Ten predictions for the next ten years

From Bob Doll, chief equity strategist at BlakRock:

1. US equities experience high single-digit percentage total returns after the worst decade since the 1930s.

2. Recessions occur more frequently during this decade than only once a decade as occurred in the last 20 years.

3. Healthcare, information technology and energy alternatives are leading growth areas for the United States.

4. The US dollar continues to become less dominant as the decade progresses.

5. Interest rates move irregularly higher in the developed world.

6. Country self-interest leads to more trade and political conflicts.

7. An aging and declining population gives Europe some of Japan’s problems.

8. World growth is led by emerging market consumers.

9. Emerging markets weighting in global indices rises significantly.

10. China’s economic and political ascent continues.

Read more about his predictions here.

American bond in bubble?

Jeremy Siegle thinks YES,

Ten years ago we experienced the biggest bubble in U.S. stock market history—the Internet and technology mania that saw high-flying tech stocks selling at an excess of 100 times earnings. The aftermath was predictable: Most of these highfliers declined 80% or more, and the Nasdaq today sells at less than half the peak it reached a decade ago.

A similar bubble is expanding today that may have far more serious consequences for investors. It is in bonds, particularly U.S. Treasury bonds. Investors, disenchanted with the stock market, have been pouring money into bond funds, and Treasury bonds have been among their favorites. The Investment Company Institute reports that from January 2008 through June 2010, outflows from equity funds totaled $232 billion while bond funds have seen a massive $559 billion of inflows.

We believe what is happening today is the flip side of what happened in 2000. Just as investors were too enthusiastic then about the growth prospects in the economy, many investors today are far too pessimistic.

The rush into bonds has been so strong that last week the yield on 10-year Treasury Inflation-Protected Securities (TIPS) fell below 1%, where it remains today. This means that this bond, like its tech counterparts a decade ago, is currently selling at more than 100 times its projected payout.

Shorter-term Treasury bonds are yielding even less. The interest rate on standard noninflation-adjusted Treasury bonds due in four years has fallen to 1%, or 100 times its payout. Inflation-adjusted bonds for the next four years have a negative real yield. This means that the purchasing power of this investment will fall, even if all coupons paid on the bond are reinvested. To boot, investors must pay taxes at the highest marginal tax rate every year on the inflationary increase in the principal on inflation-protected bonds—even though that increase is not received as cash and will not be paid until the bond reaches maturity.

…

Those who are now crowding into bonds and bond funds are courting disaster. The last time interest rates on Treasury bonds were as low as they are today was in 1955. The subsequent 10-year annual return to bonds was 1.9%, or just slightly above inflation, and the 30-year annual return was 4.6% per year, less than the rate of inflation.

Furthermore, the possibility of substantial capital losses on bonds looms large. If over the next year, 10-year interest rates, which are now 2.8%, rise to 3.15%, bondholders will suffer a capital loss equal to the current yield. If rates rise to 4% as they did last spring, the capital loss will be more than three times the current yield. Is there any doubt that interest rates will rise over the next two decades as the baby boomers retire and the enormous government entitlement programs kick into gear?

With future government finances so precarious, private asset accumulation and dividend income must become the major sources of retirement funding. At current interest rates, government bonds will not be the answer. One hundred times earnings was the tipping point for the tech market a decade ago. We believe that the same is now true for government bonds.

Paul Krugman thinks NO.

Here’s a thought for all those insisting that there’s a bond bubble: how unreasonable are current long-term interest rates given current macroeconomic forecasts? I mean, at this point almost everyone expects unemployment to stay high for years to come, and there’s every reason to expect low or even negative inflation for a long time too. Shouldn’t that imply that the Fed will keep short-term rates near zero for a long time? And shouldn’t that, in turn, mean that a low long-term rate is justified too?

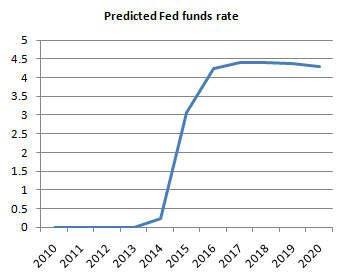

Now, take the CBO projection, which calls for unemployment to fall very slowly, and core inflation to stay low for quite a while too. Here’s what it implies for the Fed funds rate, taking the zero lower bound into account:

That’s right: four years of near-zero short-term interest rates. Does a 10-year rate of 2.6 percent still sound so unreasonable? And bear in mind that I’m not using some doomsayer’s forecast; I’m using the staid folks at the CBO.

