Home » Uncategorized (Page 24)

Category Archives: Uncategorized

Nudge and smart regulation

How to make our regulations smarter and more intelligent by utilizing psychology to shape human behaviors (source: Intelligent Investor of WSJ):

Franklin D. Roosevelt sent Wall Street to the torture rack. Barack Obama is sending Wall Street to the psychology lab.

A key component of President Obama's financial-reform package is its proposed Consumer Financial Protection Agency, which would apply findings from the science of human behavior to ensure "transparency, simplicity, fairness, and access" for borrowers, savers and other financial consumers.

That could make it a lot harder for a part-time worker to end up with an exploding mortgage that eats all her take-home pay. It might even mean that regulators will finally pay attention to the visual presentation of financial data — color, graphics and other factors that exert powerful sway over your decisions.

The proposal is an outgrowth of "Nudge," the brilliant book published last year by two University of Chicago scholars, economist Richard H. Thaler and law professor Cass R. Sunstein. A longtime friend of President Obama, Prof. Sunstein has been nominated to head the White House's Office of Information and Regulatory Affairs, a job often described as "the regulation czar."

In my view, a behavioral approach is decades overdue. Financial regulations always have been written mainly by lawyers and legislators — then promptly shot full of holes by promoters who understand how real human beings think and behave.

Lawyers think that the mere disclosure of risks and conflicts of interest provides the information that investors or consumers need. That is a fantasy. Faced with 47 pages' worth of "Risk Factors," investors come away with a warm glow of safety; risks that seem hard to understand appear unlikely to happen, and people who provide you with lots of detail seem likely to be honest.

To inform anyone, information has to be accessible. The central idea in "Nudge" is what Profs. Thaler and Sunstein call "choice architecture" — the context, format and framing of how decisions are presented to consumers. You will eat more nuts from a big bowl than from a small bowl. You will choose surgery if you are told it offers a 90% chance of survival; you will reject it if you are told there is a 10% chance it will kill you. The same people who would skip investing in a 401(k) if they had to "opt in" to the plan will participate if they have to "opt out" in order to skip it.

Prof. Sunstein, who is awaiting Senate confirmation in his post, declined to be interviewed. Cautioning that he can't speak for the Obama administration or Prof. Sunstein, Prof. Thaler discussed the new regulatory model. "The standard beer can is 12 ounces," he said. "That makes it pretty easy to compare beer prices. So now consider mortgages. It's not that you regulate the interest rates or the fees. But one way to make shopping easier is to make comparing the products simpler."

Thus, suggested Prof. Thaler, every bank or mortgage broker would have to offer two "safe-harbor" products with "standard terms that are easy to understand": a 30-year fixed mortgage with no points or prepayment penalties, and a five-year adjustable-rate mortgage. The market would set the interest rates. "By having these generic, simple mortgages," said Prof. Thaler, "you make everything else comparable."

Banks and mortgage brokers would remain free to offer more complex kinds of loans. However, added Prof. Thaler, "If the broker sells you a teaser-rate mortgage that you can't possibly afford once it resets, then as Ricky Ricardo used to say, he's got some 'splainin' to do" — including greater potential penalties from regulators. Mutual funds, 401(k)s and brokerage accounts wouldn't be regulated by the new agency but might well be influenced by its rules.

The proposal is about making regulation intelligent, not intrusive, said Eric Johnson, an expert on decision-making who teaches at Columbia Business School. "If you really do want a complicated, high-cost, high-risk mutual fund, you'll still be able to get it. But making sure that at least one option is not a disaster gives people an anchor."

Regulation that recognizes the limits of human rationality is an idea whose time has come. Like any good psychology lab, the proposed new agency will gather reams of data on how real people actually behave and adjust its rules accordingly, in real time. Of course, the financial industry will adjust its own behavior, trying to outsmart the new rules as fast as they are printed. But the war between the regulators and the regulated might finally be based on a realistic view of human nature, not fantasy.

Bailout

Country music got dressed up by economic theories and John Maynard Keynes.

Unemployment and Economic Recovery

Unemployment rate is a lagging economic indicator and it peaks long after recession ends. So how can a lagging indicator affect the burgeoning recovery? You may ask.

