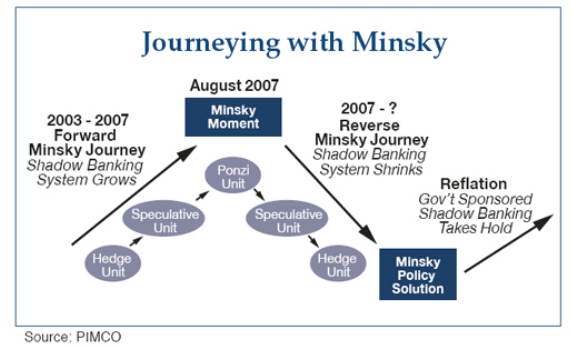

Minsky Moment in a nutshell

PIMCO’s Paul McCulley gives us a nice graph on Minsky moment:

China: Reverse Brain Drain

Following my last post on China’s hunting for the Wall Street talents, NY Times had another report: “Chinese financial institutions, in a reverse brain drain, are looking to recruit from the ranks of recently laid-off finance sector employees”.

How Iceland Collapsed

Icelanders borrowed over 200% of their income, and in foreign currencies. Many countries in Eastern Europe have the similar problem.

Commodities outlook

Interview of Don Coxe of BMO:

Get ready: for a lost decade

Sometimes it's a complete takeover; sometimes it's a bailout in the form of capital injections. Government has been in a steep learning curve in this crisis and thus far it lacked a coherent strategy. As argued in this article below, an one-time experience of Great Depression does not at all guarantee we will do absolutely better this time; Politics works in its own twisted mechanism, especially in a democracy. So don't be surprised if we have a Japan-like lost decade or even another Great Depression.

Get Ready for a Lost Decade — Bad times don't produce good policy

How many times have you heard that we've learned the lessons of the Great Depression and won't repeat the same mistakes?

![[Business World]](https://s.wsj.net/public/resources/images/ED-AI757_bw1224_DV_20081223142820.jpg)

That statement is a bit of a false promise, since there was only one Great Depression, and many, many steps were taken and not taken, with no chance to rerun the experiment over and over to figure out what worked, or would have worked, and what didn't.

Letting hundreds of banks collapse, destroying savings and confidence, is one mistake we won't make again. But many want to insist, without evidence, that more government spending would have ended the depression. That's the direction the Obama administration is taking. Others say government did not do enough to restore business confidence, or did too much to damage it, piling on taxes, regulation and labor unions. This at least is firmer ground. Plenty of evidence from history shows that actions hostile to business tend to be related to an absence of prosperity.

But more important than these talismanic assurances about what we've learned from the Great Depression is the mistake in assuming that, even if we had a coherent view of what should be done, coherent polices would therefore be implemented.

This has little relation to how policy is made in a democracy.

Policy is always bad to a degree, but long periods of prosperity tend to be self-reinforcing since powerful interests are born with the means and motive to preserve the status quo. That status quo may really be a contributor to prosperity, such as regulatory restraint and moderate tax rates. That status quo may in some respects be ill-advised, such as excessive subsidy to housing debt.

But once prosperity blows up, the quasi-virtuous policy circle becomes an unvirtuous one as new interest groups come to the fore to exploit an appetite, previously weak, to impose their costly or vindictive wish lists. And even well-meaning policy gets twisted and rendered incoherent.

It's already happening to our banking bailout. If injecting government capital to improve confidence in banks was a good idea, it did nothing to improve the banks' own confidence in their borrowers. Yet now that banks have government capital, they're being pressed to lend to politically favored constituents regardless of their own judgment about whether the borrower is good for the money.

Or take the gathering auto bailout: Taxpayer dollars are being thrown at Detroit auto makers to make them "viable," even as Congress imposes new fuel-mileage mandates requiring them to incur tens of billions in costs unlikely to be recouped from their customers — the definition of "nonviable."

Mr. Obama's troops palpitate with excitement at the prospect of $1 trillion in "stimulus," though any net benefit to the economy likely will be incidental. Al Gore has thrown out the window any unpopular carbon taxes in favor of direct subsidies to his green energy investments. He sees the moment for what it is — alarm about global warming has degenerated into a pretext. Billions will be diverted from useful purposes to create "green jobs" that deliver no meaningful impact on climate or the accumulation of atmospheric carbon.

Large "confidence" costs were always destined to flow from the extreme steps being taken, even if advisable, to prop up the economy. The federal government's alternating takeovers and bailouts of companies are inherently destabilizing and create massive uncertainty in investors and businesses. The Fed's shocking steps to print money and acquire every kind of private asset and, soon perhaps, washing machines and Chevy Tahoes, may in retrospect be seen as just the right medicine. At the moment, no rational investor or business manager looks upon such doings with confidence in our economic future.

On top of it all, the Madoff scandal is peculiarly demoralizing in ways that may make its impact greater than the sum of its parts.

Our point here is that the bad policy vicious circle probably has a long way to run. While it's still possible to entertain wild hopes about an Obama administration, such hopes are partly self-liquidating on closer inspection — they exist in the first place only because Mr. Obama has given us so little to go on, except campaign boilerplate.

Bottom line: Politics is in charge — in a way that makes a lost decade of subpar prosperity more likely than not.

Happy Holidays.

