Why NBER hasn’t declared “recession is over”

David Rosenberg explains why:

There are two other critical factors preventing NBER from declaring the all-clear signal.

First, despite the dramatic rebound in the equity market in 2009, personal income fell in 49 of the 52 U.S. cities of a million population or more. The three cities that saw an increase were closely tied to the federal government (like Washington D.C.). Indeed, government pay managed to rise 2.6% last year while all the suckers that work in the private sector posted a 6% wage decline. How this doesn’t breed dissent is a legitimate question.

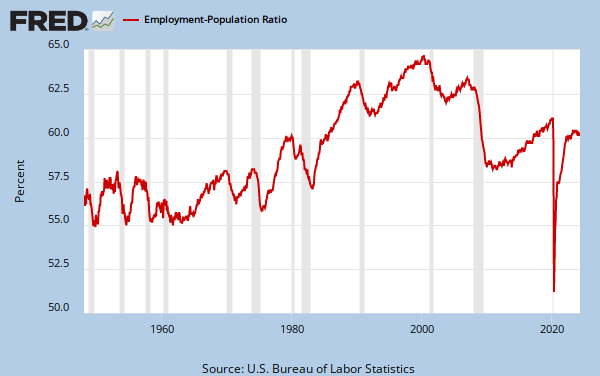

Second (…) is the rapid decline in the employment-to-population ratio. This is a far more informative measure regarding labour market performance than the traditional unemployment rate, especially at a time when discouraged workers are withdrawing from the labour force at such an alarming clip.

The employment rate has declined now for three months in a row, back to where it was at the start of the year, and smartalecks who see this recovery as anything but disturbing don’t realize that this employment rate, at 58.4%, is down from 64.0% at the 2007 high. This was the largest drop in the post-war era and what it means is that the economy is 12 million jobs shy of being at full employment.

Instead of declaring an outright war on unemployment, we instead have a government bent on measures to boost spending on cars and homes that nobody really wants since, at the margin, all people want to do is boost their once-depleted savings rates and get out of debt; or at least a half dozen housing plans to help distressed mortgage borrowers. Or infrastructure spending that so far seems to have helped line the pockets of public sector union officials with no obvious payback in terms of job creation. At least FDR paid people to work, even if it meant skyscrapers, bridges, monuments and national parks. They didn’t get paid do sit idle for 99 weeks so they can then drop out of the labour force and into oblivion (almost 45% of the unemployed have been so for more than 26 weeks — in no other recession in the past six decades did this share ever cross above 26%).

Almost half of the ranks of the unemployed have been looking for a job fruitlessly for at least six months. Let’s get these people re-engaged in the labour market, get them re-tooled and retrained for the skill set that businesses need now and in the future. Give these folks a shovel from 8 to 12 and engineering courses from 1 to 5 in return for their jobless insurance check. It’s time to get creative and aggressive with minimal cost to the taxpayer. If we can win this fight against unemployment, it’s amazing what other positive things will fall into place, from housing demand to government revenues to consumer credit quality.

Hong Kong – China’s currency lab

When to liberalize Chinese currency, Yuan or RMB? How to make Yuan more internationally influential? Hong Kong is being used by Chinese government as their forefront currency experiment lab. Reports WSJ:

![[HKVIEW]](https://sg.wsj.net/public/resources/images/MI-BE974_HKVIEW_NS_20100801171253.gif)

A burst of activity is under way here in the city that might be called China’s in-house research-and-development center for currency liberalization.

It’s on a tiny scale by normal standards of the $3 trillion-a-day market for foreign exchange. But in Hong Kong, banks are for the first time starting to lend yuan to one another outside mainland China and offering hedging services that weren’t available before. The result, say bankers, is reminiscent of the eurodollar market in the early 1960s, when extensive dealings in the greenback outside U.S. borders first took off.

The catalyst for this activity was an agreement signed June 19 between monetary authorities in mainland China and Hong Kong removing certain limits on usage of China’s yuan within Hong Kong. In the past, businesses were mostly confined to opening yuan accounts for trade-settlement purposes; now, accounts can be opened for any purpose. Businesses and individuals alike now can transfer yuan freely between accounts. Banks also can help businesses convert yuan without restriction.

…

With the latest liberalization move, banks in Hong Kong are now freer than ever to take all that yuan and put it to work. Some speak of linking the interest rate paid on yuan deposits to the direction of the euro or gold prices. Frances Cheung, senior strategist at Crédit Agricole Corporate & Investment Bank, foresees a market for yuan interest-rate swaps as interbank lending in the currency gains momentum.

…

Meanwhile, more and more yuan pour into Hong Kong. Monthly trade between Hong Kong and mainland China settled in yuan jumped tenfold from January to June to 13.24 billion yuan, or nearly $2 billion, and it’s set to rise more quickly since a pilot program allowing yuan settlement expanded to cover more of China in June.

Qu Hongbin, chief China economist at HSBC in Hong Kong, believes we are seeing just the tip of the iceberg. The anomaly, he says, is the fact that China conducts virtually all its trade in dollars, euros or yen. Historically, he says, “we’ve never seen a case where the world’s largest exporter uses other people’s currency for their trading.”