This short piece from WSJ takes on this traditional view that unemployment does not matter, and analyzes why in this recession unemployment will become the decisive factor to the path of the US recovery.

True, the markets are currently betting the old orthodoxy still holds sway. Unemployment has climbed quickly. The U.S. rate hit 9.5% in June, higher than any point since 1983, and up from 5.6% a year earlier, one of the steepest annual rises on record. In the euro zone, May’s 9.5% unemployment rate was the highest in 10 years. The Organization for Economic Cooperation and Development forecasts rates of 10% in the U.S. and more than 12% in the euro zone in 2010. But that has not stopped equity markets from rallying strongly, amid growing hopes of a recovery this year.

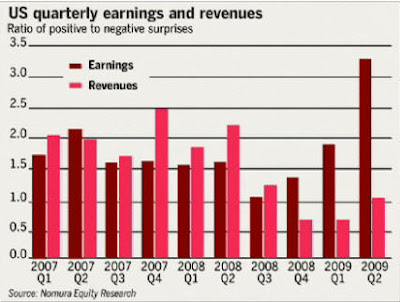

That’s partly because job losses and other cost cuts have provided a cushion for corporate profits: 82% of the S&P 500 companies to report so far have beaten second-quarter earnings expectations. The snag is that only 50% have beaten sales targets, as Deutsche Bank points out. For the moment, earnings are only being held up by costs shrinking faster than revenue. For a true recovery, sales need to start growing too. Rising unemployment may make that harder to achieve.

First, the flipside of improved corporate profits is real financial and consumer pain. U.S. credit card bad debt, for example, is rising faster than unemployment. Annualized write-offs of securitized credit card debt hit a record 10.8% in June, according to Moody’s. The agency expects that to rise to 12% to 13% in mid-2010. In Europe, Fitch’s U.K. credit card charge-off index hit a record high of 9% in April. Historically, investors have assumed that a one percentage point increase in unemployment will lead to a one percentage point increase in bad credit card debt. But the pace of job losses and levels of debt means nobody is confident previous correlations will hold. Similarly, rising unemployment could also hit house prices again, causing further turmoil for mortgage-backed securities.

Meanwhile, high unemployment is also likely to weigh on consumer sentiment. Nearly 60% of U.S. consumers expect high unemployment to persist over the next several years, the University of Michigan reported Friday. That could shape behavior: Federal Reserve Chairman Ben Bernanke warned last week that unemployment could weigh on consumer spending. Continued pressure on sales could be a further impetus for companies to cut costs and jobs, leading to more losses on consumer debt.

Financial Times also has a nice video analysis on that the current earnings growth was driven by aggressive cost cutting, rather than sales. Consumer demand still remains every weak.

(click on the graph to play video; source: FT)

Feldstein warns of ‘double-dip’ recession

Marty Feldstain says it's likely the economy will be dragged down again in the fourth quarter. He made a very good point that recovery from inventory buildup does not necessarily mean consumer demand will be bouncing back. In other words, after a huge debt bubble, there is simply not enough demand out there to sustain the recovery.

Link to video (source: Bloomberg)

Blinder: The economy has hit bottom

There are a few egg-heads Fed commentators worth listening to, Alan Blinder is one of them. In this piece, Alan Blinder explains how mechanically the economy could see a positive GDP growth in coming quarters, and why hitting the recession bottom can be good news and bad news.

How’s the economy, you ask? I have the proverbial good news and bad news, but in this case, they’re exactly the same: The U.S. economy appears to be hitting bottom.

First, the good news. Right now, it looks like second-quarter GDP growth will come in only slightly negative, and third-quarter growth will finally turn positive. Compared to the catastrophic decline we recently experienced—with GDP dropping at roughly a 6% annual rate in the fourth quarter of last year and the first quarter of this year—that would be a gigantic improvement.

Furthermore, there is a reasonable chance—not a certainty, mind you, but a reasonable chance—that the second half of 2009 will surprise us on the upside. (Can anyone remember what an upside surprise feels like?) Three-percent growth is eminently doable. Four percent is even possible. Surprised? How, with all our economic travails, could we possibly mount such a boom? The answer is that this seemingly high growth scenario isn’t a boom at all. Rather, it follows directly from the arithmetic of hitting bottom.