China’s data massage in 2009?

Just like in Asian financial crisis, Chinese officials may have to massage their data again to make the growth figure look better, so that there would be no challenge to their ruling power.

In 2009, China watchers may double check GDP number with industrial production, and electricity usage, to find the potential discrepancies.

Read report from WSJ:

China's economy is slowing. By just how much is a bit of a guess.

The uncertainties around Chinese economic data-gathering make it hard to tell. Yet with China likely to be one of the few major economies to show growth next year, the question is pretty crucial. Already there are concerns Beijing could massage its GDP data next year.

![[China's Economic Data]](https://s.wsj.net/public/resources/images/MI-AU184_CHINAH_NS_20081225215216.gif)

Keeping the annual growth rate above 8% has for long been the sine qua non of Chinese economic policy. That rate was 9% in the third quarter, and all the economic news since then points to a lower rate in the past three months of this year.

Any dip below 8%, however temporary, would be a blow to the government's standing. Having announced a $586 billion fiscal-stimulus package this autumn, the government needs to show that it has worked by next year.

For economists, the key frustration in China's GDP figures is the lack of a quarterly expenditure breakdown to balance the output figures that the statistics bureau provides. Mark Williams, of consultancy Capital Economics, says proxies for consumption, investment and net trade actually suggest the Chinese economy grew more quickly in the third quarter than 9%.

So what can China-watchers turn to as a check on official GDP data, and a means to divine the future?

Stephen Green, Standard Chartered's head of research, tracks a mixture of industrial goods production, freight activity, bank-credit growth and commodities imports to derive a measure of real activity in China. That is currently showing "very weak" growth momentum going into the first part of 2009. China's own industry minister has said industrial output needs to expand by 12% next year if the economy is to retain its 8% expansion rate. In November, industrial production grew by just 5.4% on an annual basis.

Looking further forward is more frustrating. Standard Chartered found that neither money-supply measures nor purchasing managers' indices, consumer expectations or even the stock market are reliable leading indicators.

Still, the totemic 8% growth mark will be at risk early next year. Exports, which have contributed about 20% to GDP over the last couple of years, fell year-on-year for the first time since 2001 in November, and an imminent recovery in China's main markets looks unlikely. The property sector is still in a slump, and domestic consumer spending isn't making up for the slowing of both these areas.

Set against this is the $586 billion stimulus package spread over 2009 and 2010, but its effects mightn't be felt until the second half of 2009 at the earliest. By that time, the speed and magnitude of the slowdown should already have made annual growth of 8% impossible to achieve.

The first and second quarters of 2009 will provide a stern test of China's 8% growth commitment, then — and the probity with which those figures are produced.

Jim Rogers

His investment outlook for 2009. Rogers’ views tend to mirror the Austrian economics, where everything that governments are trying to do is treated with deep distrust and suspicion.

But I agree with his outlook on agricultural commodities; Inflation is a big worry down the road; and watch when treasuries bubble bursts.

Euro’s dilemma

source: wsj

All governments would like a weaker currency to ease the pain of the financial crisis — and nowhere more than the euro zone, where the soaring common currency is inflicting economic pain and exposing political tensions. The euro zone is likely to get its wish granted in 2009.

![[Euro]](https://s.wsj.net/public/resources/images/MI-AU185A_EUROH_NS_20081225205618.gif)

As political tensions mount, investor confidence in the euro will suffer, bringing about the devaluation needed to stop it falling apart.

Investors are aware of the tension, judging by the higher premiums they want for buying the debt of weaker euro-zone economies. Italian, Portuguese and Greek government debt trades at spreads of at least one percentage point above equivalent German 10-year bonds, the highest since the euro was created in 1999. That only makes sense if investors believe there is a possibility a euro-zone member might default or even quit the single currency.

That may seem a distant prospect today, but there already is a wide disparity in the public finances of individual member states. The German government has total debt of 65% of GDP and a projected budget deficit for 2009 of around 0.5%. In contrast, Italy has total debt of 104% of GDP and a projected deficit for 2009 of more than 3%. That makes a mockery of EU rules for debt to be no greater than 60% of GDP and for annual deficits to be kept below 3%.

Weaker member states may be tempted to borrow even more to avoid a catastrophic slump, caused partly by the strength of the euro. In terms of purchasing power, the single currency is at least 20% overvalued against the dollar. With a U.K.-style devaluation out of the question, that is a particular problem for countries like Ireland and Spain, trying to restore their competitiveness and recover from burst property and construction bubbles. Credit Suisse reckons Irish and Spanish wages need to fall 20% to 30%, something no government could countenance.

In any other single currency area, this would be resolved via massive borrowing by a centralized agency, much like the U.S. Treasury, and fiscal transfers between regions. The euro zone has no mechanism for this to happen. Reluctantly resigned to spend more than it wanted to stimulate its own economy, Germany is still unwilling to fund a massive fiscal-stimulus package to revive the euro-zone economy. Hence the risk of disorderly borrowing by other countries, taking advantage of investor appetite for government bonds.

That won't please the Germans. After decades of hard work to build up their inflation-fighting credentials, they also fear they will be forced to pick up the tab if a member state defaults. On the other hand, it may stop the euro falling apart, and trigger the devaluation the eurozone economy so urgently needs.