was still in total blockage under Western Sanction (like today’s North Korea). The deliberation at the highest level then manufactured China’s unique “One Child Policy” (OCP), now worldly famous – which went into effect since mid 1970s, and got really tough since early 1980s. In urban China, OCP is strictly enforced; in rural China, it is more relaxed, especially when the first baby happens to be a girl.

Now after more than 30 years, Chinese policymakers had another problem – The rapidly shrinking young labor force. Over the past 30 years, China’s huge labor reserve (or cheap labor) has contributed a great deal to her fast economic growth. Ironically, once the growth engine started, population turned out to be a growth dividend, not a burden. China’s huge population also attracted tremendous foreign investments – who would not want a bite in the largest domestic market in the world?

But the ‘young’ developing China is forecast to face ageing problem much sooner than most countries at its development stage. To replenish population, the fertility rate should stay at least 2. Any rate below 2 means declining population (this assumes birth rate and death rate are roughly the same, but if people live longer, this will generate a larger share of older population). For thirty years, China’s fertility rate has only been slightly above 1. OCP effectively controlled China’s population growth, but also put China onto a “fast lane” toward ageing society.

Let’s get to details: One-Child Policy started roughly around 1980, so the first cohort of young population (about 20 years old) entered labor force around year 2000, that’s when China suffered its first dent on labor force. It’s no coincidence that during the same time various reports surfaced that manufacturing firms in China’s east coast started to feel labor shortage, defying the popular image that China seemed to have unlimited labor supply. The shrinking labor supply will become more severe when the last large cohort of population born right before OCP exits the manufacturing. I assume this is going to happen from now to the next five years (2010-2015), when most of these workers reach their middle-age (35 to 40). With more working experiences and skills, especially, the migrant workers in this group will seek more stable income and better location with equal social benefits. This often means exits from coastal manufacturing.

China’s young labor force will continue to shrink until 20 years after the major policy reversal. The policy reversal now in effect is to allow qualified couples to have up to two children, if both husband and wife are the only child in their own families. Let’s assume these couples will have their children between 25 and 35 years old (or between year 2005 to 2015 for the first cohort). Only when their children grow old enough to join labor force, i.e, when they become abut 20 years old (or between 2025 and 2035), will China’s young labor force start to grow again. This simply means within roughly a 30-year range, from 2000 to 2030, China’s young labor force will continuously trend downward. For a country still at its early development stage, this forecast should sound high alert to policy makers.

If you want to know about the role of population in country’s growth and development, feel free to download my lecture notes on the population theory. Economist Magazine also has a terrific article, “Does Population Matter?”

Now without further adieu, I introduce you to David Wessel’s analysis on the “Demographics and Nation’s Wealth“. Pay special attention to the US’ future demographic trend, and what can we learn from it.

Demography is not destiny. In 1300, China was bigger than Europe and had the world’s most sophisticated technology. But China blew it. By 1850, its population was 65% larger than Europe’s, but—thanks to the Industrial Revolution—Europeans were far richer.

Yet demography does matter. “We never pay enough attention to demography because it’s so long term,” says Dominique Strauss-Kahn, head of the International Monetary Fund. So turn for a moment from angst about the disappointing pace of the economic recovery and daunting government budget deficits, and look over the horizon.

Over the next 40 years, Japan and Europe will see working-age populations shrink by 30 million and 37 million, respectively, according to United Nations projections. Birth rates are low and so many of their people are already elderly.

![[Capital]](https://sg.wsj.net/public/resources/images/NA-BH438_Capita_NS_20100811192813.gif)

China’s working-age population will keep growing for 15 years or so, then turn down, the result of its one-child policy and the tendency of birth rates to fall as incomes rise. In 2050, the U.N. projects, China will have 100 million fewer workers than it does today. India’s population, in contrast, will grow by 300 million working-age persons over the next 40 years.

The U.S. is in between, benefiting from a higher birth rate and younger populations than Europe and Japan and more immigration. It is projected to add 35 million working-age persons by 2050.