Bear with me for two paragraphs while I do some numbers. In recent quarters, several critical components of GDP have declined at truly astounding annual rates—like minus 30% and minus 40%. You know the culprits: housing, automobiles and business investment. (Also inventories, about which more later.) Eventually, those huge negative numbers must turn into (at least) zeroes. Notice that the move to zero doesn’t constitute a boom, not even a dead cat bounce, but merely the cessation of catastrophic decline. In fact, hitting zero growth and staying there would be a disaster scenario. We’ll almost certainly do better.

But watch what happens when—and remember, it’s when not if—the arithmetic of bottoming out takes hold. Housing, which is down to 2.6% of GDP, will serve as an example. In the first quarter, spending on new homes declined at a stunning 39% annual rate. If that minus 39% number turned into a zero in a single quarter, that change alone would add a full percentage point to that quarter’s GDP growth (because 2.6% of 39% is about 1%). If the move to zero were to happen over two quarters, it would add about a half point to each. Many people think housing may in fact bottom out in the third or fourth quarter. Autos may already have passed their low point. And business investment will follow suit.

Now back to inventories. Recent quarters have seen an almost unprecedented liquidation of inventory stocks, which means that American businesses were producing even less than the paltry amounts they were selling. That, too, must come to an end. As inventory change turns from a large negative number into just zero, GDP will get another a big boost.

Now the key point: None of these events are probabilities; they are all certainties. The only issue is timing, about which we can only guess. But if several of these GDP components happen to bottom out at roughly the same time, we could be in for a big quarter or two.

Feeling a little better? There’s more.

Remember the fiscal stimulus that everyone seems to be complaining about? One of the critics’ complaints is that little of the stimulus money has been spent to date. OK. But that means that most of the spending is in our future.

And remember all those interest-rate cuts the Federal Reserve engineered in 2008, in a futile effort to stem the slide? The Fed’s efforts were futile largely because widening risk and liquidity spreads negated any impacts on the interest rates real people and real businesses pay to borrow. Now those spreads are narrowing, which allows the Fed’s rate cuts to start showing through to consumer loan rates, business loan rates, corporate bond rates, and the like. In short, monetary stimulus is in the pipeline—a pipeline that was formerly blocked.

So why, then, is everyone feeling so blue? That brings me to the bad news: The U.S. economy is hitting bottom.

If things feel terrible to you, you’re not hallucinating. Economic conditions are dreadful at the bottom of a deep recession. Jobs are scarce. Layoffs abound. Businesses scramble for penurious customers. Companies go bankrupt. Banks suffer loan losses. Tax receipts plunge, ballooning government budget deficits. All this and more is happening right now, in what looks to be this country’s worst recession since 1938. At such a deep bottom, few people have reason to smile. (Bankruptcy lawyers maybe?)

What’s more, GDP is not terribly meaningful to most people. Jobs are—but they will take longer, maybe much longer, to revive. The last two recessions, while shallow, illustrated painfully that job growth may not resume for months after GDP bottoms out. And the unemployment rate won’t fall until job growth rises “above trend” (say, 130,000 net new jobs per month). That’s a long way from where we are today. So, even though the economy may be making a GDP bottom about now, the unemployment rate will probably keep rising for months—which is bad news for most Americans.

One last, obvious, but unhappy, point: The bottom of a deep recession leaves the nation in a deep hole. Our economy now has massive unemployment and vast swaths of unused industrial capacity. It will take years of strong growth to return to full employment.

After the last big recession bottomed out at the end of 1982, the U.S. economy rebounded sharply, with a remarkable six-quarter spurt in which annual GDP growth averaged 7.7%. That spurt induced President Ronald Reagan, running for reelection in 1984, to declare “It’s morning again in America.” Nobody thinks we can repeat that today, hampered as we are by a damaged financial system, decimated household wealth, rising foreclosures, and traumatized consumers who have suddenly learned the virtues of thrift.

So, yes, the good news is also the bad news. The economy is hitting bottom, but it’s a long, uphill climb to get out.

Mr. Blinder, a professor of economics and public affairs at Princeton University and vice chairman of the Promontory Interfinancial Network, is a former vice chairman of the Federal Reserve Board.