…

Here’s what I think is going on: aside from the obviously intense desire of some of the bond bubble folks to see a fiscal crisis — they’ve been planning for it, and they’re not going to take no for an answer — my sense is that a lot of people just can’t bring themselves to face the reality that we’re likely to be in a zero-interest world for a long time. They just keep assuming that the Fed is going to raise rates soon, even though there is absolutely nothing about the macro situation that would justify such a rate increase.

David Rosenberg uses “bubble-rule-of thumb” and he quotes John Rogue:

“We don’t believe there is any “bond bubble”. However, there is a bubble in people believing there is a “bond bubble”. Here’s how you will know if there is a bond bubble — ask your colleagues how many of them own bonds in their personal accounts. When nobody/almost nobody raises their hand you should be comforted in knowing that the prospects of the existence of a “bond bubble” have been reduced. By the way, this tactic has worked wonderfully for gold over the last decade.”

Blinder: Fed’s running low on ammunition

The Fed is running low on ammunition, but not completely out of it. Former vice chairman of Fed’s Board of Governors, Alan Blinder, economics professor at Princeton University, lists four weak weapons the Fed is now left with, and he analyzes how the Fed should use them, and their limitations. A very insightful piece. (source: WSJ)

You may have noticed that the complexion of the U.S. economy has turned a bit sallow of late. The Federal Reserve definitely has. At its Aug. 10 meeting, the Federal Open Market Committee (FOMC) shifted attention away from its former concern—how to tighten a bit—and toward a new concern: how to loosen a bit. By central bank standards, this turnabout came at warp speed.

Chairman Ben Bernanke has told the world that the Fed is not out of ammunition. It still has easing options, should it need to deploy them. The good news is that he’s right. The bad news is that the Fed has already spent its most powerful ammunition; only the weak stuff is left. Mr. Bernanke has mentioned three options in particular: expanding the Fed’s balance sheet again, changing the now-famous “extended period” language in its statement, and lowering the interest rate paid on bank reserves. Let’s examine each.

• From exit to re-entry. The first easing option is to create even more bank reserves by purchasing even more assets—what everyone now calls “quantitative easing.” The FOMC took a baby step in that direction at its last meeting by announcing that it would no longer let its balance sheet shrink as its holdings of mortgage-backed securities (MBS) mature and are paid off. Instead, it will reinvest the proceeds in Treasury securities.

Two distinct policy shifts are embedded in this announcement. Most obviously, the gradual shrinkage of the Fed’s balance sheet—a key component of its exit strategy—comes to a screeching halt.

Less obviously, the purpose of quantitative easing changes. When the Fed buys private-sector assets like MBS it is trying to shrink interest rate spreads over Treasurys—and thereby to lower private-sector borrowing rates such as home mortgage rates—by bidding up the prices of private assets, and so lowering their yields. Judged by this criterion, the MBS purchase program was pretty successful.

But when the Fed buys long-dated Treasury securities it is trying to flatten the yield curve instead—by bidding up the prices on long bonds. That effort also seems to have succeeded, perhaps surprisingly so given the vast size of the Treasury market. Now put the two together. By reducing its holdings of MBS and increasing its holdings of Treasurys, the Fed de-emphasizes shrinking risk spreads and emphasizes flattening the yield curve. That strikes me as a bad deal for the economy because the real problem has been high risk spreads, not high Treasury bond rates.

If the FOMC is serious about re-entry into quantitative easing, it should buy private assets, not Treasurys. Which assets? The reflexive answer is: more MBS. But with mortgage rates already so low, how much further can they fall? And would slightly lower rates revive the lifeless housing market?

To give quantitative easing more punch, the Fed may have to devise imaginative ways to purchase diversified bundles of assets like corporate bonds, syndicated loans, small business loans and credit-card receivables. Serious technical difficulties beset any efforts to do so without favoring some private interests over others. And the political difficulties may be even more severe. So the Fed will go there only with great reluctance.

• What’s in a word? The FOMC has been telling us repeatedly since March 2009 that the federal-funds rate will remain between zero and 25 basis points “for an extended period.” This phrase is intended to nudge long rates lower by convincing markets that short rates will remain near zero for quite some time.

The Fed’s second option for easing is to adopt new language that implies an even longer-lasting commitment to a near-zero funds rate.

Frankly, I’m dubious there is much mileage here. What would the new language be? Hyperextended? Mr. Bernanke is a clever man; perhaps he can turn a better phrase. But market participants already interpret the “extended period” as lasting deep into 2011 or beyond. How much longer could any new language stretch that belief?

• Interest on reserves. In October 2008, the Fed acquired the power to pay interest on the balances that banks hold on reserve at the Fed. It has been using that power ever since, with the interest rate on reserves now at 25 basis points. Puny, yes, but not compared to the yields on Treasury bills, federal funds, or checking accounts. And at that puny interest rate, banks are voluntarily holding about $1 trillion of excess reserves.