So what?

History, as interpreted by modern economists pondering the mysteries of growth, teaches that more people lead to more ideas. And unlike land or oil, ideas can be used by more than one person simultaneously. Before countries began sharing ideas, the biggest had the most rapid technological progress. Now, trade, travel and the Internet speed new ideas around the globe ever-more rapidly. So the benefits are dispersed. Belgium is rich not because it is big or has invented a lot, but because it has the wherewithal to employ technology invented by others, notes Michael Kremer of Harvard University. Zaire is bigger, but lacks the wherewithal.

…

“China’s population is roughly equal to that of the U.S., Europe and Japan combined,” optimistic Stanford University economists Chad Jones and Paul Romer observed recently in an academic journal. “Over the next several decades, the continued economic development of China might plausibly double the number of researchers throughout the world pushing forward the technological frontier. What effect will this have on incomes in countries that share ideas with China in the long run?” Somewhere between a lot and really a lot, they say. In fact, they say that even if the U.S. had to bear all the costs of mitigating the added carbon emitted by a rapidly developing China, ideas generated by the Chinese would boost U.S. per capita income enough to more than compensate.

…

For China, the challenge is to build social structures and retirement schemes to sustain a growing cadre of old folks that, unlike previous generations, won’t be able to rely so much on its children for support. Today, 1.4% of Chinese are over age 80; in 2050, 7.2% will be, the U.N. projects.

…

And the U.S.? For all today’s gloom, it may be in the sweet spot. A growing population, an openness to ambitious immigrants and trade (if not disrupted by xenophobic politics) and strong productivity growth (if sustained) could lift living standards and bring faster growth, which would reduce big government budget deficits far easier for the U.S. than for slower growing Europe and Japan.

Hong Kong – China’s currency lab

When to liberalize Chinese currency, Yuan or RMB? How to make Yuan more internationally influential? Hong Kong is being used by Chinese government as their forefront currency experiment lab. Reports WSJ:

![[HKVIEW]](https://sg.wsj.net/public/resources/images/MI-BE974_HKVIEW_NS_20100801171253.gif)

A burst of activity is under way here in the city that might be called China’s in-house research-and-development center for currency liberalization.

It’s on a tiny scale by normal standards of the $3 trillion-a-day market for foreign exchange. But in Hong Kong, banks are for the first time starting to lend yuan to one another outside mainland China and offering hedging services that weren’t available before. The result, say bankers, is reminiscent of the eurodollar market in the early 1960s, when extensive dealings in the greenback outside U.S. borders first took off.

The catalyst for this activity was an agreement signed June 19 between monetary authorities in mainland China and Hong Kong removing certain limits on usage of China’s yuan within Hong Kong. In the past, businesses were mostly confined to opening yuan accounts for trade-settlement purposes; now, accounts can be opened for any purpose. Businesses and individuals alike now can transfer yuan freely between accounts. Banks also can help businesses convert yuan without restriction.

…

With the latest liberalization move, banks in Hong Kong are now freer than ever to take all that yuan and put it to work. Some speak of linking the interest rate paid on yuan deposits to the direction of the euro or gold prices. Frances Cheung, senior strategist at Crédit Agricole Corporate & Investment Bank, foresees a market for yuan interest-rate swaps as interbank lending in the currency gains momentum.

…

Meanwhile, more and more yuan pour into Hong Kong. Monthly trade between Hong Kong and mainland China settled in yuan jumped tenfold from January to June to 13.24 billion yuan, or nearly $2 billion, and it’s set to rise more quickly since a pilot program allowing yuan settlement expanded to cover more of China in June.

Qu Hongbin, chief China economist at HSBC in Hong Kong, believes we are seeing just the tip of the iceberg. The anomaly, he says, is the fact that China conducts virtually all its trade in dollars, euros or yen. Historically, he says, “we’ve never seen a case where the world’s largest exporter uses other people’s currency for their trading.”