Goldman Sachs and bubbles

Listen to this heated debate on whether Goldman Sachs manipulated the market and engineered every bubble since the Great Depression. I reckon it's hard to justify such claim but without correcting the perverse incentives on Wall Street, traders of Goldman Sachs and alike will soon again risk the whole financial system in order to earn their big fat bonuses. I don't blame Goldman Sachs; I blame the misaligned incentive system. (source: On Point)

Bernanke: The Fed’s exit strategy

Ben Bernanke again (see his previous speech) outlines how the Fed will drain the liquidity out of the system in order to avoid the danger of inflation. The Fed got plenty of tools; but these are not what matter. What matters is whether the Fed can keep its independence in conducting monetary policy, and whether the Fed can find the right timing to tighten. I put 80% chance on that the Fed can keep its independence; but 20% chance on the Fed can find the right timing, given their failure to spot the housing bubble and the previous dot.com bubble. (Warning: this piece requires readers to have some basic understanding of Fed's balance sheet and common monetary policy tools)

The depth and breadth of the global recession has required a highly accommodative monetary policy. Since the onset of the financial crisis nearly two years ago, the Federal Reserve has reduced the interest-rate target for overnight lending between banks (the federal-funds rate) nearly to zero. We have also greatly expanded the size of the Fed’s balance sheet through purchases of longer-term securities and through targeted lending programs aimed at restarting the flow of credit.

These actions have softened the economic impact of the financial crisis. They have also improved the functioning of key credit markets, including the markets for interbank lending, commercial paper, consumer and small-business credit, and residential mortgages.

My colleagues and I believe that accommodative policies will likely be warranted for an extended period. At some point, however, as economic recovery takes hold, we will need to tighten monetary policy to prevent the emergence of an inflation problem down the road. The Federal Open Market Committee, which is responsible for setting U.S. monetary policy, has devoted considerable time to issues relating to an exit strategy. We are confident we have the necessary tools to withdraw policy accommodation, when that becomes appropriate, in a smooth and timely manner.

The exit strategy is closely tied to the management of the Federal Reserve balance sheet. When the Fed makes loans or acquires securities, the funds enter the banking system and ultimately appear in the reserve accounts held at the Fed by banks and other depository institutions. These reserve balances now total about $800 billion, much more than normal. And given the current economic conditions, banks have generally held their reserves as balances at the Fed.

But as the economy recovers, banks should find more opportunities to lend out their reserves. That would produce faster growth in broad money (for example, M1 or M2) and easier credit conditions, which could ultimately result in inflationary pressures—unless we adopt countervailing policy measures. When the time comes to tighten monetary policy, we must either eliminate these large reserve balances or, if they remain, neutralize any potential undesired effects on the economy.

To some extent, reserves held by banks at the Fed will contract automatically, as improving financial conditions lead to reduced use of our short-term lending facilities, and ultimately to their wind down. Indeed, short-term credit extended by the Fed to financial institutions and other market participants has already fallen to less than $600 billion as of mid-July from about $1.5 trillion at the end of 2008. In addition, reserves could be reduced by about $100 billion to $200 billion each year over the next few years as securities held by the Fed mature or are prepaid. However, reserves likely would remain quite high for several years unless additional policies are undertaken.

Even if our balance sheet stays large for a while, we have two broad means of tightening monetary policy at the appropriate time: paying interest on reserve balances and taking various actions that reduce the stock of reserves. We could use either of these approaches alone; however, to ensure effectiveness, we likely would use both in combination.

Congress granted us authority last fall to pay interest on balances held by banks at the Fed. Currently, we pay banks an interest rate of 0.25%. When the time comes to tighten policy, we can raise the rate paid on reserve balances as we increase our target for the federal funds rate.

Banks generally will not lend funds in the money market at an interest rate lower than the rate they can earn risk-free at the Federal Reserve. Moreover, they should compete to borrow any funds that are offered in private markets at rates below the interest rate on reserve balances because, by so doing, they can earn a spread without risk.

Thus the interest rate that the Fed pays should tend to put a floor under short-term market rates, including our policy target, the federal-funds rate. Raising the rate paid on reserve balances also discourages excessive growth in money or credit, because banks will not want to lend out their reserves at rates below what they can earn at the Fed.