So the third easing option is to cut the interest rate on reserves in order to induce bankers to disgorge some of them. Unfortunately, going from 25 basis points to zero is not much. But why stop there? How about minus 25 basis points? That may sound crazy, but central bank balances can pay negative rates of interest. It’s happened.

Charging 25 basis points for storage should get banks sending money elsewhere. The question is where. If they just move money from their accounts at the Fed to the federal funds market, the funds rate will fall—but it can’t fall far. After all, it has averaged only 16 basis points since December 2008. If banks move the money into Treasury bills instead, the T-bill rate will fall. But even if it drops all the way to zero, that’s not a big change from its 12-month average of 11 basis points (for three-month bills). So charging 25 basis points is no panacea.

But suppose some fraction of the $1 trillion in excess reserves was to find its way into lending. Even if it’s only 10%, that would boost bank lending by 3%-4%. Better than nothing.

• A fourth way out. There is a fourth weapon, which the Fed chairman has not mentioned: easing up on healthy banks that are willing to make loans. Given bank examiners’ record of prior laxity, it is understandable that they have now turned into stern disciplinarians, scowling at any banker who makes a loan that might lose a nickel. That tough attitude keeps the banks safe, but it also starves the economy of credit.

Well, quite a few of those bank examiners happen to work for the Fed. It would probably do some good, maybe even a lot, if word came down from on high that some modest loan losses are not sinful, but rather a normal part of the lending business.

So that’s the menu. The Fed had better study it carefully, for if the economy doesn’t perk up, it will soon be time to fire the weak ammunition.

Housing market is dreadful

New home sales is making new historical lows,

and existing home sales reached the lowest level since 1996.

(click to enlarge; graph courtesy of Calculatedrisk)

After the expiration of home buying credit, this was expected. But the magnitude of decline still shocked people. Due to slow sales, inventory of unsold homes starts to ramp up again.

And this is happening despite historically low mortgage rate. Two things might be working against potential home buyer’s psychology: 1) Is my job secure? 2) Will the house price keep falling?

(click to enlarge; graph courtesy of Northern Trust)

Is America in paradigm shift?

Long recession, high unemployment. Will the long ailing economy eat away American optimism?

Almost 3 years into recession (technically, the recession may have ended in summer of 2009), the current recovery looks much dimmer than previous ones (see details in the following article). In 1970s, there was also a lot of pessimism. Back then, the problem was high inflation and high unemployment, or the so-called “stagflation”. Now, we are facing a much worse scenario, the threat of deflation combined with high unemployment. With current employment trend, we will probably still be stuck with 9% unemployment rate by the mid of the next year. People started to feel the dent psychologically, and this pessimism is so easy to spread, believe me.

For contrarian investors out there, this is your best time looking out for opportunities. But before that, let’s take a minute to read this nice piece from the Journal, “The End of American Optimism“, by Mortimer Zuckerman:

Our brief national encounter with optimism is now well and truly over. We have had the greatest fiscal and monetary stimulus in modern times. We have had a whole series of programs to pay people to buy cars, purchase homes, pay off their mortgages, weatherize their homes, and install solar paneling on their roofs. Yet the recovery remains feeble and the aftershocks of the post-bubble credit collapse are ongoing.

We are at least 2.5 million jobs short of getting back to the unemployment rate of under 8% promised by the Obama administration. Concern grows that we are looking at a double-dip recession and hovering on the brink of a destructive deflation. Things are bad enough for Federal Reserve Chairman Ben Bernanke to have characterized the economic outlook late last month as “unusually uncertain.”

Are we at the end of the post-World War II period of growth? Tons of money have been shoveled in to rescue reckless banks and fill the huge hole in the economy, but nothing is working the way it normally had in all our previous crises.

Rather, we are in what a number of economists are referring to as the “new normal.” This is a much slower-growing economy that, recent surveys have revealed, is causing many Americans to distance themselves from the long-held assumption that their children will have it better than they.

What was thought to be normal in the context of post-World War II recoveries? One is that four quarters into the recovery, real GDP would expand at an annual rate over 6%. We are coming out of the current recession at a 2.4% growth rate.

We did enjoy a GDP boost from a buildup of inventories anticipating a recovery at normal speed, but it didn’t happen. David Rosenberg, chief economist of Gluskin Sheff, regards it as “frightening” that whereas the “normal” rate of increase in final sales is 4% annually, this time sales have averaged only 1.2%, the weakest revival in recorded history.

At this point after the onset of a recession, employment payrolls have typically exceeded 700,000 jobs above the previous peak. In this recession, we are still down roughly eight million jobs from the December 2007 peak. As for consumer confidence, the Conference Board survey shows an average a full 20 points below the average lows of previous recessions.