Considerable international experience suggests that paying interest on reserves effectively manages short-term market rates. For example, the European Central Bank allows banks to place excess reserves in an interest-paying deposit facility. Even as that central bank’s liquidity-operations substantially increased its balance sheet, the overnight interbank rate remained at or above its deposit rate. In addition, the Bank of Japan and the Bank of Canada have also used their ability to pay interest on reserves to maintain a floor under short-term market rates.

Despite this logic and experience, the federal-funds rate has dipped somewhat below the rate paid by the Fed, especially in October and November 2008, when the Fed first began to pay interest on reserves. This pattern partly reflected temporary factors, such as banks’ inexperience with the new system.

However, this pattern appears also to have resulted from the fact that some large lenders in the federal-funds market, notably government-sponsored enterprises such as Fannie Mae and Freddie Mac, are ineligible to receive interest on balances held at the Fed, and thus they have an incentive to lend in that market at rates below what the Fed pays banks.

Under more normal financial conditions, the willingness of banks to engage in the simple arbitrage noted above will tend to limit the gap between the federal-funds rate and the rate the Fed pays on reserves. If that gap persists, the problem can be addressed by supplementing payment of interest on reserves with steps to reduce reserves and drain excess liquidity from markets—the second means of tightening monetary policy. Here are four options for doing this.

First, the Federal Reserve could drain bank reserves and reduce the excess liquidity at other institutions by arranging large-scale reverse repurchase agreements with financial market participants, including banks, government-sponsored enterprises and other institutions. Reverse repurchase agreements involve the sale by the Fed of securities from its portfolio with an agreement to buy the securities back at a slightly higher price at a later date.

Second, the Treasury could sell bills and deposit the proceeds with the Federal Reserve. When purchasers pay for the securities, the Treasury’s account at the Federal Reserve rises and reserve balances decline.

The Treasury has been conducting such operations since last fall under its Supplementary Financing Program. Although the Treasury’s operations are helpful, to protect the independence of monetary policy, we must take care to ensure that we can achieve our policy objectives without reliance on the Treasury.

Third, using the authority Congress gave us to pay interest on banks’ balances at the Fed, we can offer term deposits to banks—analogous to the certificates of deposit that banks offer their customers. Bank funds held in term deposits at the Fed would not be available for the federal funds market.

Fourth, if necessary, the Fed could reduce reserves by selling a portion of its holdings of long-term securities into the open market.

Each of these policies would help to raise short-term interest rates and limit the growth of broad measures of money and credit, thereby tightening monetary policy.

Overall, the Federal Reserve has many effective tools to tighten monetary policy when the economic outlook requires us to do so. As my colleagues and I have stated, however, economic conditions are not likely to warrant tighter monetary policy for an extended period. We will calibrate the timing and pace of any future tightening, together with the mix of tools to best foster our dual objectives of maximum employment and price stability.

—Mr. Bernanke is chairman of the Federal Reserve.

What India must do to become an affluent country

Martin Wolf writes on FT on what India must do to catch up with China and become an affluent country in a generation. Compared to China, in my mind, India enjoys the advantage of being a democratic country (Indians may not feel the same way), but its caste system, poor infrastructure, and bureaucracy are really dragging its feet.

I am a true believer of competitions, including competitions between countries. Without China’s fast growth since 1978, India may not have had the urge to initiate its own reform in mid 90s; and without India rising in IT and innovation, China may still have specialized in manufacturing only. Competition can produce win-win situation. Most politicians focus on how to grabbing a bigger share of the same pie; economists, fundamentally optimists, focus on how to create a much bigger pie, even sharing a smaller part of it.

What India must do if it is to be an affluent country

What will the world economy – indeed, the world – look like after the financial crisis is over? Will this prove to be a mere blip or something more fundamental? Much of the answer will be provided by the performance of the two Asian giants, China and India. Rightly or wrongly, it is widely accepted that China will continue to grow very rapidly. But what is the likely future for India?

I attended debates on this question in Mumbai and Delhi two weeks ago. The occasion was the launch of a report prepared by the Centennial Group for this year’s Emerging Markets Forum.* It addresses a provocative question: what would need to change if India were to become an affluent country in one generation? The answer is: a great deal. But one thing is clear: after the performance of the past three decades, the goal is not laughable.

Since 1980 the average living standards of Chinese and Indians have, for the first time in the histories of these two ancient civilisations, experienced a sustained and rapid rise. In one generation, India’s gross domestic product per head rose by 230 per cent – a trend rate of 4 per cent a year. This would seem a fine accomplishment if China’s had not increased by 1,090 per cent – a trend rate of 8.7 per cent. Yet even if India has lagged behind, the change has been large enough for aspiration to replace resignation as the ethos of a large and rising proportion of Indians.

The recent past offers at least four further reasons for optimism. First, the rate of growth has been accelerating: over the five years up to and including 2008, the average annual rate of economic growth was 8.7 per cent, up from 6.5 per cent at the previous peak in 1999. Second, vastly higher savings and investment underpin this acceleration, with gross domestic savings up to 38 per cent of GDP in the financial year 2007-08. Third, India’s economy has globalised, with the ratio of trade in goods and services up to 51 per cent of GDP in the last quarter of 2008, up from 24 per cent a decade before. This was not far behind China’s 59 per cent of GDP (see chart below).

Finally, the democratic political system, for all its frailties, works. Indian democracy is a wonder of the political world. What happened in the past election seems a big development – the re-election of a Congress-led government, with a big increase in the party’s seats. It is widely believed that this reflects a choice of competence over caste and secularism over sect. Not least, the electorate registered approval of the competence and integrity of Manmohan Singh, the prime minister. I have been lucky to have known Dr Singh for three and a half decades. I admire nobody more. I only hope he is prepared to use his possibly final period in office boldly.

So what needs to happen if Indians are to enjoy an affluent lifestyle? The answer, suggests the report, is that India must sustain growth at close to 10 per cent a year over a generation. This is not inconceivable: China has managed that, from a lower base, over three decades. But it is a massive task, particularly for so huge, diverse and complex a country. Extraordinary change would have to occur, inside India and in India’s relationships with the world.

For this to be conceivable, at least four things would have to happen: the world must remain peaceful; the world economy must remain open; India must avoid the stagnation into which many middle-income countries have fallen; and, finally, the resource and environmental implications of its rise to affluence must be managed.

Moreover, India itself must overcome three big challenges: maintaining, indeed strengthening, social cohesion at a time of economic and social upheaval; creating a competitive and innovative economy; and playing a role in its region and the world commensurate with the country’s size and rising importance. In fundamental respects, India must turn itself into a different country.

Not least, as the report makes clear, India would have to be governed quite differently. In India a vigorous, albeit too often corrupt, democratic process has been superimposed on the “mindsets, institutional structures and practices inherited from the British Raj”. India has prospered despite government, not because of it. It is a miracle that the giant has fared as well as it has. But if this country is to prosper it must create infrastructure, provide services, promote competition, protect property and offer justice. The country must move from what the report calls “crony capitalism and petty corruption” to something different. The quality of government, widely believed to be deteriorating, must, instead, radically improve.

Just how far the transformation would have to go is shown by the “seven inter-generational issues” on which this report focuses: first, tackling disparities, not least among social groupings, but without further entrenching group-based entitlements and group-based politics; second, improving the environment, including the global environment; third, eliminating India’s pervasive infrastructure bottlenecks; fourth, transforming the delivery of public services, particularly in India’s ill-served cities; fifth, renewing education, technological development and innovation; sixth, revolutionising energy production and consumption; and, finally, fostering a prosperous south Asia and becoming a responsible global power.

I take two big things from the analysis in this report, one for India and another for the world.

For India, I conclude that even sustaining recent performance is going to be very hard. The era when the country could prosper just by stopping government from getting in the way is ending. India now requires efficient, service-providing government by competent technocrats and honest politicians. Of course, many foolish interventions still need to be removed. The government also needs to refocus its limited energy and resources on its essential tasks. But it must be able to perform these tasks far more effectively than it can today.

What I take for the world is that India, for all the huge challenges it confronts, is likely to continue its rise, if more slowly than the report assumes. The job of adjusting the familiar western ways of thinking about the world to the new realities has hardly begun. Within a decade a world in which the UK is on the United Nations Security Council and India is not will seem beyond laughable. The old order passes. The sooner the world adjusts, the better.