There seems to be a structural change in the American economy. The relationship of household debt to income has proven unsustainable. The ratio is normally established somewhere below 100%, but in 2007 the debt ratio hit 131% of income. It has now fallen to 122%, but at this pace it would take another five years to bring it under 100%. The pre-bubble norm was 70%. To get to this ratio again, debt would have to be reduced by about $6 trillion.

In the meantime, we may well be looking at a vicious cycle of defaults that in turn would produce credit tightening and still more economic weakness—compounding the caution among borrowers, lenders and public financial authorities.

The most obvious source of distress right now is lack of payroll growth, and it’s likely to get worse. Real unemployment today is well above the headline number of 9.5%. That number held steady only because 1,115,000 people gave up hope of finding work and left the labor force in the last three months. Otherwise the headline unemployment rate would have been around 10.4%.

Now there are at least 14.5 million Americans still searching for work: 1.4 million of them have been jobless for more than 99 weeks, 6.5 million have been jobless for over 27 weeks. This is a stunning reflection of the longer-term unemployment we are coping with.

…The Obama administration projects the unemployment rate will drop to 8.7% by the end of next year and 6.8% by 2013. That is totally unrealistic. It means we would have to add nearly 300,000 jobs a month over the next three years. At the rate we’re going, it will take anywhere from six to nine years to climb out of this hole. The labor market may be improving, but the pace is glacial.

If there is one great policy failure of this recession, it’s that we have not used the crisis to introduce structural reforms. For example, we have a gross mismatch of available skills and demonstrable needs. Businesses struggle to find the skills and talents that are needed to compete in this new world. Millions drawing the dole to sit around should be in training for the jobs of the future that require higher educational skills.

Given that nearly eight in 10 new jobs, according to the administration, will require work-force training or higher education, it furthermore makes no sense that we have reversed the traditional American policy of welcoming skilled immigrants and integrating them into our economy. Because of a recrudescent nativism, we send home thousands upon thousands of foreign students who have gotten masters and doctoral degrees in the hard sciences at American universities. These are people who create jobs, not displace them. The incorporation of immigrants used to be one of the core competencies of our economy. It’s time to return to that successful model.

Higher education is another critical issue. As President Obama pointed out last week in his speech at the University of Texas, we have fallen from first to 12th in college graduation rates for young adults. The unemployment rate for those who have never gone to college is almost double what it is for those who have.

Education may be the key economic issue of our time, Mr. Obama said in his speech, for “countries that out-educate us today . . . will out-compete us tomorrow.” To improve our performance will involve massive increases in scholarship support for higher education, and an increase in H-1B visas for foreign students who get M.A.s and Ph.D.s in the hard sciences.

But if the economic scene these days is daunting, the political scene is downright depressing. We have a paralyzed system. Neither the Democrats nor the Republicans seem able to find common ground to address what is clearly going to be an ongoing employment crisis. Finding that common ground is a job opportunity for real leaders.

Now let’s watch this interview of PIMCO’s El-Erian, the pioneer of the fancy phrase “New Normal”.

Update 1. David Rosenberg WSJ interview, in which Rosenberg explains his position of why the risk of US economy faltering is quite high, and what’s the best solution to revitalize the economy (this is a very informative piece, will be very useful for the macro-type).

So, if America is in a paradigm shift, what does this mean for China? In the past couple of months, I have been traveling in China, talking with fellow economists. There seemed to be a consensus that this recession is also the historical dividing line on China’s economic development path – China is also in a paradigm shift, moving away from a heavily export-oriented economy to a more consumption-domestic oriented economy.

The world is changing fast…

Summer retreat in Fontainbleau

I am in Fontainbleau, France, attending my department's strategic meeting at INSEAD. The discussion will be how to position economics department inside a business school, which I know nothing about. But I won't miss the chance to come to France for some good food. Having lived overseas for just over ten years now, I feel French food is the only cuisine who could rival Chinese in terms of variety and sophistication. Some other cuisine are sometimes very good, like Italian and Thai, but they lack variety. Another pleasure to travel in France is that you can always find a good café to sit down and sip a cup of coffee, while resting your tired legs.

Deflation Fears

How real is deflation threat? Why do economists worry more about deflation than inflation? Where should investors put their money during deflationary environment. On Point, my favorite program of WBUR, discusses these questions (source: NPR).

I also include a background chart:

(click to enlarge; source: CalculatedRisk)

Inflation (core CPI) in historical perspective:

(click to enlarge; source: St. Louis Fed)

Double dippin’

Bad time doesn’t mean we can’t have fun: